The French economist Thomas Piketty argued last year in a surprising best-seller, "Capital in

the Twenty-First Century," that rising wealth inequality was a natural result of free-market policies,

a direct challenge to the conventional view that economic inequalities shrink over time. The controversial

implication drawn by Mr. Piketty is that governments should raise taxes on the wealthy.

Notable quotes:

"... His speeches can blend biblical fury with apocalyptic doom. Pope Francis does not just criticize the excesses of global capitalism. He compares them to the "dung of the devil." He does not simply argue that systemic "greed for money" is a bad thing. He calls it a "subtle dictatorship" that "condemns and enslaves men and women." ..."

"... The Argentine pope seemed to be asking for a social revolution. "This is not theology as usual; this is him shouting from the mountaintop," said Stephen F. Schneck, the director of the Institute for Policy Research and Catholic studies at Catholic University of America in Washington. ..."

"... Left-wing populism is surging in countries immersed in economic turmoil, such as Spain, and, most notably, Greece . But even in the United States, where the economy has rebounded, widespread concern about inequality and corporate power are propelling the rise of liberals like Senator Bernie Sanders of Vermont and Senator Elizabeth Warren of Massachusetts, who, in turn, have pushed the Democratic Party presidential front-runner, Hillary Rodham Clinton, to the left. ..."

"... Even some free-market champions are now reassessing the shortcomings of unfettered capitalism. George Soros, who made billions in the markets, and then spent a good part of it promoting the spread of free markets in Eastern Europe, now argues that the pendulum has swung too far the other way. ..."

"... Many Catholic scholars would argue that Francis is merely continuing a line of Catholic social teaching that has existed for more than a century and was embraced even by his two conservative predecessors, John Paul II and Benedict XVI. Pope Leo XIII first called for economic justice on behalf of workers in 1891, with his encyclical "Rerum Novarum" - or, "On Condition of Labor." ..."

"... Francis has such a strong sense of urgency "because he has been on the front lines with real people, not just numbers and abstract ideas," Mr. Schneck said. "That real-life experience of working with the most marginalized in Argentina has been the source of his inspiration as pontiff." ..."

"... In Bolivia, Francis praised cooperatives and other localized organizations that he said provide productive economies for the poor. "How different this is than the situation that results when those left behind by the formal market are exploited like slaves!" he said on Wednesday night. ..."

"... It is this Old Testament-like rhetoric that some finding jarring, perhaps especially so in the United States, where Francis will visit in September. His environmental encyclical, "Laudato Si'," released last month, drew loud criticism from some American conservatives and from others who found his language deeply pessimistic. His right-leaning critics also argued that he was overreaching and straying dangerously beyond religion - while condemning capitalism with too broad a brush. ..."

"... The French economist Thomas Piketty argued last year in a surprising best-seller, "Capital in the Twenty-First Century," that rising wealth inequality was a natural result of free-market policies, a direct challenge to the conventional view that economic inequalities shrink over time. The controversial implication drawn by Mr. Piketty is that governments should raise taxes on the wealthy. ..."

"... "Working for a just distribution of the fruits of the earth and human labor is not mere philanthropy," he said on Wednesday. "It is a moral obligation. For Christians, the responsibility is even greater: It is a commandment." ..."

"... "I'm a believer in capitalism but it comes in as many flavors as pie, and we have a choice about the kind of capitalist system that we have," said Mr. Hanauer, now an outspoken proponent of redistributive government ..."

"... "What can be done by those students, those young people, those activists, those missionaries who come to my neighborhood with the hearts full of hopes and dreams but without any real solution for my problems?" he asked. "A lot! They can do a lot. ..."

ASUNCI�N, Paraguay - His speeches can blend biblical fury with apocalyptic doom. Pope Francis

does not just criticize the excesses of global capitalism. He compares them to the "dung of the devil."

He does not simply argue that systemic "greed for money" is a bad thing. He calls it a "subtle dictatorship"

that "condemns and enslaves men and women."

Having returned to his native Latin America, Francis has renewed his left-leaning critiques on

the inequalities of capitalism, describing it as an underlying cause of global injustice, and a prime

cause of climate change. Francis escalated that line last week when he made a

historic apology for the crimes of the Roman Catholic Church during the period of Spanish colonialism

- even as he called for a global movement against a "new colonialism" rooted in an inequitable economic

order.

The Argentine pope seemed to be asking for a social revolution. "This is not theology as usual; this is him shouting from the mountaintop," said Stephen F. Schneck,

the director of the Institute for Policy Research and Catholic studies at Catholic University of

America in Washington.

The last pope who so boldly placed himself at the center of the global moment was John Paul II,

who during the 1980s pushed the church to confront what many saw as the challenge of that era, communism.

John Paul II's anti-Communist messaging dovetailed with the agenda of political conservatives eager

for a tougher line against the Soviets and, in turn, aligned part of the church hierarchy with the

political right.

Francis has defined the economic challenge of this era as the failure of global capitalism to

create fairness, equity and dignified livelihoods for the poor - a social and religious agenda that

coincides with a resurgence of the leftist thinking marginalized in the days of John Paul II. Francis'

increasingly sharp critique comes as much of humanity has never been so wealthy or well fed - yet

rising inequality and repeated financial crises have unsettled voters, policy makers and economists.

