Professional financial hackers have a lot of common with the organized crime. And not only

in respect to common addictions

to cocaine and prostitutes. But there is a subtle difference: financial hackers make it daily (and

very lucrative) business to figure out ways to abide by the letter of the law while violating its

spirit. Although the claim that they do not break the law has very little credibility. They do break

the law, but at the same time their political influence is big enough to keep them out of jail. In

2012 Lanny Breuer, then the head of the Justice Department's criminal division openly admitted

that. In a speech at the New York City Bar Association he said that he felt that it was his duty to

consider the health of the company, the industry, and the markets in deciding whether or not to file

charges. Which in case of Goldman represents insurmountable obstacle to criminal prosecution.

In any case GS converted itself into a special type of TBTF company, the company that specialized in hacking financial system. And in a large company internal

politic can turn really destructive both to the firm and society at large. In fact, in large

companies there are

people with very high IQ at the top with personal traits that makes them more dangerous in comparison with

bosses of Mexican gangs.

It also makes internal political battles more vicious. BTW, a lot of

psychopaths have above average IQ.

In a way the USA never had a subprime crisis. What we had was systemic, neoliberalism-induced crisis that involves FED,

government, congress, banking, ratings, insurance, investment and financial industries (the banks were

at the center of this crime syndicate and they were the largest beneficiaries of the crimes committed),

one manifestation of which was 2008 subprime crisis.

Large banks became huge, dominant political force and based on their political weight, they hacked the

financial system in the same way computer hackers hack computers systems to suit their short term needs

and first of all for enrichment of the brass (appetite for "make money fast" schemes was greatly raised

during dot-com crisis).

As Simon Johnson wrote in May 2009 the USA had a

The Quiet Coup with banks becoming the most favored and the most protected industry of the Congress.

Financial system is essentially a system of rules. If a rich and powerful organization is directed toward

hacking the rules: finding weaknesses and exploiting them it is undistinguishable from mafia in a very

precise meaning of the term (organize crime syndicate with strong ethnic component), only more sophisticated.

Again they are not gangsters in traditional meaning of this word, they are of a hackers, and as such

they are much more difficult to prosecute. As a comment to blog post at EconomistView by "Eric"

(Paul Krugman The Unwisdom of Elites) aptly stated:

Villains....who exactly? The principle reason that there have been few prosecutions of high level

bankers is that not so much that got done was illegal. Reckless, maybe. But even here is it really

reckless behavior if you have a belief -- which turns out to be true -- that public finances will

bear the downside risks on your behalf?

In hindsight it feels like these things should have been illegal, but the available serious punishments,

such as not bailing out AIG, not allowing various investment firms to become bank holding entites,

not backstopping the GSEs (read their debt issues and you'll see that nowhere is a claim made for

public backing), not taking first loss positions on Bear Stearn assets, etc., etc., were foregone

by voluntary actions by public officials.

Make peace with the truth that there will be no sweeping prosecutions, least of all by the federal

government of the USA.

Those are serious, well educated and well motivated guys which are paid good money for finding the

flaws and based on this knowledge subverting existing system of rules, rules which are the essence of

financial system. Essentially they are professional financial system hackers. Or a strange

brand of Harvard trained Mafiosi (and again, Mafia is nothing more that a diversified criminal business

with strong ethnic component ;-). But unlike Mafia they have really good connections in government

and essentially captured the government in a silent coup. In a way this organization behaves like cancer

cells in a human body and prognosis is not that good, despite the fact that the patient survived one

time:

Finanally, the Great Recession was brought on by a runaway financial sector, empowered by reckless

deregulation. And who was responsible for that deregulation? Powerful people in Washington with close

ties to the financial industry, that’s who....

Due to deregulation which was the important part of neoliberal doctrine, they become legislators

of their own business... Here is what a telling quote from the post

Overruled found on

macrobusiness.com.au

But in global finance there are some things happening that are genuinely different. Dangerously

so. It is becoming a hall of mirrors, money referring to itself in an

infinite regress. Little wonder that people are attracted to gold, because gold seems

to be a tangible, solid measure of value, something we can rest on in an environment where everything

seems relative. Yet this, too, is an illusion. The yellow metal only has value because it has a history

of being deemed to have value. It is no more an objective measure of value than the pieces of coloured

plastic, notes, that make up legal tender.

To explain what I mean, let’s start with a definition of what

money is. It is rules. Rules about value and obligation. Those rules are usually based on legally

enforced structures, although that need not be the case. In the case of cross border capital markets,

the enforcement is informal because there is no supranational government to impose penalties. Disputes

are resolved by a handful of law firms, the main penalty is to be prevented from participating for

a period.

Now if money is rules, then what does it mean to “de-regulate

financial markets” as was claimed in the 1990s? Can you de-regulate

rules? Obviously not. So what happened? The place where rules were set shifted.

Instead of government for the most part making the rules, the

traders started making the rules. The logic was, as Alan Greenspan

argued, that because everyone was acting in their self interest then nothing could possibly go wrong.

Pricing would be accurate, the less formal self organisation of the market would be superior to the

formal oversight of governments (what would governments, which are always bad, know?) and everyone

would win. Free lunches as far as the eye can see.

So the rules proliferated, especially after the advent of the

Black and Scholes pricing of risk, a clever piece of maths based on what is probably circular argument,

but one that is sufficiently concealed to give traders the impression that they are handing off risk

accurately. This led to the explosion of derivatives and securities markets, including such instruments

as collateralised debt obligations, credit default swaps and endless hedging games (my personl favourite

is a derivative on “volatility”).

Now the point about rules is that they are based on agreement,

and their creation can be without any limit provided traders are prepared to agree, to trust each

other enough to transact. They are not finite in the way that, say, gold is. And so the rule making

exploded. The global stock of derivatives is $US600 trillion, about twice the capital stock of the

world (all the shares, property, equities, bonds and bank deposits). Far from deregulation making

the rules of finance more more streamlined and more efficient — as if the efficiency of money could

be measured anyway, given that it would mean measuring money with itself — the rule making expanded

wildly. And we all know what happened when the trust that underlies those rules collapsed.

Lloyd Blankfein personality (The Independent called him

the prince of Casino Capitalism) also suggests that GS

might operate in the throes of an addiction to gambling. And they know they are controlled

by their addiction, and so they hate themselves, like addicts typically do, for their lack of self-control.

They also see what their addiction is doing to the nation and the world, and guilt collides with craving,

making the addiction even more disturbing.

From the Wall Street Journal

In December 2007, after the firm distributed multimillion-dollar bonus checks in part thanks to

bets on a mortgage meltdown, about 10 Goldman mortgage traders, surrounded by dozens of cheering

colleagues, wolfed down the burgers, according to attendees. Bystanders wagered cash on how many

burgers the traders could eat.

The annual event resembled a scene out of “Liar’s Poker,” a book depicting bawdy antics of bond

traders at Salomon Brothers in the 1980s. In fact, the 2007 contest was held just a few floors away

from where the Salomon traders worked when that firm leased space in the same Manhattan building.

It was a lower-stakes version of what went on every day in the group: aggressive, take-no-prisoners

trading. Mortgage-backed bonds, including complex derivatives that tracked pools of risky loans,

were traded for big money in Goldman’s 400-person mortgage unit.

Addicts used to hate their actions, hate the world that lets them act, and they dehumanize the victims

who suffer from it in a way that the strong hate the weak.

