|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

| “The Fed is now actively and directly engaged in the redistribution of wealth.” The problem is that it is the redistribution from the poorer to the richer. I have no problem with people becoming richer due to talent, hard work, or innovation, but people who can’t figure out that loans have to be paid back do not deserve to keep any of their bonuses or ill conceived salaries. The Fed has embarked upon a policy of affirmative action for the stupid. |

|

|

The term "regulatory capture" is a new term for "regulatory corruption" and refers to the subversion of regulatory agencies by the firms they regulate, not exclusively by money but by more subtle means such as revolving door policies, defunding those initiatives that run against to firms interests, changing legislation that effective emasculate the regulator, etc. This is to be distinguished from regulation that is intended by the legislative body that enacts it to serve the private interests of the regulated firms, for example by shielding them from new entry. Regulatory capture implies that the regulated firms unleashed the war on the regulatory agency and won it, turning the agency into their vassal.

How are we to judge the Federal Reserve? The Fed by its very nature has been a very opaque institution. The Fed was designed as a unique hybrid in which government would share its powers with the private banking industry. But recently it became more like agent of Wall street in government. All-in-all this is an extremely powerful, shadow organization, which after its politization by Greenspan looks not unlike Politburo of the CPSU of the USSR (which being a party body formally did not have either legislative or executive power at all).

|

|

The Fed Chairman is the highest unelected official on the country and may be No.2 in Washington power corridors in general (In some areas he is No.1 as he does have some influence on presidential elections and can help to defeat incumbent by increasing interest rates or help the current administration to say in power by slashing rates). What truly goes on behind the closed doors of the Fed? We don't know how sycophantic are the relationships amongst the Fed Chair and Fed governors, but indirect facts like Alan Blinder short tenure under Greenspan suggest that Feds power structure is authoritarian with all-powerful Fed chairman and under some chairmen has the distinct "cult of personality" bent. Again the structure not unlike the power structure of Soviet Politburo.

The working hypothesis is that the level of "cult of personality" really resembles the same for the position of the General Secretary of CPSU. Whatever are their personal feelings and beliefs members obligingly vote for the party line proposed by the Chairman. As Greenspan once put it, any open discord undermines the Fed influence. And he has a point, although the price to pay for the fake unity might be too high. Add to this hidden relationships between Fed Open Market Committee members and Wall Street titans and their political operatives...

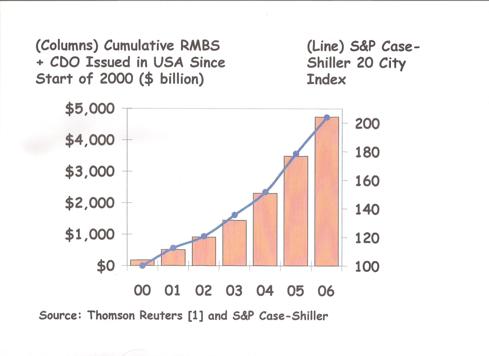

The financial sector has grown to be a larger part of the overall economy. The financial sectors share of credit (debt) has increased from 15% in 1974 to 41% in 2008. Consequently, the economy is now more vulnerable to the effects of a bursting credit bubble stemming from the financial sector. In other words hypertrofied financial secor is the source of systemic instability. And credit induced recessions are more severe than non-credit related recessions, such as the bursting of the high-tech bubble.

After allowing creation of banking oligopolies with their ability to distort markets, avoid competition, and corrupt politics and the regulatory system Fed became just a pawn in big game, member of the same banksters cartel. That means that Fed was not simply corrupted but it was corrupted to the core in true RICO sense.

By law, the Fed has a responsibility for the stability of the financial system and for maintain adequate reserves by the banks. Initial role of the Fed was more narrow: it was created in 1913 to provide temporary liquidity to banks to meet depositor withdrawals caused by financial panics. Fed liquidity enables banks to avoid selling assets in distressed markets where asset values might be temporarily impaired. The law allows the Fed to lend based on acceptable collateral, to otherwise solvent banks. Over time, a variety of tools have been added to fight financial panics, including FDIC insurance. Also Fed was given important regulatory functions aimed at preventing the excessive risk taking by taking too much debt (aka leverage) and maintaining too low capital levels which were one of the sources of Great Depression.

In Greenspan era the Fed has been criminally derelict in fulfilling its regulatory functions under the Federal Reserve Act, namely monitoring banking institutions to be sure the correct capital levels were being maintained. As a shrewd political operative and compulsive careerist Greenspan was mainly interested in his survival and playing the hand of bank oligopolies was a sure way to ensure his election and reelection.

In the current crisis Fed's actions departed from past responses in a number of important ways.

The size of the Fed commitment is directly related to the large credit share enjoyed by the financial sector. Fed intervention, in size and scope never before seen, has prevented the full effect of a natural downsizing that would have occurred with the bursting of the financial credit bubble. In some instances, financial firms have become bigger and more powerful. The owners of affected debt and some stockholders, are the primary beneficiaries of the bailouts. Bailouts have increased future deficits and potential taxes by unimaginable amounts. The economy’s exposure to financial sector crisis has increased.

The FED deepened the division between those perceived as less risky and those perceived as more risky with their minimum capital requirements based on perceived default risks. In most other aspects of social life such discrimination and profiling is prohibited.And this regulatory division is even more perverse in a recession when some triple-A rated clients are downgraded and the banks have to get new capital to cover these; and which mostly comes from stopping lending to those of which require even larger capital requirements. This is the most dangerous of all pro-cyclical effects of the Basel regulations, but also the most ignored.

|

|

Switchboard | ||||

| Latest | |||||

| Past week | |||||

| Past month | |||||

Mar 31, 2019 | www.nakedcapitalism.com

... ... ...Running in the background, though, was a new, darker theme: That the post-2008 reforms had gone too far in restricting policymakers' discretion in crises. The trio most responsible for making the post-Lehman bailout revolution -- Ben Bernanke, Timothy Geithner, and Henry Paulson -- expressed their misgivings in a joint op-ed :

But in its post-crisis reforms, Congress also took away some of the most powerful tools used by the FDIC, the Fed and the Treasury the FDIC can no longer issue blanket guarantees of bank debt as it did in the crisis, the Fed's emergency lending powers have been constrained, and the Treasury would not be able to repeat its guarantee of the money market funds.

These powers were critical in stopping the 2008 panic The paradox of any financial crisis is that the policies necessary to stop it are always politically unpopular. But if that unpopularity delays or prevents a strong response, the costs to the economy become greater.

We need to make sure that future generations of financial firefighters have the emergency powers they need to prevent the next fire from becoming a conflagration.

Sotto voce fears of this sort go back to the earliest reform discussions. But the question surfaced dramatically in Timothy Geithner's 2016 Per Jacobsson Lecture, " Are We Safer? The Case for Strengthening the Bagehot Arsenal ." More recently, the Group of Thirty has advanced similar suggestions -- not too surprisingly, since Geithner was co-project manager of the report, along with Guillermo Ortiz, the former Governor of the Mexican Central Bank, who introduced the former Treasury Secretary at the Per Jacobson lecture.

Aside from the financial collapse itself, probably nothing has so shaken public confidence in democratic institutions as the wave of bailouts in the aftermath of the collapse. The redistribution of wealth and opportunity that the bailouts wrought surely helped fuel the populist surges that have swept over Europe and the United States in the last decade. The spectacle of policymakers rubber stamping literally unlimited sums for financial institutions while preaching the importance of austerity for everyone else has been unbearable to millions of people.

Especially in money-driven political systems, affording policymakers unlimited discretion also plainly courts serious risks. Put simply, too big to fail banks enjoy a uniquely splendid situation of "heads I win, tails you lose" when they take risks. Scholars whose research INET has supported, notably Edward Kane , have shown how the certainty of government bailouts advantages large financial institutions, directly affecting prices of their bonds and stocks.