The real question about Goldman is what constructive role in economy those guys play. Are they just

government supported and government protected extortion gang operating mainly in developing market,

but due to inertia ripping off home constituents? Is Goldman really such an indispensable financial

intermediary? If one looks at the firm’s revenue breakdown it's clear that this is more of a casino

than anything else, and some of GS moves are savagely predatory and put the economy in danger (they

were instrumental in causing the collapse of AIG (see

Janet Tavakoli- Goldman Sachs Nearly Bankrupted AIG); saving AIG was largely about saving the derivatives

market, which is so big and unstable that the bankruptcy of a large and intertwined counterparty could

mean the bankruptcy of all gamblers including Goldman). AS

Karl Denninger

noted on April 12, 2009:

There is a rumor about Goldman Sachs flying around on the street - allegedly they are about to report

their second-best quarter in history, +$12 billion or so.

A 47 percent gain for the company’s stock price this year and a return to profitability in

the first quarter may help Chief Executive Officer Lloyd Blankfein raise new money, analysts said.

That might let Goldman Sachs, the sixth-biggest bank, return the cash received in October from

the Treasury’s Troubled Asset Relief Program and shake off compensation and hiring restrictions

imposed on banks that took the U.S. aid.

Gee, you don't think being paid by the taxpayer through AIG's "conduit" for losses that didn't

(yet) happen at 100 cents on the dollar might have anything to do with that, do you?

And further (and potentially much worse) there is the repeated statement by Goldman executives

that they were "fully hedged" against a potential counterparty default by AIG.

One wonders - was that "hedge" to be short the equity on AIG itself, perhaps?

Why is this important?

Because if that's how Goldman hedged they got paid twice and the taxpayer literally

got robbed.

Someone in Congress needs to look into this now; there are already rumblings

of investigation. Those rumblings need to get a lot louder and turn into subpoenas,

not "polite inquiries."

If in fact Goldman (or anyone else) was "hedged" against a possible credit loss from their CDS

with AIG and they were able to collect on that hedge (no matter what it was)

those payments through AIG need to be clawed back immediately as nobody is entitled

to be paid twice for the same risk and reap what amounts to a windfall profit by quite literally

engineering a multi-billion dollar transfer of funds from the Taxpayer to the firm!

This is not small potatoes either - we're talking $100 billion+ in aggregate with these various

banks on a worldwide basis.

We the people deserve answers on this right now and if persons in our government handed these

banks $100 billion dollars of our tax money for what was a covered bet, allowing them to collect

twice on a risk that had not yet been realized (when at most they were entitled to collect once via

their private hedging activity) every single person involved in that scandal must be immediately

removed from office, prosecuted if possible, and every nickel of those funds must be clawed back

by whatever means are necessary.

The fact that GS is run by a compulsive gambler completes the picture. It’s a hybrid hedge

fund and bookie, with an investment bank and asset management business attached to create some respectability.

As NYT wrote

(Clients

Worried About Goldman’s Many Hats )

Goldman’s trading operation has grown so pivotal and influential that many analysts say the firm

as a whole now operates more like a hedge fund than an investment bank — another benchmark of the

firm’s internal evolution that can create new friction with clients.

Is we assume that GS is a parasite on the body of the society, the question arise who is protecting

such a mass scale racket in comparison with which Russian mobsters are just children. “Great vampire

squid" Goldman Sachs is a strange firm and sometimes it is difficult to figure where GS ends and government

starts and vise versa.

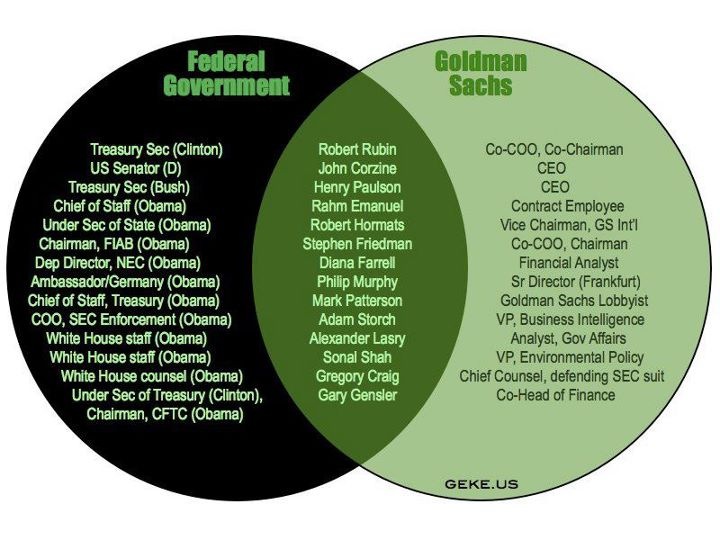

Paulson continued to appoint Goldman Sachs alumni to positions of power after the AIG decision—he

named Edward C. Forst, a former head of Goldman’s investment-management division, to help draft the

$700 billion Toxic Asset Relief Program (of which $10 billion went to Goldman Sachs), and then Neel

Kashkari, a former Goldman V.P., as the TARP manager. And of course Edward Liddy, former Goldman

board member, was already serving as the new CEO of AIG. Suddenly, everywhere you looked, men who

had passed through the Goldman gauntlet of loyalty and rewards were now in key positions overseeing

the rescue of the financial system. The company was earning its nickname: “Government Sachs.”

"Goldman's activity is of negative social value. Its recent profits came from trading, which basically

amounts to profiting from insider information at the expense of others," says

Stiglitz.

GS is more like a hedge fund then an investment bank. While slimy business practices of Goldman Sacks

flourished in the atmosphere of deregulation, the idea of milking fiat money system with stock

market is the central in GS business model. That's why a recent

Rolling Stone article called the firm a "great vampire squid wrapped around the face of humanity,

relentlessly jamming its blood funnel into anything that smells like money." And a 2007 New York Times

column likened its culture to the KGB, the former Soviet Union's secret police.

It's not as if Goldman escaped the financial crisis unscathed. There was a period of chaos last year

when Blankfein admits he was willing to consider any option to survive, including merging with Citigroup,

which by contrast is today considered one of the weakest financial institutions, 34%-owned by the government.

Recently Goldman short selling of MBS during the time the other arm of the firm was packaging them caused

a lot of outrage, but nothing was done so far by Obama administration to curb abuses. We will see if

Blankfein will go to jail for perjury.

Professor Krugman, other wise people have also noticed the same mind boggling phenomenon that

you very well pointed out. What has this great country become now? Goldman Sachs and what it represents

have shear contempt for each and everyone of those they have the Audacity to repeatedly and legally

rob, the retirees, the pension funds of teachers and firefighters, 401ks of the workers and savings

of all decent people.

Your suggestion that Goldman worked its miracles by being clever is

disingenuous. As the Times own Gretchen Morgenson demonstrated,

Government Sachs worked it miracles by sitting down at the private table

with goverment decision-makers -- like its old boss Hank Paulson --& hammering out recovery program

that benefitted Goldman & whenever possible maimed or killed its competitors (bon

voyage, Lehman brothers). If Goldman is corrupt, its Toadies in Treasury T-shirts are worse. Geithner

& the top Goldman alum who run Treasury should all be fired, & Goldman should never again enjoy the

special status it has acquired through well-placed veterans. There can never be honest & effective

regulation when Goldman & its revolving bureaucrats decide what & who is to be regulated. The change

we can believe in come from leaders who serve the people; not those who serve big banking.

I am on a completely different ideological plane than you are. I think your Keynesian economics

are a complete and absolute fraud. BUT what you say about Goldman Sachs is fact. I do not think that

you go far enough. Too many government players are involved with or developed from Goldman. They

guided our policies in a way that helped Goldman. More than anything, a special prosecutor needs

to be appointed to investigate this travesty of justice.