For these reasons INET convened a panel at a G20 preparatory meeting in Berlin on " Moral Hazard Issues in Extended Financial Safety Nets ." The Power Point presentations of the three panelists are presented in the order in which they gave them, since the latter ones sometimes comment on Edward Kane 's analysis of the European banks. Kane, who coined the term "zombie bank" and who famously raised early alarms about American savings and loans, analyzed European banks and how regulators, including the U.S. Federal Reserve, backstop them.

Peter Bofinger , Professor of International and Monetary Economics at the University of Würzburg and an outgoing member of the German Economic Council, followed with a discussion of how the system has changed since 2008. Helene Schuberth , Head of the Foreign Research Division of the Austrian National Bank, analyzed changes in the global financial governance system since the collapse.

The panel took place as public discussion of a proposed merger between two giant German banks, the Deutsche Bank and Commerzbank, reached fever pitch. The panelists explored issues directly relevant to such fusions, without necessarily agreeing among themselves or with anyone at INET.

But the point Robert Johnson, INET's President, and I made some years back , amid an earlier wave of talk about using public money to bail out European banks, remains on target:

We are only interested observers of the arm wrestling between the various EU countries over the costs of bank rescues, state expenditures, and such. But we do think there is a clear lesson from the long history of how governments have dealt with bank failures . [If] the European Union needs to step in to save banks, there is no reason why they have to do it for free best practice in banking rescues is to save banks, but not bankers. That is, prevent the system from melting down with all the many years of broad economic losses that would bring, but force out those responsible and make sure the public gets paid back for rescuing the financial system.

The simplest way to do that is to have the state take equity in the banks it rescues and write down the equity of bank shareholders in proportion. This can be done in several ways -- direct equity as a condition for bailout, requiring warrants that can be exercised later, etc. The key points are for the state to take over the banks, get the bad loans rapidly out of those and into a "bad bank," and hold the junk for a decent interval so the rest of the market does not crater. When the banks come back to profitability, you can cash in the warrants and sell the stock if you don't like state ownership. That way the public gets its money back .at times states have even made a profit.

In 2019, another question, alas, is also piercing. In country after country, Social Democratic center-left parties have shrunk, in many instances almost to nothingness. In Germany the SPD gives every sign of following the French Socialist Party into oblivion. Would a government coalition in which the SPD holds the Finance Ministry even consider anything but guaranteeing the public a huge piece of any upside if they rescue two failing institutions?

The full article of Edward Kane

WheresOurTeddy , March 29, 2019 at 11:49 am

Enforcement of financial laws is not our thing. Just ask Chuck Schumer of the #Non-Resistance:

https://theintercept.com/2019/03/28/sec-democratic-commissioner-chuck-schumer/

Louis Fyne , March 29, 2019 at 12:17 pm

There needs to be an asset tax on/break up of the megas. End the hyper-agglomeration of deposits at the tail end. Not holding my breath though. (see NY state congressional delegation)

To be generous, tax starts at $300 billion. Even then it affects only a dozen or so US banks. But would be enough to clamp down on the hyper-scale of the largest US/world banks. The world would be better off with lot more mid-sized regional players.

thesaucymugwump , March 29, 2019 at 12:17 pm

Anyone who mentions Timmy Geithner without spitting did not pay attention during the Obama reign of terror. He and Obama crowed about the Making Home Affordable Act, implying that it would save all homeowners in mortgage trouble, but conveniently neglected to mention that less than 100 banks had signed up. The thousands of non-signatories simply continued to foreclose.

Not to mention Eric Holder's intentional non-prosecution of banksters. For these and many other reasons, especially his "Islamic State is only the JV team" crack, Obama was one of our worst presidents.

chuck roast , March 29, 2019 at 12:21 pm

Thank you Yves and Tom Ferguson.

Fergusons graph on DBK's default probabilities coincides with the ECB's ending its asset purchase programme and entering the "reinvestment phase of the asset purchase programme".

https://www.ecb.europa.eu/mopo/implement/omt/html/index.en.html

The worst of the euro zombie banks appear to be getting tense and nervous.

https://www.youtube.com/watch?v=dKpzCCuHDVY

Maybe that is why Jerome Powell did his volte-face last month on gradually raising interest rates. Note that the Fed also reduced its automatic asset roll-off. I'm curious if the other euro-zombies in the "peers" return on equity chart are are experiencing volatility also.Craig H. , March 29, 2019 at 1:04 pm

Apparently the worst fate you can suffer as long as you don't go Madoff is Fuld. According to Wikipedia his company manages a hundred million which must be humiliating. It's not as humiliating as locking the guy up in prison would be by a very long stretch.

Greenspan famously lamented that there isn't anything the regulators can really do except make empty threats. This is dishonest. The regulations are not carved in stone like the ten commandments. In China they execute incorrigible financiers all the time.

John Wright , March 30, 2019 at 10:31 am

Greenspan was never willing to counter any problem that might irritate powerful financial constituencies. For example, during the internet stock bubble of the late 1990's, Greenspan decried the "irrational exuberance" of the stock market. The Greenspan Fed could have raised the margin requirement for stocks to buttress this view, but did not. As I remembered reading, Greenspan was in poor financial shape when he got his Fed job.

His subsequent performance at the Fed apparently left him a wealthy man. Real regulation by Greenspan may have adversely affected his wealth. It may explain why Alan Greenspan would much rather let a financial bubble grow until it pops and then "fix it".

Procopius , March 31, 2019 at 12:30 am

Everybody forgets (or at least does not mention) that Greenspan was a member of the Class of '43, the (mostly Canadian) earliest members of the Objectivist Cult with guru Ayn Rand. Expecting him to act rationally is foolish. It may happen accidentally (we do not know why he chose to let the economy expand unhindered in 1999), but you cannot count on it. In a world with information asymmetry expecting markets to be concerned about reputation is ridiculous. To expect them to police themselves for long term benefit is even more ridiculous.

rd , March 29, 2019 at 3:06 pm

I think Finance is currently about 13% of the S&P 500, down from the peak of about 18% or so in 2007. I think we will have a healthy economy and improved political climate when Finance is about 8-10% of the S&P 500 which is about where I think finance plays a healthy, but not overwhelming rentier role in the economy.

Inode_buddha , March 29, 2019 at 4:51 pm

I think things will be much better when finance is about ~3% of the S&P 500, but no more than that.

Mar 14, 2019 | jessescrossroadscafe.blogspot.com

"But the impotence one feels today -- an impotence we should never consider permanent -- does not excuse one from remaining true to oneself, nor does it excuse capitulation to the enemy, what ever mask he may wear. Not the one facing us across the frontier or the battle lines, which is not so much our enemy as our brothers' enemy, but the one that calls itself our protector and makes us its slaves. The worst betrayal will always be to subordinate ourselves to this Apparatus, and to trample underfoot, in its service, all human values in ourselves and in others."

Simone Weil

"And in some ways, it creates this false illusion that there are people out there looking out for the interest of taxpayers, the checks and balances that are built into the system are operational, when in fact they're not. And what you're going to see and what we are seeing is it'll be a breakdown of those governmental institutions. And you'll see governments that continue to have policies that feed the interests of -- and I don't want to get clichéd, but the one percent or the .1 percent -- to the detriment of everyone else...

If TARP saved our financial system from driving off a cliff back in 2008, absent meaningful reform, we are still driving on the same winding mountain road, but this time in a faster car... I think it's inevitable. I mean, I don't think how you can look at all the incentives that were in place going up to 2008 and see that in many ways they've only gotten worse and come to any other conclusion."

Neil Barofsky

"Written by Carmen Segarra, the petite lawyer turned bank examiner turned whistleblower turned one-woman swat team, the 340-page tome takes the reader along on her gut-wrenching workdays for an entire seven months inside one of the most powerful and corrupted watchdogs of the powerful and corrupted players on Wall Street – the Federal Reserve Bank of New York.