One quick side note, Asset Backed Securities and other derivatives

are not inherently bad, they are bad in the hands of scummy New York investment banks.

But otherwise they can help small entities raise capital and allow their business models to flourish

and withstand the onslaught of larger entities.

===

This isn't the American Dream anymore, but the great American Fraud! The US has now the best of

both worlds: the privatisation of the profits, and the socialization of the losses!

I do hope that with their robust democracy the US will come out of this situation in a better

manner.

10 reasons why Wall Street has absolute power over America's democracy

Paul B. Farrell, MarketWatch Last update: 7:13 p.m. EDT April 20,

ARROYO GRANDE, Calif. (MarketWatch) -- Two mind-numbing fast-paced dramas. Two parallel worlds.

One real, one fiction, both deadly. Jack Bauer, mythic hero of "24." Dying from a deadly bio-pathogen

leaked from weapons developed by Starkwood, a rogue mercenary army attacking the presidency, hell-bent

on taking over America.

The other drama in play: "Hank the Hammer" Paulson, iconic Wall Street hero, a Trojan Horse placed

inside Washington by Goldman Sachs as Treasury Secretary in control of America's $15 trillion economy.

Goldman, a modern dynasty with vast financial powers much like those once used by the de' Medici,

Rothschilds and Morgans to control nations.

One of the confounding aspects of bear market rallies is that the longer they last, the more likely

investors are to expect a correction, says Barron's Bob O'Brien.

Both dramas play high-stakes games with financial WMDs that have lethal consequences. Jack compresses

thrills, kills and chills into 24 hours. Hank, Goldman and their army of Wall Street mercenaries

move with equally blinding speed, heart-pounding action.

Drama? You bet. Six short months ago Hank led an assault on Congress. The scene parallels one

in "24:" Sangala War Lord Juma's brazen attack inside the White House. But no AK-47s necessary. The

Hammer assaulted Congress with just a two-and-a-half page memo in hand. Like a crack special-ops

warrior, he took down the enemy, demanding $750 billion, absolute control, total secrecy, no accountability

and emergency powers to act immediately ... warning that inaction was not an option, that collapse

of America's banking system was imminent, would bring down the global monetary system, pushing world's

economies into a "Great Depression II." Congress surrendered.

Here's the whole plot:

Scene 1. American government is now run by the 'Goldman Conspiracy'

Oh, you really think just I'm plotting a television series? Or just paranoid, exaggerating this

power grab? You better read "The Usual Suspects," Matthew Malone's brilliant article in Portfolio

magazine: He "exposed" the "Goldman Sachs 'conspiracy' to take over the U.S. financial system." Read

it in this context: America's financial sector has exploded from 19% of corporate profits in 1986

to 41% today, becoming a magnet for every wannabe billionaire. They know why Wall Street must control

Washington.

Malone focuses on the incestuous "conspiracy" of Goldman alumni in Treasury, Bank of America,

Merrill Lynch, AIG, Citigroup, Washington lobbyists and politicians.

Scene 2. Huge conflicts motivating Wall Street's 'Trojan Horse'

And just in case you think any emphasis on The Hammer's conflict of interest was invented purely

to increase drama, please remember that he worked at Goldman for three decades after serving under

Nixon. He got $38 million his last year as CEO in 2006 before becoming Treasury Secretary.

Then during the market meltdown six months ago the $700 million personal fortune he built at Goldman

was threatened by Goldman's huge $20 billion derivatives exposure at AIG: Suddenly his responsibilities

at Treasury merged with a strong self-interest in protecting his personal fortune. AIG was "saved."

Scene 3. Wall Street's 'quiet coup' also runs world's banking system

There's another equally disturbing expose in "The Quiet Coup," Simon Johnson's great article in

Atlantic magazine. A former chief economist at the International Monetary Fund, Johnson also warns

that America's "financial industry has effectively captured our government" and is "blocking essential

reform."

Worse, he says that unless we break Wall Street's stranglehold (unlikely in the new Washington)

we will be unable "to prevent a true depression," warning that "we're running out of time," echoing

many of our predictions of the "Great Depression II" coming soon.

See previous Paul B. Farrell.

Scene 4. Wall Street used the meltdown to take over America's government

Matt Taibbi, author of "The Great Derangement," captured this drama in a Rolling Stone piece,

"The Big Takeover, how Wall Street insiders are using the bailout to stage a revolution." A must-read:

"As complex as all the finances are, the politics aren't hard to follow. By creating a crisis that

can only be solved by those fluent in a language too complex for ordinary people to understand, the

Wall Street crowd has turned the vast majority of Americans into non-participants in their own political

future. ... in the age of CDS and CBO, most of us are financial illiterates."

Wall Street "used the crisis to effect a historic, revolutionary change in our political system

-- transforming a democracy into a two-tiered state, one with plugged-in financial bureaucrats above

and clueless customers below."

Scene 5. How Obama is keeping alive Bush's 'disaster capitalism'

Back in 2007 at the start of the meltdown, Hank was misleading us in Fortune: "This is far and

away the strongest global economy I've seen in my business lifetime." In the real world, Naomi Klein,

author of "The Shock Doctrine: Rise of Disaster Capitalism," was warning us that "during boom times

it's profitable to preach laissez faire, because an absentee government allows speculative bubbles."

But "when those bubbles burst, the ideology becomes a hindrance and goes dormant while big government

rides to the rescue." Then, free-market "ideology will come roaring back when the bailouts are done.

The massive debts the public is accumulating to bail out the speculators will then become part of

a global budget crisis." TARP paybacks: Obama has a new "disaster capitalism."

Scene 6. Wall Street's CEOs rule like dictators in a banana republic

Seriously, here's how bad Taibbi sees it: "Paulson and his cronies turned the federal government

into one gigantic half-opaque holding company, one whose balance sheet includes the world's most

appallingly large and risky hedge fund, a controlling interest in a dying insurance giant, huge investments

in a group of teetering megabanks, and shares here and there in various auto-finance companies, student

loans, and other failing business."

And let's include $5.5 trillion in Fannie Mae and Freddie Mac. Wall Street's greed and stupidity

resembles the self-destructive reigns of banana republic dictators.

Scene 7. Wall Street makes an un-American bet on 'disaster capitalism'

Today as you ponder buying some Goldman stock, remember, you're really betting that "disaster

capitalism" is back, strong, tightening its stranglehold on Washington and on the American taxpayers,

who will guarantee all Wall Street's future failures. Yes, this is un-American, but so what?

The "Goldman Conspiracy" is still probably a good short-term buy ... if you're interested in betting

on America's new "democracy of capitalists, by capitalists, and for capitalists," with "The Conspiracy"

leading the joint chiefs of this new mercenary army ... and it only took six short months for their

"Quiet Coup!"

Scene 8. Banks recycle TARP money, pump earnings, cheat America

Here's how it worked: The Hammer conned a clueless Congress, then shelled out $350 billion of

our taxpayer money (Helicopter Ben Bernanke helped by upping the ante with a couple trillion side-bet),

buying toxic debt to save his ol' Wall Street buddies. They stopped lending and used the dough to

doctor their balance sheets.

So no surprise that Goldman, Wells Fargo and J.P. Morgan Chase are now reporting "blockbuster"

first-quarter earnings, says the New York Times, while just months ago "many of the nation's biggest

banks were on life support."

Get it? They screwed taxpayers and borrowers so they can repay TARP with (you guessed it) our

recycled TARP money. Now it's back to business-as-usual, with no restrictions on CEO pay and bonuses

... no thank-yous ... no admissions of guilt ... while some even arrogantly deny that they ever needed

TARP money.

Scene 9. Wall Street's already set the stage for new disaster

Right after the election in November, at the peak of the banking crisis, when Hank, Goldman and

the Wall Street mercenary armies were divvying up the $350 billion TARP money, we detailed

30 reasons for the "Great Depression II" likely coming around 2011. We quoted John Whitehead,

former Goldman Sachs chairman, former chairman of the New York Fed, former Reagan deputy secretary

of state. He warned America's problems will take years, burn trillions, result in massive deficits:

"This is a road to disaster," he said. "I've always been a positive person and optimistic, but

I don't see a solution here." He did see a depression at the end of that road, one you can call the

"Great Depression II."

Scene 10. Obama turned 'The Goldman Conspiracy' into a superpower

Do you see the parallels: Jack and Starkwood, Hank and Goldman? Jack's a great mythic hero. We

need to believe a hero will defend the little guy, stand between us and total annihilation. But Jack

Bauer's "dead." Yes, dead. Jack's not real. Never was "alive." Jack's a fiction, a figment of Main

Street America's vivid imagination, the symbol of "hope" for a populist revolution. Hope that Jack,

Barack or some other new hero will emerge, take power back from Wall Street and return it to the

people.

Unfortunately that won't happen, folks. Yes, on TV Jack will come back from near-death, again.

But in real life, Hank, Goldman and Wall Street's mercenaries are winning the war. Read and weep

Portfolio's chilling finale: "Obama's victory and Geithner's appointment are the completion of Goldman's

meticulously crafted plan to become a superpower. The firm now has the clout to impose its will on

the financial markets, and the world."

GOP or Dems? Conservatives or liberals? It doesn't matter.

We'll all controlled by "The Conspiracy." So why not surrender, let them have the power? The truth

is, through their lobbyists and surrogates in Washington, they already rule America. Surrender is

a mere formality.

Accept reality. Hold them accountable later. After the next crisis. After the next meltdown of

disaster capitalism -- if there's anything left after the "Great Depression II" sweeps like a pandemic

across the planet, consuming all economies, for a long time. But for now, Goldman and other banks

may well be short-term buys. Just be ready to dump them in the near future ... a scenario that will

be here sooner than you think.

"Why does the US use the winter storm as the excuse every time?" Shu Bin, director of the

State Grid Beijing Economics Research Institute, told the Global Times on Thursday, noting

that the power grid system is very vulnerable and requires constant maintenance and

upgrade.

A report from the US Department of Energy (DOE) in 2015 said that 70 percent of power

transformers in the country were 25 years or older, 60 percent of circuit breakers were 30

years or older, and 70 percent of transmission lines are 25 years or older. And the age of

these components "degrades their ability to withstand physical stresses and can result in

higher failure rates," the report noted.

[...]

"The US has no nationwide power grid network allocation plan like China. When it

encounters extreme weather, a state won't help another state like some Chinese provinces

and regions do with flexible allocation plans," Lin Boqiang, director of the China Center

for Energy Economics Research at Xiamen University, told the Global Times on Thursday.

[...]

"China uses 50Hz across the country, like the country has the same heartbeat," he said,

adding that China has never experienced such a scale of blackouts as the US.

[...]

China has mastered the top technologies such as "UHV transmission" and "flexible DC

transmission" and started the strategic "west-east electricity transmission" and

"north-south electricity transmission" projects, which in turn offer an opportunity for the

development of the country's western region.

Not as apocalyptic as it may seem. I wrote a comment on the situation in the earlier

thread

here .

Temps are starting to move up and tomorrow (Thursday) should begin the thaw. Friday is

sunny and 47 deg F for a high, then sunny weekend and following. So we're over the worst of

it. The lowest it ever got was around 0 deg F.

The infrastructure failed - the people paid to manage this failed - everybody is angry, 10

people died so far last I heard.

Rolling blackouts, some people very much suffering, townships opening warming shelters -

probably not millions of pipes bursting. Not totally iced in, just nowhere to go. People

stayed home. Businesses stayed closed. Not totally without food, people stocked up staples in

2020.

Not that dire. Absolutely fucking disgusting, and a hardship that touched everyone - some

people got really screwed and I don't know why the treatment was uneven like that - not

demographics, something with the grid. Dire, yes, and life-threatening to some or perhaps

many (numbers not clear to me yet), but not so dire as your picture suggests. Nothing like

Katrina, except the same ineptness.

But heads will roll. The governor has mandated an investigation into the regulator, ERCOT.

What follows next is of great interest. Facts will appear. I'll post anything useful.

I heard a rumor it was getting better. Could be less blackouts. Will post now in case

power goes off ;)

This Texas debacle may light a heated debate in the USA for the next weeks, for two

reasons:

1) Texas is the big alt-right/Trumpist Festung for the foreseeable future. Their

nation-building process involve catapulting Texas as the anti-California ,

the conservative version of the Shining City on the Hill, around which the USA will be

rebuilt;

2) What is happening in Texas right now goes directly to the heart of neoliberalism, which

is the political doctrine that vertebrates the alt-right. That's why conservative ideologues

such as Tucker Carlson et al are desperately scrambling on TV and social media to blame the

outage on the so-called Green New Deal.

What is happening right now in Texas, therefore, may be another episode on the battle for

the soul of the American Empire.

LYNN FRIES : This newsdoc explores the folly of expecting private enterprise to

operate in the service of the public interest on a grand scale, globally, in key fields:

Financing the United Nations 2030 Agenda and Sustainable Development Goals, Climate change,

Health, Digital cooperation, Gender equality and the empowerment of women, Education and

skills. Specifically, it explores the United Nation's Strategic Partnership Agreement with the

World Economic Forum. The agreement was signed by the Office of the UN Secretary-General and

Executives of WEF, the World Economic Forum better known as DAVOS, a leading proponent of

public-private partnerships and a multistakeholder approach to global governance.

The United Nations as the world's intergovernmental multilateral system should always focus

on protecting common goods and providing global public benefits. That's the position of

signatories of an Open Letter sent to the UN Secretary-General by hundreds of civil society

organizations from all regions of the world. The letter states: "This public-private

partnership will permanently associate the UN with transnational corporations, some of whose

essential activities have caused or worsened the social and environmental crises that the

planet faces. This is a form of corporate capture". The letter calls on the Secretary-General

to terminate the Agreement.

I met up with Harris Gleckman to get his take on all this. Harris Gleckman is the author of

"Multistakeholder Governance and Democracy: A Global Challenge" and is currently working on a

handbook on the governance of multistakeholderism. Harris Gleckman is a Senior Fellow at the

Center for Governance and Sustainability, UMass Boston. We go now to our featured clips of that

meeting.

LYNN FRIES : Civil society is calling the World Economic Forum-UN Agreement as a

corporate takeover of the UN.

HARRIS GLECKMAN: The UN Charter starts with the words "We the Peoples". What the

Secretary-General is doing through the Global Compact and now through the partnership with the

World Economic Forum is tossing this out the window. He is saying: I'm going to align the

organization with a particular structural relationship with multinationals, with

multistakeholderism, and set aside attention to all the different peoples of the world in their

particular interests of environment, health, water needs and really talk about how to govern

the world with those who have a particular role in creating problems of wars from natural

resources, of creating problems relating to climate, creating problems relating to food supply

and technologies. That is undermining a core element of what the United Nations has been and

should be for its next 75 years.

LYNN FRIES : It's striking that the Agreement was signed as the UN is celebrating 100

years of multilateralism, the centenary year 1919 to 2019. And next year 2020 will mark the

1945 signing of the UN Charter 75th anniversary.