The days were literally gut-wrenching. Segarra reports that after months of being alternately gas-lighted and bullied at the New York Fed to whip her into the ranks of the corrupted, she had to go to a gastroenterologist and learned her stomach lining was gone.

She soldiered through her painful stomach ailments and secretly tape-recorded 46 hours of conversations between New York Fed officials and Goldman Sachs. After being fired for refusing to soften her examination opinion on Goldman Sachs, Segarra released the tapes to ProPublica and the radio program This American Life and the story went viral from there...

In a nutshell, the whoring works like this. There are huge financial incentives to go along, get along, and keep your mouth shut about fraud. The financial incentives encompass both the salary, pension and benefits at the New York Fed as well as the high-paying job waiting for you at a Wall Street bank or Wall Street law firm if you show you are a team player .

If the Democratic leadership of the House Financial Services Committee is smart, it will reopen the Senate's aborted inquiry into the New York Fed's labyrinthine conflicts of interest in supervising Wall Street and make removing that supervisory role a core component of the Democrat's 2020 platform. Senator Bernie Sanders' platform can certainly be expected to continue the accurate battle cry that 'the business model of Wall Street is fraud.'"

Pam Martens, Wall Street on Parade

The New York Sun

By DAWN BENNETT,

Adapted From Financial Myth Busting | April 5, 2015http://www.nysun.com/national/the-floating-kilogram-the-editor-of-the-sun-talks/89117/

The following is adapted from an interview by Dawn Bennett, host of the radio show "Financial Myth Busting," with the editor of The New York Sun, Seth Lipsky. The broadcast aired March 8:

* * *

Ms. Bennett: Seth Lipsky is the author of a book titled "The Floating Kilogram and Other Editorials on Money from The New York Sun." Before the Sun, he spent 20 years at the Wall Street Journal where he served on the editorial board and helped launch the Asian Wall Street Journal as well as the Wall Street Journal Europe. Recently, Seth authored a column in the New York Post titled "Why does the Federal Reserve Fear a Real Audit," which is a question much on my mind. Seth, welcome.

Mr. Lipsky: Thanks, Dawn. It's nice to be with you.

Ms. Bennett: To put it charitably, Janet Yellen appears to be very alarmed that some members of Congress want to conduct a comprehensive audit of the Federal Reserve for the first time since it was created. If the Federal Reserve is doing everything correctly, why should Mrs. Yellen be alarmed and what does she have to hide?

Mr. Lipsky: Well, that's a great question. The Federal Reserve is already audited, in the sense that an accountant comes in and goes over its books. But what the Congress is talking about is a much broader look by the Governmental Accountability Office of how the central bank forms our monetary policy and what its relations are with foreign banks. The Fed has been fighting this tooth and nail as an intrusion on its independence. What Congress knows is that the Constitution gave the monetary power precisely to Congress.

Congress has a constitutional obligation and power to establish the American monetary system and regulate it, to coin money, regulate its value and that of foreign coinage. This has become a big issue where we have not taken a really systematic look at how the Fed operates in the hundred years that it's been in existence. We're starting the second century, and there is growing sentiment in the Congress to take a look at this. The audit of the Fed measure passed the House as recently as of September by a vote of 333 to 92, with 109 Democrats joining the Republicans. So the Fed is certainly growing concerned.

Ms. Bennett: The only reason Janet Yellen has the power to coin money is because Congress delegated its own power to the Federal Reserve in 1913. Isn't congressional oversight of that power something that should be considered commonsensical by the Federal Reserve?

Mr. Lipsky: The Fed was created in 1913. The Coinage power was first acted on in 1792, and coinage was given not to any Federal Reserve but to the United States Mint. When the second central bank came up to the Supreme Court it was really the tax and the borrowing power that the courts were looking at when they okayed the authority of the central bank.

Ms. Bennett: We are all accountable to someone or something, so what is wrong about the Federal Reserve being accountable to Congress?

Mr. Lipsky: Nothing whatsoever. Even Chairman Yellen acknowledges that Congress has the power. She's just pleading and warning that it not interfere. Why is Congress growing concerned about this in the first place? It's because the Great Recession has lasted six years and we still do not feel like we've recovered. What is the Fed's role in this? Could the reason that the Great Recession lasted so long be attributable to monetary policy? The value of the dollar has been allowed to collapse below one 1,100th of an ounce of gold. It was a 265th of an ounce of gold when George W. Bush was sworn in. These are huge questions, and somebody needs to ask them.

Ms. Bennett: It is quite clear to me that the Federal Reserve doesn't want the rest of us to actually be able to see what they really up to. If we did know what they're doing, do you think most Americans would just want it shut down? To your point, since 1913, the dollar has actually lost over 97% of its purchasing power. And of course, the economy has been subjected to one painful depression and a series of what I call Fed-created recessions. Despite the poor track record, we continue to support them. At the end of the day, does it matter if we even have a Federal Reserve?

Mr. Lipsky: I think the monetary questions do matter to every American in all positions. My favorite statistic is that between 1947 and 1971 the average unemployment rate was below 5%. From 1971 until today it was above 6%. What happened in 1971, when the unemployment rate began souring? What happened is we abandoned the Bretton Woods Gold Exchange System, under which the dollar was linked to gold, and the money began flowing not in the productive enterprises, but into the money markets and hedge funds and all these sorts of things and not so much into the kind of investment that created the great industrial base in America.

Ms. Bennett: Let's talk about that type of investment. According to a government report I've read, the Federal Reserve made $16.1 trillion in loans to big banks during that financial crisis. In my opinion, [it once] created the dotcom bubble and the housing bubble. Now, I think it has created the financial bubble that our markets are experiencing.

Mr. Lipsky: Asset inflation. The debate over inflation is one of the most important debates in the country. The left wing likes to say there is no inflation, but the dollar is worth only a tiny amount of the constitutional specie, which is gold and silver, compared to what it used to be worth. This is what people feel when they hear the government say there's no inflation but they try to go to the grocery store and they spend $50 or $100 on a tiny plastic bag with a few items in it.

Ms. Bennett: Yes, I know shelf inflation is huge, but I want to talk about commodities for a bit. The Department of Justice has recently said again that they're going after the big banks that have been, on an ongoing and continuous basis, manipulating gold and silver. What are your thoughts on that? Will it work this time? And, if so, is there a simple solution to stop them from doing this? They seem to get their hands slapped, apologize, and then come back and do it again, and again.

Mr. Lipsky: The news that the Justice Department is looking at something like ten or twelve major banks for possibly rigging the price of gold broke the same week that Mrs. Yellen was up on Capitol Hill testifying against an audit of the Fed.

Ms. Bennett: That's right.

Mr. Lipsky: One of the questions that The New York Sun raised is what is she afraid of then? Is it the danger that the Fed has been meddling in the gold market the way the Justice Department is alleging commercial banks have been doing it? It's the Fed that regulates commercial banks after all. I don't want to carry that argument too far. I asked it then in an editorial more in the nature of a question. But there is a movement in Congress to open up what is called a Centennial Monetary Commission that after the first hundred years of the Fed, would just take a look at how the whole system is working.

We've been in a period of fiat money, meaning dollars that have no connection in law to any gold or silver or other constitutional money. We've been in a fiat system since 1971. Previously, our dollars were always defined in terms of gold and silver, suddenly they're not. The unemployment average is much higher; the bankruptcy rate is much higher; the inequality rate has been much higher since the mid 1970's. Could this be related to the fact that we abandoned sound money in the mid 1970s?

Ms. Bennett: De-dollarization has been going on now for the last few years, and I think it's because the dollar is continuing to get weaker. Our political system and economic system aren't what they used to be. Do you think it's possible that if China, for example, standardizes the renminbi it will start taking power away from the U.S. dollar?

Mr. Lipsky: The abandonment of sound money by the U.S. has brought forth a whole chain of foreign governments that are alarmed and wonder whether a new system should be set up. China. There is talk of Russia going on a gold standard; the European Union is having its own catastrophe with the Euro, and it's wondering whether the dollar ought to be replaced as the international reserve. The United Nations, for crying out loud, has gotten involved in this.