HARRIS GLECKMAN : Lynn, if I could give you an overview of what I'm concerned about

the aspect of this about multistakeholderism is that the Secretary-General is the leading

public figure for the multilateral system, the intergovernmental system. The World Economic

Forum is the major proponent or one of the major proponents that a multi-stakeholder governance

system should replace or marginalize the multilateral system. So the Secretary-General is

taking steps to just jump on the bandwagon of multistakeholderism without a public debate about

the democratic character of multistakeholderism, about a public debate about whether this is

effectively able to solve problems, without a public debate about how stakeholders are selected

to become global governors or even a public debate about what role the UN should have with any

of these multistakeholder groups.

LYNN FRIES : I noted that the letter that was sent to the UN Secretary-General was

also copied to the President of the General Assembly, the President of the Security Council and

the Chair of the G77 with a request that it be circulated to all Governments as an Official

Document.

HARRIS GLECKMAN : The Secretary-General should have gone to the intergovernmental

process to debate this issue and now civil society is saying to the intergovernmental process:

If the Secretary-General isn't going to tell you about it, we want you to have that debate

anyway.

LYNN FRIES : In addressing the UN Secretary-General the letter by Civil Society

Organizations recognized that the Secretary-General faced serious challenges.

HARRIS GLECKMAN: Yes it is absolutely the case that the Secretary-General is caught

in a very difficult bind. Governments are not able to collect and are not collecting their

taxes from the bulk of international business activities because of movements around tax

havens. Government's say: well we don't have the money, so we cannot underwrite an effort to

have a credible global governance system and this is affecting the operation of the UN. So the

Secretary-General is looking at a challenge. He has the financial challenge: under payment of

current dues and underfunding of the whole organization and an aggressive effort by the Trump

administration to deconstruct all the organizations of the international system in a period

Lynn where as you observed it's the hundredth year of multilateralism and the 75th year of the

United Nations. And here the Secretary-General has two major crises on his hands in terms of

the integrity of the system.

LYNN FRIES: Briefly give us some context on what you see as the motivation of the

World Economic Forum.

HARRIS GLECKMAN : The World Economic Forum's motivation for joining, for perhaps,

even driving forward this idea of a strategic partnership came from their work following the

financial crisis starting n 2008-09. Davos, the common name for the World Economic Forum,

convened 700 people working for a year and a half on a project that they called Global Redesign

Initiative. They created that project because they realized that the whole public view about

globalization as "a good for the world" was crumbling as a result of the financial crisis. And

so they wanted to propose a new method of governing the world. And two of the elements of their

proposal – that's actually a 700 page research paper – were to have a new

relationship with governments in the United Nations system and to advocate that the global

problems of the world should be solved by multistakeholder groups. This new partnership with

the Secretary-General is an implementation of what they laid out in their Global Redesign

Initiative to have a special place in the United Nations system for corporations to influence

the behavior of the international organizations. And also for those corporations to be able to

say to other people: Look we're in partnership with the United Nations so treat us as if we

were neutral friendly bodies.

Let me just share with you a couple of examples that may help convey how serious that is.

The Sustainable Development Goals were negotiated by governments in open sessions and they

determined what the goals should be in 17 areas. Multistakeholder groups have announced that

they are going to implement Goal 8 or Goal 6. And in the process, they declare: Here is how we

will work on health, here's how we will work on education, here's how we will work on the

environment. And rewrite what is the outcome of the Sustainable Development Goals in their own

organizational interest. In some ways, that's not surprising. You bring together a group of

companies, selected governments, selected civil societies, selected academics and they will

have their own internal dynamic of concern. But what they do is they assert that what they are

doing- their rewritten version- actually they are telling the world: Well, we are actually

doing the UN version. But that is not what their text is.

For example, in the energy field, in the energy goal there are five key adjectives that

describe the target about global energy needs. The leading multistakeholder group, Sustainable

Energy for All, their target has four of those adjectives and they drop the one which was

AFFORDABILITY. This is how the process of multistakeholders taking over an area, redefining it

but to the public announcing that they are implementing the intergovernmental goals is an

unhealthy development in global governance.

LYNN FRIES : The Civil Society letter referred to the Agreement as a public-private

partnership as did you in a recent OPED. Explain more about the public interest issue with

public-private partnerships.

HARRIS GLECKMAN : Well let's take a particular effort of a public-private partnership

in providing water in a city. Historically this is a public or a municipal function to make

sure that there is adequate amounts of water. The quality of water is healthy and its safety.

And that it's regularly and reliably available to the residents in the area. When a

public-private partnership comes in, the corporate side may have an interest in some of these

goals but add an additional one. That is they want a return on their investment, they want a

profit from it. So some of the items of those various public functions – access, quality

of material of water, reliability of water, access to all people then gets suddenly changed. So

if there's a manufacturing facility in one part of town more water may be diverted in that

direction. If water purification is a little hard about a particular element: We may get a

little lazy about doing that in the interests of profits. If it's going to take a lot of work

to dig up a street and replace pipes, they'll say: Well, we can wait another five years and use

those pipes which may have lead in them. All because now you add the fact that this

public-private partnership needs to make a return of profit on what should be, what

historically has a public municipal function. So you create this unequal development in terms

of meeting public needs against the now new requirement that if you want a water system, you

have to produce a profit for some of the actors involved.

LYNN FRIES : Food security is a major issue for vast populations. Comment on the

implications for food security.

HARRIS GLECKMAN : If we want to build, recover, create a food secure world, you need

to work with those who are growing, producing foods directly. Not those who are processing,

distributing, marketing, rebranding. We need to start at the very base and create a system of

engagement with small farmers, with small fishing families, with those around the world who are

the actual food producers. Who have been preserving knowledge and building knowledge for

centuries, they received that knowledge from centuries. That's the direction that would change

the way in which we could actually look at the issues of hunger and food security in the world

in a quite different fashion. Going to those who have a profit-centered motive in global

governance will sharply narrow what might be possible to do. That's what the partnership will

tend to do as the Secretary General and WEF have private discussions about how do we address

the issue of food security while not talking very loud about how we make a profit in that

process.

LYNN FRIES : If the UN Secretary-General invited you for a 1:1 what would you

say?

HARRIS GLECKMAN : I think that I would say to the Secretary-General that he needs to

give a major re-examination of the way the United Nations works with all of the peoples of the

world. In order to provide a stronger base for the United Nations, the doors have to be made

wider so that the views of various popular bodies, social movements, communities around the

world have far greater access to the United Nations. I'd also say to him. Mr. Secretary

General, the UN needs an open and clear conflict of interest policy and a conflict of interest

practice. For those multinationals who are causes of problems, who aggravate the global

problems of inequality we need and you as Head of the United Nations need to separate the

United Nations from that process. They should not be invited to attend meetings. They should

not be allowed to make statements. In the climate area, those who are continuing to extract

natural resources from the ground where they should stay we have taken too much of carbon out

of the ground. If we're going to meet the Paris Accord, they should have no role entering the

United Nations. I'd also say to the Secretary General that he needs to establish a much bigger

office to support civil society. At the moment, the UN support for civil society organization

institutional support is about two people. That is absolutely the wrong level of engagement

with the wider elements of civil society. And the last thing I would probably say to the

Secretary-General is that the UN is very proud of having developed a system of internal

governance that protects the weaker countries, the smaller countries, that their views can be

heard in the intergovernmental governance process. The Secretary-General should not engage with

multi stakeholder groups who do not have a rulebook that allows for the protection of smaller

members of the group, that does not have a way to appeal and challenge decisions that does not

require public disclosure of their finances, all of those characteristics of

multistakeholderism. The Secretary General should have and the UN should have no relationship

with those who are not interested in protecting core concepts of democracy

LYNN FRIES : We have to leave it there. Special thanks to our guest contributor,

Harris Gleckman, and thank you for watching and for your interest in this segment of

GPEnewsdocs coming to you from Geneva, Switzerland.

The WEF and its various constituencies try to overtake control of development with their

"public-private partnership" flag but how these, let's say, partnerships, actually work and

interact with local communities and governments is an issue that need to attract more

scrutiny and transparency. If one uses the migratory pressure as a measure, so far,

development in Africa, South America and South Asia is not doing a good job on the part of

local communities. There may be a few success cases, as it seems to be the case that

deforestation in Brazil that while proceeding it's way, has somehow slowed down compared to

the last decade of the XXth century. But when a success story is analysed what you find

behind is simply strong government action as the Brazilian did starting in 2004 when they

begun the monitoring of development in the Amazon basin and expanded in 2006 with a

moratorium in soya culture and beef production. The WEF has a series of initiatives on what

they call sustainable development that sound excellent in their web pages but in reality do

not seem to work so well and the UN should be kept independent and legally above of the WEF

initiatives to monitor development and accountability. This initiative will almost certainly

result in foxes governing henhouses.

As I see it the WEF makes the hell of a good PR job without counterbalancing parties.

Truly scary stuff and why does it remind me of the way public transport was destroyed in

the US: step 1 – starve it of revenue; step 2 – privatize it (while promising

better service); step 3 – let it rot; and step 4 – close it down (responding to

the public, gripping about how bad the service had become). The job accomplished!

One has to wonder what the Sec. General has been smoking lately and where are Russians and

Chinese to push back?

The UN will never accomplish its mission, man is incapable of bringing about world peace.

The UN is here for one reason and one reason only and that is to destroy the false religious

system when the political rulers hand it their power to accomplish just that.

If WEF is looking at doing infrastructure on a global scale that is based on good science,

is sustainable and maintainable, the ultimate power over the "multi-stakeholder groups"

submitting their bids to the UN should be the UN – this means a new UN mandate that

must be ratified yearly by voters, and bureaucrats that must win elections. If this big idea

is going to accomplish what needs to be done the "stakeholders" might want to take a close

look at what happened to the dearly departed ideas of neoliberalism. Neoliberalism was

destroyed from within by the need for ever more profit; by the" rat-race to the bottom" and

by externalizing costs in the form of pollution – by the most obviously unsustainable

practices, both social and environmental. If the goal is clear and comprehensive all these

problems inherent in yesterday's capitalism will have to be addressed at the get-go. It is a

difference of scale whether a city hires a contractor to do new waterlines, or the UN hires

"multi stakeholder groups" to do some continent-wide 50 year project. That means the UN will

need to become answerable to the people for the management of all these big ideas. Because

conflict of interest will be so massive as to be unmanageable otherwise. And one definition

will be imperative – Just what stake or stakes is/are held by "multi-stakeholder

groups"? Because what is at stake is the planet itself. Not money.

The UN problem has always been money. The 200 nation states are dilatory in paying their

dues. This gives the few rich countries power – 'cooperate with us and we'll fund your

activities.' Its not as bare-faced as I state it but you get the picture. To solve this

problem we need the majority of countries to vote to make national dues a precedent claim on

each government. Publish the result of the vote and monthly progress towards the aim. Name

the countries cooperating.

Once the UN administration is confident of its income it can plan its activities better,

make peoples' health and livelihoods a priority and achieve a much higher profile amongst

humanity.

"Mining transnationals find it cheaper to buy water rights than to desalinate seawater and

transport it for tens or hundreds of kilometers. Even more so if they have to use less

polluting but more expensive desalination technologies.

This is an unequal and unjust war where the main victims are the poor population, small

farmers and the sustainable development of our region of Atacama.

We continue to approve and facilitate the approval of mining projects and mega-projects

without making it a condition not to consume water from the basin.

– The population of Copiapó, Caldera, Tierra Amarilla and Chañaral,

particularly the lower income population, suffers the consequences of having to endure

repeated supply cuts, low pressure and a terrible quality of drinking water.

The drinking water crisis in the mentioned cities is a direct consequence of the over

exploitation of the Copiapó river basin by foreign mining companies, of the

purchase-sale and speculation with water rights, as well as of the irrationality and

indolence of the State in not establishing priorities in the use of the vital water" https://www.youtube.com/watch?v=8lGEONBfvTM

Although corporate meddling is not unheard of in the UN system, under the new terms of the

UN-WEF partnership, the UN will be permanently associated with transnational corporations. In

the long-term, this would allow corporate leaders to become 'whisper advisors' to the heads

of UN system departments.

The UN system is already under a significant threat from the US Government and those who

question a democratic multilateral world. Additionally, this ongoing corporatization will

reduce public support for the UN system in the South and the North, leaving the system, as a

whole, even more vulnerable.To prevent a complete downfall, the UN must adopt effective

mechanisms that prevent conflicts of interest consistently. Moreover, it should strengthen

peoples and communities which are the real human rights holders, while at the same time build

a stronger, independent, and democratic international governance system.

There is a strong call to action going on by hundreds of organizations against this

partnership agreement http://bit.ly/33bRQZP

"... As Hudson points out, WW1 was a coup for the USA's financial sector and allowed them to gain control of academia to erase Marx and his Classical Economist allies and replace them with their own toadies along with their newly formed product--Propaganda and the nascent Police State, which the institution of Prohibition greatly facilitated. ..."

The latest by Crooke I found a curious read since he bases his article on his interpretation

of Adam Tooze's books about the world wars, neither of which I've read. Curious because we

know from Hudson that the counterrevolution by the Feudal Lords of banking and land holding

against Classical Economists and their political allies began in earnest well before then in

@1870 and that their Race for Africa was a big part of their efforts to regain their hold on

their home governments.

Within the USA, a similar revolution was being waged although it began several decades

later in response to the Populists.

As Hudson points out, WW1 was a coup for the USA's financial sector and allowed them

to gain control of academia to erase Marx and his Classical Economist allies and replace them

with their own toadies along with their newly formed product--Propaganda and the nascent

Police State, which the institution of Prohibition greatly facilitated.

I wrote the above to provide barflies with a contrasting historical context much of which

was recently reviewed via all the Marxian discussion and where the actual roots of

Neoliberalism are seated.

Deep at the core is the battle by Banksters and their allies to keep their institutions

private versus the Classical and Populist goal of making them public utilities and how the

World Wars helped the former to gain their goals.

Tooze's narrative seems okay on the surface, and it clearly fooled Crooke, but it's

incomplete. What did the European Powers run out first that generated WW1's stalemate? Money

for arms as posited or human bodies to man those arms? In George Seldes's censored interview

with Hindenburg a week after the Armistice, published in You Can't Print That! ,

the defeated Field Marshal admitted it was the entry of American Men--human numbers--that

turned the tide and made it clear to him that the war couldn't be won. Sure, money helped get

the doughboys over there, but before they arrived masses of money were sent in both

directions that didn't change the balance other than to create the unpayable postwar debts

the Americans demanded be paid.

karlofi@103

Hindenburg realised that the manpower resources of the US were crucial, though they hardly

came into play on the battle field. But it was US raw materials, combined with the British

blockade, that were the crucxial factor.

With the US the Alliance was simply, even minus Russia, too big, too powerful. And then

there was the military reality that the Allies were beginning to organise themselves on the

battlefield: including tanks etc.