One of my favorite moments happened in 1965, when the President of France, Charles de Gaulle, called a thousand reporters into the presidential palace sat them down and addressed them on the importance of restoring gold as the international standard. His argument was that it puts all countries on the same basis: America, France, England, China, little countries, and it takes a lot of the partisanship out of the monetary question internationally, or it takes the politics out of money. It's ironic that Fed loves to talk about how we shouldn't politicize the monetary system. If one really wants to de-politicize the monetary system, restoring a gold standard or something like it is exactly the way to do it.

Ms. Bennett: Mrs. Yellen claims that opening the Fed to an outside audit would "politicize" - her word - monetary policy.

Mr. Lipsky: Right.

Ms. Bennett: Isn't it political when Senator Schumer, for example, tells her to keep rates low every time she testifies before the Senate Banking Committee? Isn't it already happening?

Mr. Lipsky: You're exactly right. Why is it always the conservatives that are doing the politicizing and not the liberals? The big politicization of monetary policy happened in 1978 with the passage of Humphrey-Hawkins, which said that the Fed has to have a second mandate of increasing the employment rate or decreasing unemployment, in addition to affecting the value of our dollar. That opened the door to an enormous political interference in monetary policy.

Ms. Bennett: I know you're not a gold trader or silver trader...

Mr. Lipsky: I'm a newspaperman.

Ms. Bennett: There you go. But I'm certain you follow the markets. What do you think would be a simple solution to fix the ongoing and continuous manipulation of gold and silver so that we can get more stability? It does seem, whether it's a Federal Reserve or some other central bank, that they're interfering with it in order to make the fiat currency look stronger than it really is.

Mr. Lipsky: I favor a definition by law, enacted by Congress under its constitutional powers to coin money and regulate its value, and fix the standards of weights and measures - a law passed by Congress defining the dollar as a fixed amount of gold or silver. Silver was the main specie used in early years of our republic. The debate over whether gold or silver was better went on through the 19th century, and we basically decided in 1900, with the passage of the Gold Standard Act, to make gold the true national money. I think that would go a long way toward solving this problem. There are a lot of questions as to exactly how to do it, whether there should be a system like Bretton Woods, which said dollars had to be redeemed in gold if they were held by foreign governments.

Ms. Bennett: In physical gold, not paper gold. In physical gold.

Mr. Lipsky: Right.

Ms. Bennett: There's a big difference there.

Mr. Lipsky: Therefore the price at which one fixes the dollar, the value, the amount of gold, has to be carefully worked out. But the gold standard is not some flaky thing. This was believed in by George Washington, Thomas Jefferson, James Madison, Alexander Hamilton, and almost every president since, up until Richard Nixon. John Kennedy, Woodrow Wilson, Grover Cleveland - they all believed in it.

Ms. Bennett: Seth, "The Floating Kilogram and other Essays on Money from The New York Sun." For any listeners not familiar with the Sun, can you bring them up to speed?

Mr. Lipsky: The New York Sun is an online newspaper that I edit. We published in print until several years ago. It's a leading voice in journalism for a sound dollar. It supports a sound dollar, limited government, and a restoration of constitutional dollar based on gold or silver. This is the first radio interview about the book.

Ms. Bennett: Thank you.

Mr. Lipsky: This book contains on this issue 130 editorials that have been issued in the Sun in recent years. Steve Forbes calls them "brilliant," "irrefutable," and "the Federalist Papers for the gold standard." James Grant calls the book both "persuasive" and "unfailingly entertaining." It's a book for every person, not just the experts, and it's available on Amazon.com, the online bookstore, and you'll have a copy in a day or two if you place your order. "Pure gold" is the way the economist Judy Shelton described this book. The title, Dawn, comes from the discovery that the kilogram, which is the last metric weight measure based on a physical object, has been losing mass - atom by atom. The Sun in one of its editorials said, "Why don't we float the kilogram just like we float the dollar?" That's from where the title of the book comes.

Ms. Bennett: If President Obama, or our next president, were to become motivated to make reforms, what do you think the takeaway from this book would to be? Definitely a gold standard?

Mr. Lipsky: So I think the takeaway is going to be that in our monetary system at some point, the dollar has to be defined in terms of something real rather than just another dollar. At the moment, if you take your dollar to the central bank to redeem it, they'll give you another dollar. There's no reference to anything real and no classical measure of value. We have what Jim Grant likes to call the Ph.D. standard, and I think we need to move away from that to the kind of standard that sustained our country during its periods of greatest growth and strongest employment.

Ms. Bennett: We always seem to make changes in the United States when things break down, but not beforehand. What is going to be the instigator to standardize our currency?

Mr. Lipsky: People say things could become a disaster. The last six years have been a disaster.

Ms. Bennett: Exactly.

Mr. Lipsky: Huge amounts of unemployment, not just for a short period, but for six years. It's consumed almost the entire Obama presidency. People are still trying to figure out their homes, still trying to figure out how the price of college got more than halfway to $100,000 a year - you know, all these things. We've been living through this, and I think events have energized Congress to start looking at this. The Sound Dollar Act, or Centennial Monetary Commission Act, or Audit the Fed Act, or Free Competition in Currency Act. This is why Janet Yellen - to bring it back to where we came in - is fighting so hard against the Congress doing this. We're in a constitutional moment here where Congress is going to take a look at this, I predict.

Ms. Bennett: Do you think they're going to have the guts to do it?

Mr. Lipsky: I think the American people have a lot of guts.

Ms. Bennett: Me, too.

Mr. Lipsky: And at the end of the day, the Congress has to listen to the American people.

Zero Hedge

While the world of mainstream media stock pundits would like investors to believe that there is a wall of money on the sidelines waiting anxiously to go all-in on stocks (bear in mind there's a seller for every buyer and where does the cash on the sidelines go when it is handed over to the seller in return for his stock?), as none other than Charles Schwab notes in this brief Bloomberg TV clip, "investors are less rattled" than most believe, "and have stayed invested" in large part. "There hasn't been a wholesale movement away from stocks," he goes on, busting myths asunder, adding that "investors want to see market-driven conditions, not Fed manipulated ones."

So perhaps - just perhaps - Schwab is right, if the Fed stepped away and let markets be markets once again, maybe real capital would flow once again?

Schwab goes on to discuss how the Fed's policy has hurt the older generation - "it has been a terrible thing"

Beginning at around 50 seconds, Schwab calmly dismisses one of the biggest market myths and raises a few red flags - "we see the market go up or down depending on which Fed member is speaking..."

April 17, 2013

From the event at the Philadelphia Fed on April 17th, 2013 (04/17/2013) conference segment "Fixing the Banking System for Good" .

In video testimony to the Philadelphia Federal Reserve in April of 2013, Jeffrey Sachs, one of the world's most respected economists, expresses outrage at the extent of moral bankruptcy in the American financial system and the docile president and regulators who do nothing about it.

Jeffrey Sachs' Speech on Wall Street Corruption The Big Picture

April 30, 2013 at 9:21 am

Hmmm.

Corrupt government; corrupt financial system; corrupt business culture; corrupt legal system.

Why on earth is America inheriting the Russian model ?

Petey Wheatstraw

It's the standard for failed countries.

spooz

For those who would like to listen to other speakers at The 31st Annual Monetary and Trade Conference where Sachs presented this (including Michael Kumhof's presentation on The Chicago Plan Revisited, which starts at about 1:02, and which I would LOVE to see more economists discuss), here is the link.

Concerned Neighbour

Of course he's right. It's truly remarkable the amount of corruption out there that is visible; just imagine how much isn't.

My own pet theory is that the regulators made a deal early on in the crisis with the TBTF banks: "Help us levitate the markets, and we won't throw you in jail". If I'm right, it's obviously been a massive success.