As for the "Feudal Lords of Banking..." Hudson is a great resource, but his theory sounds

wrong to me.

When I first happened across Seldes's interview and knowing the "stabbed in the back"

claim that Hitler used in his rise to power, I was very curious as to why it was

censored--what possible reason could be claimed to withhold such an important set of

revelations? Clearly as Seldes himself says, if it had been published at the time, the entire

course of subsequent history would likely have taken a different direction. Are you familiar

with Seldes? He was I.F. Stone's idol and model with a penchant for truth-telling regardless

of the subject or people involved. The book I linked to is filled with similar stories that

contradicted the current narrative being sold to the masses, and his subsequent works are

similar. But as you might guess, few people have ever heard of him or his writings.

Given what Hudson reveals about the manipulation of the learning/teaching of

political-economy, it would be very wise to suspect much of what was/is produced via the

"social sciences," (history written by the victors) which is why my collegiate mentor

stressed the learning methodology he devised to try and arrive at the best non-subjective

conclusion as possible whatever the inquiry--to try and duplicate as closely as possible the

scientific method for confirmation of theories. I've discovered quite a lot of metaphysics

within the entire spectrum of social science disciplines that's made me question a vast

catalog of assumptions. As Fischer and other historians have discovered, historical truth

often lies literally in the margins--the annotations--made by decision makers or obscure

signals reports filed away within deep archives or forensic chemical reports detailing what

is or isn't present within the samples. The learning of the revealed truths can be painful,

making the adage Ignorance is Bliss rather powerful and enticing. But that's not for me as I

subscribe to the alternative adage, The Truth will set you Free.

I'm just reading Keen's 2nd Edition of his Debunking Economics: The Naked Emperor

Dethroned? where he writes on page 29: "[...], conventional Marxsim is as replete with

logical errors as is neoclassical economics, even though Marx himself provides a far better

foundation for economic analysis than did Walras or Marshall."

To my knowledge, Keen refers to himself as a Post-keynesian economist (not to be confused

with bastardized Keynesian or central banks' Neo-Keynesian economics), highly influenced by

the work of Hyman Minsky who learned under Schumpeter.

Unemployment benefits currently are usually is just six month or so; this is the time when you can plan you "downsizing". You do

not need to rush but at the same time do not expect that you will get job offers quickly, if at all. Usually it does not happen.

many advertised positions are fakes, another substantial percentage is already reserved for H1B candidates and posting them is the

necessary legal formality.

Often losing job logically requires selling your home and moving to a modest apartment, especially if no children are living with

you. At 50 it is abut time... You need to do it later anyway, so why not now. But that's a very tough decision to make... Still, if the current housing market is close to the top

(as it is in 2019), this is one of the best moves

you can make. Getting from your house several hundred thousand dollars allows you to create kind of private pension to compensate for

losses in income till you hit your Social Security check, which currently means 66.

$300K investment in A quality bonds that returns 3% per year is enough to provides you with $24K per year "private pension" from 50 to

age of 66 when social security kicks in. That allows you to pay for the apartment and amenities. The food is extra but with this

level of income you qualify for food assistance.

This way you can take lower paid job, of much lower paid job (which mean $15 per hour), of temp job and survive.

And if this are many form you house sell your 401k remains intact and can supplement your SS income later on. Simple Excel spreadsheet can provide you with

a complete picture of what you can afford and what not. Actually the ability to walk of fresh air for 3 or more hours each day worth a lot

of money ;-)

Notable quotes:

"... Losing a job in your 50s is a devastating moment, especially if the job is connected to a long career ripe with upward mobility. As a frequent observer of this phenomenon, it's as scary and troublesome as unchecked credit card debt or an expensive chronic health condition. This is one of the many reasons why I believe our 50s can be the most challenging decade of our lives. ..."

"... The first thing you should do is identify the exact day your job income stops arriving ..."

"... Next, and by next I mean five minutes later, explore your eligibility for unemployment benefits, and then file for them if you're able. ..."

"... Grab your bank statement, a marker, and a calculator. As much as you want to pretend its business as usual, you shouldn't. Identify expenses that don't make sense if you don't have a job. Circle them. Add them up. Resolve to eliminate them for the time being, and possibly permanently. While this won't necessarily lengthen your fuse, it could lessen the severity of a potential boom. ..."

Losing a job in your 50s is a devastating moment, especially if the job is connected to a long career ripe with upward mobility.

As a frequent observer of this phenomenon, it's as scary and troublesome as unchecked credit card debt or an expensive chronic health

condition. This is one of the many reasons why I believe our 50s can be the most challenging decade of our lives.

Assuming you can clear the mental challenges, the financial and administrative obstacles can leave you feeling like a Rube Goldberg

machine.

Income, health insurance, life insurance, disability insurance, bills, expenses, short-term savings and retirement savings are

all immediately important in the face of a job loss. Never mind your Parent PLUS loans, financially-dependent aging parents, and

boomerang children (adult kids who live at home), which might all be lurking as well.

When does your income stop?

From the shocking moment a person learns their job is no longer their job, the word "triage" must flash in bright lights like

an obnoxiously large sign in Times Square. This is more challenging than you might think. Like a pickpocket bumping into you right

before he grabs your wallet, the distraction is the problem that takes your focus away from the real problem.

This is hard to do because of the emotion that arrives with the dirty deed. The mind immediately begins to race to sources of

money and relief. And unfortunately that relief is often found in the wrong place.

The first thing you should do is identify the exact day your job income stops arriving . That's how much time you have

to defuse the bomb. Your fuse may come in the form of a severance package, or work you've performed but haven't been paid for yet.

When do benefits kick in?

Next, and by next I mean five minutes later, explore your eligibility for unemployment benefits, and then file for them if

you're able. However, in some states severance pay affects your immediate eligibility for unemployment benefits. In other words,

you can't file for unemployment until your severance payments go away.

Assuming you can't just retire at this moment, which you likely can't, you must secure fresh employment income quickly. But quickly

is relative to the length of your fuse. I've witnessed way too many people miscalculate the length and importance of their fuse.

If you're able to get back to work quickly, the initial job loss plus severance ends up enhancing your financial life. If you take

too much time, by your choice or that of the cosmos, boom.

The next move is much more hands-on, and must also be performed the day you find yourself without a job.

What nonessentials do I cut?

Grab your bank statement, a marker, and a calculator. As much as you want to pretend its business as usual, you shouldn't.

Identify expenses that don't make sense if you don't have a job. Circle them. Add them up. Resolve to eliminate them for the time

being, and possibly permanently. While this won't necessarily lengthen your fuse, it could lessen the severity of a potential boom.

The idea of diving into your spending habits on the day you lose your job is no fun. But when else will you have such a powerful

reason to do so? You won't. It's better than dipping into your assets to fund your current lifestyle. And that's where we'll pick

it up the next time.

We've covered day one. In my next column we will tackle day two and beyond.

Peter Dunn is an author, speaker and radio host, and he has a free podcast: "Million Dollar Plan." Have a question for Pete

the Planner? Email him at [email protected]. The views and opinions expressed in this column are the author's and do not

necessarily reflect those of USA TODAY.

Only the greedy, selfish, well off, egotistical and share holders believe that Public

Services should, could and would benefit from privatisation and deregulation.

Education and Health for example are (in theory) a universal right in the UK. As numbers

in the population rise and demographics change so do costs ie delivery of the service becomes

more expensive.As market force logic is introduced it also becomes less responsive - hence

people not able to get the right drugs and treatment and challenging and challenged young

people being denied an education that is vital for them in increasing numbers.