Mark E HofferSachs, and others, may appreciate..

The Propaganda System That Has Helped Create a Permanent Overclass Is Over a Century in the Making

April 29, 2013

Print VersionBy Andrew Gavin Marshall, Blacklisted News

Where there is the possibility of democracy, there is the inevitability of elite insecurity. All through its history, democracy has been under a sustained attack by elite interests, political, economic, and cultural. There is a simple reason for this: democracy – as in true democracy – places power with people. In such circumstances, the few who hold power become threatened. With technological changes in modern history, with literacy and education, mass communication, organization and activism, elites have had to react to the changing nature of society – locally and globally.

From the late 19th century on, the "threats" to elite interests from the possibility of true democracy mobilized institutions, ideologies, and individuals in support of power. What began was a massive social engineering project with one objective: control. Through educational institutions, the social sciences, philanthropic foundations, public relations and advertising agencies, corporations, banks, and states, powerful interests sought to reform and protect their power from the potential of popular democracy…"

http://www.blacklistednews.com/The_Propaganda_System_That_Has_Helped_Create_a_Permanent_Overclass_Is_Over_a_Century_in_the_Making/25648/0/38/38/Y/M.html

Simon Johnson continues his push against conflicts of interest within the Federal Reserve system:Three More Governance Questions for the Fed, by Simon Johnson, Commentary, NY Times: Over the last several weeks on this blog, I have expressed ... concerns about governance arrangements at the Federal Reserve Bank of New York. I have made the specific case for Jamie Dimon, the chief executive of JPMorgan Chase, to step down from the New York Fed's board because of the large, unexpected losses in his bank's London proprietary trading operation - and the fact that these activities and their disclosure are now under investigation by the Fed. ...

In addition,... I have three substantive governance concerns for the New York Fed... First and most important, why didn't Mr. Dimon step down from the board of the New York Fed in March 2008, when JPMorgan Chase bought Bear Stearns with financial support provided, in part, by the Fed? ...

The authorities worked closely with JPMorgan Chase... JPMorgan's downside risk ... was limited. ... The precise terms of this arrangement were, appropriately, subject to detailed negotiation... How was it appropriate for Mr. Dimon to remain on the board of the New York Fed while this negotiation was going on? ...

Second, I would like to raise a question about Stephen Friedman, who was a Class C director of the New York Fed - and chairman during the intense financial crisis period, from January 2008 through early 2009. ...

According to the rules established by the Federal Reserve Board,... [there is a] fairly comprehensive ban on holding financial stock... But Mr. Friedman at that time was and still is a senior executive at Stone Point Capital, where ... he is involved in the fund's investment decisions. ... How was Mr. Friedman allowed to own these shares while being a Class C director? ...

Mr. Friedman bought Goldman Sachs stock after the company was effectively rescued by the Federal Reserve... I don't understand how a Class C director could have thought it was acceptable to buy any financial services company stock. ...

Third, I have a further question about the role of Lee C. Bollinger, the president of Columbia University, who is a Class C director and chairman of the Federal Reserve Bank of New York. ...

According to the Federal Reserve Act (Section 4.20): the chairman of a Federal Reserve Bank "shall be a person of tested banking experience." Mr. Bollinger ... does not have banking experience. ... Please explain to me how having Mr. Bollinger as chairman of the New York Fed is consistent with the Federal Reserve Act.

Taken together, these three questions raise a much bigger issue. If the intent and letter of the Federal Reserve Act are being followed in some ways and not in others - without proper notification to Congress or written rules available to the public explaining exemptions and exceptions - how exactly does this help maintain the legitimacy of the Federal Reserve System?

See also Corruption of FED

May 24, 2012By Simon Johnson

There are two diametrically opposed views of how the largest financial companies in our economy operate. On the one hand, there are those like Charles Ferguson, director of the Academy Award-winning documentary "Inside Job" and author of the new book, "Predator Nation." Mr. Ferguson takes the view that greed and immorality now prevail to an excessive degree at the heart of Wall Street.

Academics and other experts have become corrupted, the responsible regulators have been intellectually captured, and law enforcement officials refuse to act – despite the accumulation of evidence before their eyes.

"Inside Job" was gripping and emotional; "Predator Nation" contains many more specific details and evidence, as this excerpt dealing with academics (one Republican and one Democrat) makes clear.

The second view is that the people in charge of large banks and bank holding companies have done nothing wrong. To see this view in action, look no further than this week's debate about whether Jamie Dimon, chief executive of JPMorgan Chase, should resign from the board of the Federal Reserve Bank of New York. The New York Fed oversees his organization, including assessing whether it is taking dangerous risks, so there are reasonable questions about whether this creates a potential conflict of interest.

A balanced account of this debate appeared in American Banker, which kindly agreed to bring the entire article out from behind its paywall. The strongest statement from the pro-Dimon corner comes from Ernest Patrikis, a partner with White & Case L.L.P. and former general counsel of the New York Federal Reserve:

"I don't see Jamie Dimon's conflict of interest. What's the conflict? He's expected to represent the banks' view, the lenders' view."

Yet even people who are generally sympathetic to banks feel that there is a perception problem with Mr. Dimon's position. Treasury Secretary Timothy Geithner said exactly that to the "PBS NewsHour" last week.

Kenneth Guenther, the former head of the Independent Community Bankers of America, told American Banker:

"I do think there is a public perception problem when the head of the largest bank gets into a massive highly publicized trading loss, which he articulately condemns, when he's tied to the Federal Reserve Bank of New York, and the president of the Federal Reserve Bank is vice chair of the Federal Open Market Committee. There is a perception problem. I don't think there's any way around it."

What exactly is a conflict of interest? Narrowly defined, an actual conflict of interest would involve using public office for personal financial gain – and would be a matter for criminal prosecution.

There is only one case that I am aware of in which a director of the New York Fed went to prison for such a violation – Robert A. Rough was indicted in December 1988, on charges that he leaked sensitive interest-rate information to a brokerage firm. He was sentenced to six months in prison.

More broadly, however, in modern America we use the term "conflict of interest" when we believe someone may be promoting private interests while acting in a public role.

Allowing big bankers to become too influential is an important part of what Mr. Ferguson writes about. If you don't understand the channels through which influence actually works in the United States today, you need to see "Inside Job," which touched a nerve and won an Oscar precisely because it is profoundly undemocratic when powerful people are able behave in this way.

Elizabeth Warren, a Democratic candidate for the Senate in Massachusetts, said Mr. Dimon should resign from the board of the New York Fed. The recent spectacular trading losses at his company require a full investigation, which should include an examination of how the supervision process broke down. How can this be anything other than awkward for the New York Fed while Mr. Dimon – hardly known as a shrinking violet – sits on its board?

Senator Bernie Sanders, independent of Vermont, would go further, proposing legislation that would remove any bankers from the boards of Federal Reserve banks. For more background, you may want to consult Page 65 and other parts of this report from the Government Accountability Office, which deal with potential conflicts of interest in the Federal Reserve System, or at least read Senator Sanders's summary of the report.

To be clear, directors of the New York Fed are in principle kept away from bank-supervision matters – a point that was codified in December 2010, following the passage of the Dodd-Frank financial reform legislation.

Under the current bylaws, directors are not involved in appointing, monitoring or compensating the head of supervision, although they have input into the selection and remuneration of the head of research (an important position, as this person helps to shape the Fed's view on bank capital and all technical matters relative to risk management), and they oversee other management issues. Bill Dudley, the president of the New York Fed, interacts with the board at least several times a month, as you can see from his schedule.