Meanwhile - as Public Services are devalued and denuded in this system the private sector

becomes increasingly wealthy at the top while its workers become poorer and less powerful at

the bottom.

With the introduction of Tory austerity which punishes the latter to the benefit of the

former there is no surprise that this system does not work and has provided a platform for

the unscrupulous greedy and corrupt to exploit Brexit and produce conditions which will take

'Neoliberalism' to where logic suggests it would always go - with the powerful rich protected

minority exerting their power over an increasingly poor and powerless majority.

The competitive tender approach ensures the cheapest bids get the contracts and the cheapest

bids are those most likely to employ exploited labour and cheap materials as well as cutting

corners. Result? a job of sorts gets done, but the quality is rubbish, with no investment or

pride in the product. Look at Hong Kong where this is longstanding practice: new tunnel, half

the extractor fans do not work correctly because they were poorly installed. I once spoke to

the Chief Engineer of the Tsing Ma bridge, he was stressed out of his socks for the whole

construction period trying to monitor all the subcontractors who had bid so low they had to

cheat to make a profit with the result that they would try to cut corners and avoid doing

things if they thought they could get away with it. Good job that engineer was diligent.

Others may be less able or willing.

BTW: I seldom find comparisons in UK-media to other countries when those countries are

better.

I think that's because most of the UK media is propaganda for the established system,

which they rely on for advertising revenue and access to information. If an outlet's

journalists start seriously questioning the existing system, a few things happen: 1.

the journo doesn't get promoted within the system; 2. their access to information is

curtailed (they are not invited to briefings etc., and; 3. advertising revenue drops. As the

business model of most mainstream media is to present consumer audiences to advertisers, this

is not going to sit well with the owners, see 1 and 2 above leading to poor evaluations. Any

journo with half a brain quickly learns this and fits in. Only so far and no further.

As a Tory for most of my longish life, I have to agree that whilst some things have

flourished once privatised, certain services must remain in public ownership and control to

enable governments to improve or reduce, depending on national taxation and expenditure - if

people want better services then they must be prepared to pay for them, and of course the

long-term pensions of the workforce. Managers should be subject matter experts before running

departments, not just accountants or management consultants, so they can improve delivery not

just constantly re-structure or carp on about 'efficiency savings'.

Having worked in shipping, that industry has oscillated several times but rail is an

interesting example - a disaster in the dying days of national ownership, the private world

started well improving safety, reliability and capacity but has gone downhill in recent

years, not helped by the track management system. Again, the airlines started well but now

several have gone into administration and BA has 'down-qualitied' itself to become one of the

worst.

Some parts of the NHS can be provided by private industry but limited to service provision

and collective buying only - certainly NOT cancer screening.

Then, when you look at private providers who go bust and completely fail to provide any

acceptable capability - jails, probation, social care etc. one wonders when, if ever,

politicians will realise that it costs them, the civil service and commercial management an

incredible amount of time, effort and cost just to fail!

Outsourcing government work is the most inefficient way of getting it done for the benefit of

taxpayers. When the profits private companies make from it are added to what economies must

invest to pay the taxes for it it's astonishing how popular it has become throughout the

world, something only explicable if those authorising it are amongst the most stupid of

financial administrators or the most corrupt.

Outsourcing for example £1m worth of work requires that amount to be paid in taxes,

which needs about £5m to be earned in wages and profits to pay £1m in taxes,

which in turn needs an investment of perhaps ten times that amount, when the £1m is

borrowed by debt laden governments to be repaid by over-borrowed and overtaxed economies.

If the outsourced company is not profit-making it will borrow the capital to be able to

deliver what's required and that in turn will raise the amount it will want for future work,

which is what I think accounts for Carillion and the other outsource giants going to the

wall.

The process is generally the fault of governments failing to adhere strictly to the necessity

of only paying its workforce on average the same as the private sector pays its workers,

which in democracies is not an unfair requirement demanded by equality legislation. Many

would claim that such was why Margaret Thatcher decided on privatising so many public

utilities especially after the miners' strike in Ted Heath's government and why it gained so

much support and popularity when wages and benefits for similar skill levels seemed so much

better and jobs more secure for many public sector workers involved than they were in the

private sector. Now of course, the high costs of private necessary public services are making

life unbearable for the majority of workers and welfare recipients while profits are going

abroad to those who own them and the EU in getting the flak – courtesy of the media -

for the resultant poverty and austerity, allowed the false £350m a week to win the

referendum. The £4 billion a week worth of exports to the EU paid most of that and the

way companies are relocating to hedge against Brexit means a lot of lost jobs will go with

them – some earlier estimates but it at more than 100,000 - which doesn't seem to deter

those determinedly wanting out of the EU one little bit.

This is a blessing for the low labour cost Member States, who being in the populous markets

the multinationals need, can attract the UK industries looking to further cut costs and

freight charges so those that go will never come back because higher costs in the Brexit UK

will not be compensated for easily with uncompetitive price hikes for EU customers, unlike

CAP payments that have been promised to farmers by the government proBrexit Minister.

The doom and gloom felt by many I think is well justified when sovereign debt and bank credit

is considered relative to taxes. While sovereign debt is regarded as an asset and future

taxes are acceptable for bank credit and both can be securitized by banking systems to borrow

even more capital that will be acceptable to central banks as QE, it's not surprising that

sovereigns don't need to worry about economies being unable to provide the taxes their

governments unlawfully spend even when leaving it for future generations is also unlawful

i.e. is a crime, since if they don't, their central banks and bond holders covered by them

will. When the cost in trillions since 2016 already spent by government in preparing for

Brexit is included one can't help but think that the financial economy has made a proverbial

killing from UK incorporated and now owns most if not all of it. If most of the finance for

Brexit came from its financiers and investors is it possible that after Brexit they'll pour

trillions back into the economy to make it capable of not only surviving but also competing

favourably with the EU, Japan, China, and the US?

I have to disagree. Hardly anything has flourished after privatisation. The big failures,

which get all the publicity, were generally basket case private businesses which had to be

nationalised to save them from collapse.

Sometimes they are stuffed with public money and

sold at a loss to the public, like the Tory nationalisation of Rolls Royce, or deprived of

funds like British Rail to provide an excuse to liberate thousands of square miles of real

estate

This latter is the scheme for the NHS with hospitals and other property provided at

great public expense sold off to any shark who says he has the money, and once it's private

load the enterprise with debt and walk away.

Unlike the privatisations of the 80s and 90s there's barely any pretence these days

that new sell-offs are anything more than simply part of a quest to find new avenues for

profit-making in an economy with tons of liquid capital but not enough places to profitability

put it.

Back in the Thatcher/Reagan years there were at people around who genuinely believed in the

superiority of the market, or at least, made the effort to set out an intellectual case for

it.

Now we're in a different era. After 2008, hardly anyone really believes in neoliberal

ideas anymore, not to the point that they'd openly make the case for them anyway. But while

different visions have appeared to some extent on both left and right, most of those in

positions of power and influence have so internalised Thatcher's 'there is no alternative'

that it's beyond their political horizons to treat any alternatives which do emerge as

serious propositions, let alone come up with their own.

So neoliberalism stumbles on almost as a reflex action. Ben Fine calls it a 'zombie' but I

think the better analogy is cannibalism. Unlike the privatisations of the 80s and 90s there's

barely any pretence these days that new sell-offs are anything more than simply part of a

quest to find new avenues for profit-making in an economy with tons of liquid capital but not

enough places to profitability put it. Because structurally speaking most of the economy is

tapped out.

Privatising public services at this point is just a way to asset strip and/or funnel

public revenue streams to a private sector which has been stuck in neoliberal short-term, low