Mr. Dudley, a former Goldman Sachs executive, was originally appointed president of the New York Fed by a board that included Mr. Dimon as a voting member. The Dodd-Frank legislation stripped so-called "Class A" directors, of which Mr. Dimon is one, from voting on such appointments. Mr. Dudley was subsequently reappointed by the Class B and Class C directors of the board. (For more on the different classes of directors, see this page)

Mr. Dimon has also been an outspoken opponent of financial reform of late – including the Volcker Rule (on proprietary trading) and attempts to strengthen capital requirements. He is an intensely political figure, despite the fact that an important footnote in the Board of Governors' policy on political activity by Reserve Bank Directors says,

In all instances, directors should avoid any political activity that would publicly identify the director as being associated with the Federal Reserve System or would embarrass the System or raise questions about the independence of the director or the ability to perform Federal Reserve duties.

Directors are allowed to lobby and engage in other specific activities. The issue is whether these actions undermine the effectiveness of the New York Fed.

There is recent precedent for New York Fed board members resigning when there is a perceived conflict of interest – and when the legitimacy of the Federal Reserve System would undoubtedly have been undermined if they had refused to resign.

Dick Fuld, the chief executive of Lehman Brothers, resigned (on Thursday, September 11, 2008) shortly before his firm collapsed (on September 15, but its last day of business was Friday, September 12) – and presumably because the New York Fed was at the center of intense discussions about who should suffer what kind of losses or get rescued. Did he resign of his own volition or was he encouraged to resign?

Stephen Friedman, then the former chief executive of Goldman Sachs, resigned in early 2009 when it became clear that he had bought Goldman stock after Goldman became a bank and therefore fell under the supervision of the New York Fed.

Mr. Friedman was chairman of the New York Fed at that time. (To be clear, Mr. Friedman was not involved in any of the decisions that saved Goldman in fall 2008, and I am not accusing him of using his public position for personal financial gain.)

For those of you keeping score at home, Mr. Fuld was a Class B director and Mr. Friedman was a Class C director.

If you think Mr. Dimon should resign from the New York Fed, you can express your opinion by signing this on-line petition, which I drafted. (For more background on why he should resign, see this blog post.)

If Mr. Dimon refuses to resign – as seems likely – he can removed by the Board of Governors of the Federal Reserve System (not by his fellow directors at the New York Fed). The petition is therefore addressed to the Board of Governors.

There is an undeniable perception problem. It is damaging the legitimacy of the Federal Reserve. As Treasury Secretary Geithner implied, this must be "addressed" – a great Washington euphemism – by Mr. Dimon leaving the board of the New York Fed.

An edited version of this blog post appeared this morning on the NYT.com's Economix; it is used here with permission. If you would like to reproduce the entire column, please contact the New York Times.

mattmossman

Not impressed by that American Banker article. If the Fed needs to get the view of the banks, is having them on the board of a regulatory agency the only way to do so? The reporter should have asked Ernest Patrikis that. If the Fed would benefit from getting perspective from outside Washington, is having Jamie Dimon on the board of the NY Fed the only way to get that? Should have asked Chip MacDonald that. If its perception and not reality, shouldn't Karen Shaw Petrou be asked why, after what's happened, she feels that way?Vern McKinleyWe all know what the common sense position is about having a bank president on the board of a banking regulator. There should be more burden of proof placed upon the people insisting that this is fine. Not enough to just cite a perception/reality gap.

This gets back to the creation of the Federal Reserve in 1913/1914. It was a creation of bankers for bankers. A much more substantial change would be to make the FRBNY subject to the Freedom of Information Act. The Board in Washington is, the FRBNY is not. Makes no sense.

11 May 2012

...And They Repeatedly Fail to Protect the Public From It. "How can we expect righteousness to prevail when there is hardly anyone willing to stand up for a righteous cause?Such a fine, sunny day, and I have to go..."

Sophie Scholl, last words

The spin machine is revving up, and the spokesmodels are gesticulating wildly, in an effort to direct and deflect this failure of governance at JPM.

See how manfully Jamie Dimon has come clean on this. And look how well the Fed's capital standards are protecting us from a failure at JPM because of this unfortunate but 'manageable' trading mistake.A craven Congress, dominated by a hard core of one-percenter bully boys, an Obama Administration intimately tied to Wall St. cronies, and the Federal Reserve, which is a private institution of financial establishment insiders making a weak attempt at self-regulation cloaked in secrecy, have failed the public once again.Jamie and the regulators could not possibly have known (CEO defense) what was going on in their firm because the world is now so complex. They will try and work harder so don't disturb them or bad things will happen to us and it will be your fault. But this will be a buying opportunity!

Simon Johnson points out what many may miss in all this. The side effects of the continuing campaign by the banks' lobbyists to weaken reform have given us a hint of the next financial crisis to come which will be caused by a collapse in the derivatives market. And who could have seen it coming.

And I would like to make the point, and nail it to the door of the spineless media, that JPM had to admit, while the position was still open, that their 'hedge' had blown up in their faces, and that it was no hedge at all, but a thinly disguised attempt to circumvent the curbs on proprietary trading. More simply, they were preparing to flout the law and were brazenly lying about it, and their use of leverage and very risky bets in search of enormous bonuses. And they are doing the same thing on a much larger scale in other markets.

And it is no coincidence that financial fraud prosecutions under the Obama Administration are at a twenty year low, and the media and even his political opposition say almost nothing about it.

"All governments suffer a recurring problem: Power attracts pathological personalities. It is not that power corrupts but that it is magnetic to the corruptible."The credibility trap has captured our leadership. They cannot change course without admitting their failures, and to admit their failures is to weaken or even lose their grip on power. And so it's steady as she goes, onto the rocks. Better a general than a personal failure, risking other people's lives to protect your gains, because there is opportunity in a crisis as long as you still have a seat in the game.Frank Herbert

The cheating, stealing, and lying will continue until the system finally collapses, or until the people finally wake up, take responsibility for their government, and demand meaningful reform.

JP Morgan Debacle Reveals Fatal Flaw In Federal Reserve Thinking

By Simon Johnson

May 11, 2012Experienced Wall Street executives and traders concede, in private, that Bank of America is not well run and that Citigroup has long been a recipe for disaster. But they always insist that attempts to re-regulate Wall Street are misguided because risk-management has become more sophisticated – everyone, in this view, has become more like Jamie Dimon, head of JP Morgan Chase, with his legendary attention to detail and concern about quantifying the downside.

In the light of JP Morgan's stunning losses on derivatives, announced yesterday but with the full scope of total potential losses still not yet clear (and not yet determined), Jamie Dimon and his company do not look like any kind of appealing role model. But the real losers in this turn of events are the Board of Governors of the Federal Reserve System and the New York Fed, whose approach to bank capital is now demonstrated to be deeply flawed.

JP Morgan claimed to have great risk management systems – and these are widely regarded as the best on Wall Street. But what does the "best on Wall Street" mean when bank executives and key employees have an incentive to make and misrepresent big bets – they are compensated based on return on equity, unadjusted for risk? Bank executives get the upside and the downside falls on everyone else – this is what it means to be "too big to fail" in modern America.The Federal Reserve knows this, of course – it is stuffed full of smart people. Its leadership, including Chairman Ben Bernanke, Dan Tarullo (lead governor for overseeing bank capital rules), and Bill Dudley (president of the New York Fed) are all well aware that bankers want to reduce equity levels and run a more highly leveraged business (i.e., more debt relative to equity). To prevent this from occurring in an egregious manner, the Fed now runs regular "stress tests" to assess how much banks could lose – and therefore how much of a buffer they need in the form of shareholder equity.

In the spring, JP Morgan passed the latest Fed stress tests with flying colors. The Fed agreed to let JP Morgan increase its dividend and buy back shares (both of which reduce the value of shareholder equity on the books of the bank). Jamie Dimon received an official seal of approval. (Amazingly, Mr. Dimon indicated in his conference call on Thursday that the buybacks will continue; surely the Fed will step in to prevent this until the relevant losses have been capped.)

There was no hint in the stress tests that JP Morgan could be facing these kinds of potential losses. We still do not know the exact source of this disaster, but it appears to involve credit derivatives – and some reports point directly to credit default swaps (i.e., a form of insurance policy sold against losses in various kinds of debt.) Presumably there are problems with illiquid securities for which prices have fallen due to recent pressures in some markets and the general "risk-off" attitude – meaning that many investors prefer to reduce leverage and avoid high-yield/high-risk assets.

But global stress levels are not particularly high at present – certainly not compared to what they will be if the euro situation continues to spiral out of control. We are not at the end of a big global credit boom – we are still trying to recover from the last calamity. For JP Morgan to have incurred such losses at such a relatively mild part of the credit cycle is simply stunning.

The lessons from JP Morgan's losses are simple. Such banks have become too large and complex for management to control what is going on. The breakdown in internal governance is profound. The breakdown in external corporate governance is also complete - in any other industry, when faced with large losses incurred in such a haphazard way and under his direct personal supervision, the CEO would resign. No doubt Jamie Dimon will remain in place.

And the regulators also have no idea about what is going on. Attempts to oversee these banks in a sophisticated and nuanced way are not working.

The SAFE Banking Act, re-introduced by Senator Sherrod Brown on Wednesday, exactly hits the nail on the head. The discussion he instigated at the Senate Banking Committee hearing on Wednesday can only be described as prescient. Thought leaders such as Sheila Bair, Richard Fisher, and Tom Hoenig have been right all along about "too big to fail" banks (see my piece from the NYT.com on Thursday on SAFE and the growing consensus behind it).

The Financial Services Roundtable, in contrast, is spouting nonsense – they can only feel deeply embarrassed today. Continued opposition to the Volcker Rule invites ridicule. It is immaterial whether or not this particular set of trades by JP Morgan is classified as "proprietary"; all megabanks should be presumed incapable of managing their risks appropriately.

Read the rest here.

Jesse's Café AméricainFuture generations will look back and ask themselves, 'How could they not see what was happening? Were they blind?'

The Fed is not the only problem here, but a key enabler. White collar crimes and fraud flourished amongst the robber barons even in the days of the gold standard. It just was not as convenient, as easy, to defraud the people en masse through the debasement of the currency.

The Fed has merely proven to be as vulnerable as the regulators and the Congress to the power of the monied interests. If the political campaign process had not been corrupted by money, if the fairness doctrine in the media and Glass-Steagall in banking had not been overturned by the mindless impulse to cast aside the best of the laws, many of the problems we have today would not be so great.

These fellows creates crises, and then 'save us' from them, while lining their own pockets and perpetuating the swindle for their less publicly visible puppet masters.

There is little doubt in my own mind that Greenspan knew exactly what he was doing, and made his fateful decision after a meeting with Robert Rubin in the 1990's shortly after his famous 'irrational exuberance' speech. What was said, what was promised or threatened, I cannot say. But the change in direction became clear. It became open season on the voices of reason and restraint in Washington.

What Clinton hatched, Bush brought to full fruition, particularly with his tax cuts, stock bubble, and unfunded wars. And when the Great Reformer came to Washington in the midst of the collapse, he brought back the very advisors who had helped to create the problem in the first place and betrayed the mandate of those who had elected him, prosecuting no one.

And in the aftermath of the financial collapse, the first popular reform movement that rose up in anger against the bailouts, The Tea Party, was quickly turned into a corps of willing tools that turned on the weak and the least among us, the very victims of a corrupt system, in their petulant pride and misdirected anger.

I only fear that the Fed, and some of the perpetual outsiders of history, will be made the scapegoats by the real culprits when the time of reckoning comes, and that genuine reform will be thwarted once again as it has been so many times in the past. Their hypocrisy and shamelessness knows no bounds.

NYT

Who Captured the Fed?

By DARON ACEMOGLU and SIMON JOHNSON

March 29, 2012, 5:00 am...But in the light of the crisis of 2008 and its aftermath, we have to ask: Has our central bank fallen back under the influence of special interests?

...At the dawn of the republic, Thomas Jefferson railed against the risks posed by government backing for concentrated power in the financial sector. President Andrew Jackson fought to abolish the Second Bank of the United States in the 1830s, the leading private bank of his day, which helped manage public finances and the banking system. Consequently, there was nothing resembling a central bank in the United States for much of the 19th century.

The Federal Reserve System, created in 1913, was a uniquely American compromise, trying to balance public and private interests. Banks controlled the boards of the 12 regional Feds – with big Wall Street firms holding great sway over the New York Fed, which had a disproportionate influence within the system as a whole - and still does.

This version of the system presided over a crazed and highly leveraged stock market boom in the 1920s and the catastrophic collapse of credit in the early 1930s, while protecting the big Wall Street firms.

...Unfortunately, as the United States and other countries learned after 1945, clever politicians can use central banks to manipulate the business cycle, boosting output growth and cutting unemployment ahead of elections. Richard Nixon, for example, famously pushed the Fed to ease monetary policy when it suited him.

...Increasingly, however, it seems that technocratic policy-making is just a myth. We have come full circle, and the Wall Street banks are calling the shots again.

Crucially, the idea that politics is just about electioneering misses the point. Politics is about getting what you want, not just through the ballot box but by persuading people in public office to take actions that help you. So declaring the central bank independent doesn't move it outside the orbit of politics.

Monetary policy has an impact on inflation, output and employment. But it also has a major impact on stock market prices. Any central banker raising interest rates is reducing stock market values and thus eroding the bonuses of top bankers and other chief executives.

Those people will lobby, asserting that higher interest rates will undermine the economy and cause us to plummet into recession, or worse.

In principle, the Fed could stand up to the bankers, pushing back against all specious arguments. In practice, unfortunately, the New York Fed and the Board of Governors are quite deferential to financial-sector "experts." Bankers are persuasive; many are smart people, armed with fancy models, and they offer very nice income-earning opportunities to former central bankers.

We have lost track of the number of research notes from major banks pleading for easier credit, lower capital requirements, delay in implementing financial reforms or all of the above.

In recent decades the Fed has given way completely, at the highest level and with disastrous consequences, when the bankers bring their influence to bear – for example, over deregulating finance, keeping interest rates low in the middle of a boom after 2003, providing unconditional bailouts in 2007-8 and subsequently resisting attempts to raise capital requirements by enough to make a difference.

As the American economy begins to improve, influential people in the financial sector will continue to talk about the need for a prolonged period of low interest rates. The Fed will listen.

This time will not be different."

Read the entire article here.

A new audit of the Federal Reserve released Wednesday detailed widespread conflicts of interest involving directors of its regional banks. "The most powerful entity in the United States is riddled with conflicts of interest," Sen. Bernie Sanders said after reviewing the Government Accountability Office report.

The study required by a Sanders Amendment to last year's Wall Street reform law examined Fed practices never before subjected to such independent, expert scrutiny. "This is exactly the kind of outrageous behavior by the big banks and Wall Street that is infuriating so many Americans," Sanders said.

Sanders said he will work with leading economists to develop legislation to restructure the Fed and bar the banking industry from picking Fed directors.

The corporate affiliations of Fed directors from such banking and industry giants as General Electric, JP Morgan Chase, and Lehman Brothers pose "reputational risks" to the Federal Reserve System, the report said. Giving the banking industry the power to both elect and serve as Fed directors creates "an appearance of a conflict of interest," the report added.

The 108-page report found that at least 18 specific current and former Fed board members were affiliated with banks and companies that received emergency loans from the Federal Reserve during the financial crisis.

1 currency now -yogi :

"Here is what the GAO found:

- The affiliations of the Federal Reserve's board of directors with financial firms continue to pose "reputational risks" to the Federal Reserve System. (See page 32 of GAO report)

- The policy of the Federal Reserve to give members of the banking industry the power to both elect and serve on the Federal Reserve's board of directors creates "an appearance of a conflict of interest." (See page 32 of GAO report)

- The GAO identified 18 former and current members of the Federal Reserve's board affiliated with banks and companies that received emergency loans from the Federal Reserve during the financial crisis including General Electric, JP Morgan Chase, and Lehman Brothers. (See page 39 of GAO report)

- There are no restrictions on directors of the Federal Reserve Board from communicating concerns about their respective banks to the staff of the Federal Reserve. (See page 36 of GAO report)

- Many of the Federal Reserve's board of directors own stock or work directly for banks that are supervised and regulated by the Federal Reserve. These board members oversee the Federal Reserve's operations including salary and personnel decisions. (See page 41 of GAO report)

- Under current regulations, Fed directors who are employed by the banking industry or own stock in financial institutions can participate in decisions involving how much interest to charge to financial institutions receiving Fed loans; and the approval or disapproval of Federal Reserve credit to healthy banks and banks in "hazardous" condition. (See pages 41- 42 of GAO report)

- The Federal Reserve does not publicly disclose its conflict of interest regulations or when it grants waivers to its conflict of interest regulations. (See page 47 and 49 of GAO report)

- 21 members of the Federal Reserve's board of directors were involved in making personnel decisions in the division of supervision and regulation at the Fed. (See page 105 of GAO report)"

January 2, 2011 | nakedcapitalism.com

This post first appeared on August 24, 2008

Go Willem Buiter! The London School of Economics prof and former Bank of England and European Bank for Reconstruction and Development official has been saying for some time that the Fed suffers from "cognitive regulatory capture" and has been far too responsive to the needs of Wall Street. It's been puzzling to watch his detailed, well argued criticisms go unnoticed, particularly when they have been offered at forums where one would think they'd be impossible to ignore (for instance, a conference co-hosted by the New York Fed where Buiter presented a pretty harsh paper on what he called the North Atlantic Financial Crisis).

Well, he finally seems to have gotten through, perhaps because he is forward enough to criticize Fed officials to their face at an event they are hosting. Or maybe it's because the pattern of conduct he decries is so patently obvious that the key actors can no longer fool themselves. From Bloomberg:

Former Bank of England policy maker Willem Buiter sparked the biggest debate at the Federal Reserve's annual mountainside symposium, saying the central bank pays too much heed to the concerns of financial institutions."The Fed listens to Wall Street and believes what it hears," Buiter said yesterday in a paper presented to the Fed's conference in Jackson Hole, Wyoming. "This distortion into a partial and often highly distorted perception of reality is unhealthy and dangerous."

The Wall Street Journal's Economics blog provides a similar account and a link to the paper.

Mr. Buiter slams the Federal Reserve, European Central Bank and Bank of England for what he says was a mishandling of the financial crisis and monetary policy over the past year. He gives the worst marks to the Fed, saying it's too close to Wall Street and financial markets - responding to their needs to the detriment of the wider economy. Mr. Buiter, a former member of the BOE's Monetary Policy Committee, said the Fed overreacted to the economic slowdown - misjudging the importance of financial stability to the overall economy - and created a deeper inflation problem as a result.The paper is quite long, but it is very well written and moves very quickly for this sort of exercise (it does get geeky from time to time). I will confess to having read only the first 30 pages, but his argument seems spot on:

My thesis is that both monetary theory and the practice of central banking have failed to keep up with key developments in the financial systems of advanced market economies, and that as a result of this, many central banks were to varying degrees ill-prepared for the financial crisis that erupted on August 9, 2007.The Fed gets disproportionate attention, in part due to the venue of the presentation, in part because Buiter contends that the Fed did the worst job of the major central banks. Note that Buiter is more of inflation hawk than we are, but as a result, Buiter thinks that letting housing prices decline is not the end of the world and implicitly, adjustments need to run their course (per his point 4). Even though we think this deleveraging will be nastier than Buiter anticipates, we think that trying to hold asset prices at inflated levels will inevitably fail and the effort will only create more damage. To Buiter again:

[T]hree factors contribute to Fed's underachievement as regards macroeconomic stability. The first is institutional: the Fed is the least independent of the three central banks and, unlike the ECB and the BoE, has a regulatory and supervisory role; fear of political encroachment on what limited independence it has and cognitive regulatory capture by the financial sector make the Fed prone to over-react to signs of weakness in the real economy and to financial sector concerns.The second is a sextet of technical and analytical errors: (1) misapplication of the 'Precautionary Principle'; (2) overestimation of the effect of house prices on economic activity; (3) mistaken focus on 'core' inflation; (4) failure to appreciate the magnitude of the macroeconomic and financial correction/adjustment required to achieve a sustainable external equilibrium and adequate national saving rate in the US following past excesses; (5) overestimation of the likely impact on the real economy of deleveraging in the financial sector; and (6) too little attention paid (especially during the asset market and credit boom

that preceded the current crisis) to the behaviour of broad monetary and credit aggregates.All three central banks have been too eager to blame repeated and persistent upwards inflation surprises on 'external factors beyond their control', specifically food, fuel and other commodity prices. The third cause of the Fed's macroeconomic underachievement has been its tendency to use the main macroeconomic stability instrument, the Federal Funds target rate, to address financial stability problems. This was an error both because the official policy rate is a rather ineffective tool for addressing liquidity and insolvency issues and because more effective tools were available, or ought to have been. The ECB, and to some extent the BoE, have assigned the official policy rate to their price stability objective and have addressed the financial crisis with the liquidity management tools available to the lender of last resort and market maker of last resort.

Of his three charges, Buiter is on solid ground on the first and third. The second set (his points 1-6) are debatable, but you can make a case for them, and he does.

Some of his comments are blunt:

In the case of the Fed, the nature of the arrangements for pricing illiquid collateral offered by primary dealers invites abuse….All three central banks have gone well beyond the provision of emergency liquidity to solvent but temporarily illiquid banks. All three have allowed themselves to be used as quasifiscal agents of the state, providing subsidies to banks and other highly leveraged institutions, and assisting in their recapitalisation, while keeping the resulting contingent exposure off the budget and balance sheet of the fiscal authorities. Such subservience to the fiscal authorities undermines the independence of the central banks even in the area of monetary policy.

There is a lot of good stuff. For instance, Buiter discusses the "asymmetric" response of regulators to asset bubbles (they let the bubble run but jump in to try to arrest the collapse) and discusses remedies.

Unfortunately, a lot of participants seemed more interested in defending the Fed than in sifting through Buiter's analysis to see what might be valid and useful:

Fed Governor Frederic Mishkin said Buiter's paper fired "a lot of unguided missiles," and former Vice Chairman Alan Blinder "respectfully disagreed" with his analysis of the central bank's crisis management…..Mishkin lashed out against Buiter's assertion that the Fed's rate reductions may cause higher consumer prices.

"I wish he had actually read some of the literature on optimal monetary policy, because it might have been very helpful in this context," said Mishkin, who collaborated with Bernanke on inflation research in the 1990s.

Mishkin, a leading advocate of the Fed's effort to sustain economic growth through rapid rate reductions, said research shows that "what you need to do is act more aggressively."

In reply, Buiter said the value of such a strategy "is not at all obvious to me."

[Bank of Isreal's Stanley] Fischer, drawing laughter from the audience, held up a red fire extinguisher saying, "I asked the organizers for some technical assistance in dealing with this discussion."

While defending the Fed, Blinder said Buiter's papers "often feature an alluring mix of brilliant insight and outrageous statements." The central bank's performance, though not flawless, has been "pretty good" given the magnitude of the crisis, he said.

European Central Bank President Jean-Claude Trichet also came to the Fed's defense, saying "what has been done until now has been pretty well done under very difficult circumstances."

Although the Wall Street Journal coverage of the response is less detailed, it says that Blinder, who was tasked with critiquing the paper, told a long-form version of the Dutch boy putting his finger in the dam, and said that Buiter would rather have the dam leak out of obedience to his belief in moral hazard, and let the dam burst.

I may be reading too much into this, but it strikes me that Blinder went out of his way to be insulting (anyone who regularly participates in critiques of academic papers please read the WSJ post and comment).