Left-wing populism is surging in countries immersed in economic turmoil, such as Spain, and,

most notably, Greece. But even in the United States, where the economy has rebounded, widespread

concern about inequality and corporate power are propelling the

rise of liberals like Senator Bernie Sanders of Vermont and Senator Elizabeth Warren of Massachusetts,

who, in turn, have pushed the Democratic Party presidential front-runner, Hillary Rodham Clinton,

to the left.

Even some free-market champions are now reassessing the shortcomings of unfettered capitalism.

George Soros, who made billions in the markets, and then spent a good part of it promoting the spread

of free markets in Eastern Europe, now argues that the pendulum has swung too far the other way.

"I think the pope is singing to the music that's already in the air," said Robert A. Johnson,

executive director of the Institute for New Economic Thinking, which was financed with $50 million

from Mr. Soros. "And that's a good thing. That's what artists do, and I think the pope is sensitive

to the lack of legitimacy of the system."

Many Catholic scholars would argue that Francis is merely continuing a line of Catholic social

teaching that has existed for more than a century and was embraced even by his two conservative predecessors,

John Paul II and Benedict XVI. Pope Leo XIII first called for economic justice on behalf of workers

in 1891, with his encyclical "Rerum Novarum" - or, "On Condition of Labor."

Mr. Schneck, of Catholic University, said it was as if Francis were saying, "We've been talking

about these things for more than one hundred years, and nobody is listening."

Francis has such a strong sense of urgency "because he has been on the front lines with real people,

not just numbers and abstract ideas," Mr. Schneck said. "That real-life experience of working with

the most marginalized in Argentina has been the source of his inspiration as pontiff."

Francis made his speech on Wednesday night, in Santa Cruz, Bolivia, before nearly 2,000 social

advocates, farmers, trash workers and neighborhood activists. Even as he meets regularly with heads

of state, Francis has often said that change must come from the grass roots, whether from poor people

or the community organizers who work with them. To Francis, the poor have earned knowledge that is

useful and redeeming, even as a "throwaway culture" tosses them aside. He sees them as being at the

front edge of economic and environmental crises around the world.

In Bolivia, Francis praised cooperatives and other localized organizations that he said provide

productive economies for the poor. "How different this is than the situation that results when those

left behind by the formal market are exploited like slaves!" he said on Wednesday night.

It is this Old Testament-like rhetoric that some finding jarring, perhaps especially so in the

United States, where Francis will visit in September. His environmental encyclical, "Laudato Si',"

released last month, drew loud criticism from some American conservatives and from others who found

his language deeply pessimistic. His right-leaning critics also argued that he was overreaching and

straying dangerously beyond religion - while condemning capitalism with too broad a brush.

"I wish Francis would focus on positives, on how a free-market economy guided by an ethical framework,

and the rule of law, can be a part of the solution for the poor - rather than just jumping from the

reality of people's misery to the analysis that a market economy is the problem," said the Rev. Robert

A. Sirico, president of the Acton Institute for the Study of Religion and Liberty, which advocates

free-market economics.

Francis' sharpest critics have accused him of being a Marxist or a Latin American Communist, even

as he opposed communism during his time in Argentina. His tour last week of Latin America began in

Ecuador and Bolivia, two countries with far-left governments. President Evo Morales of Bolivia, who

wore a Che Guevara patch on his jacket during Francis' speech, claimed the pope as a kindred spirit

- even as Francis seemed startled and caught off guard when Mr. Morales gave him a wooden crucifix

shaped like a hammer and sickle as a gift.

Francis' primary agenda last week was to begin renewing Catholicism in Latin America and reposition

it as the church of the poor. His apology for the church's complicity in the colonialist era received

an immediate roar from the crowd. In various parts of Latin America, the association between the

church and economic power elites remains intact. In Chile, a socially conservative country, some

members of the country's corporate elite are also members of Opus Dei, the traditionalist Catholic

organization founded in Spain in 1928.

Inevitably, Francis' critique can be read as a broadside against Pax Americana, the period of

capitalism regulated by global institutions created largely by the United States. But even pillars

of that system are shifting. The World Bank, which long promoted economic growth as an end in itself,

is now increasingly focused on the distribution of gains, after the Arab Spring revolts in some countries

that the bank had held up as models. The latest generation of international trade agreements includes

efforts to increase protections for workers and the environment.

The French economist Thomas Piketty argued last year in a surprising best-seller, "Capital

in the Twenty-First Century," that rising wealth inequality was a natural result of free-market policies,

a direct challenge to the conventional view that economic inequalities shrink over time. The controversial

implication drawn by Mr. Piketty is that governments should raise taxes on the wealthy.

Mr. Piketty roiled the debate among mainstream economists, yet Francis' critique is more unnerving

to some because he is not reframing inequality and poverty around a new economic theory but instead

defining it in moral terms. "Working for a just distribution of the fruits of the earth and human

labor is not mere philanthropy," he said on Wednesday. "It is a moral obligation. For Christians,

the responsibility is even greater: It is a commandment."

Nick Hanauer, a Seattle venture capitalist, said that he saw Francis as making a nuanced point

about capitalism, embodied by his coinage of a "social mortgage" on accumulated wealth - a debt to

the society that made its accumulation possible. Mr. Hanauer said that economic elites should embrace

the need for reforms both for moral and pragmatic reasons. "I'm a believer in capitalism but

it comes in as many flavors as pie, and we have a choice about the kind of capitalist system that

we have," said Mr. Hanauer, now an outspoken proponent of redistributive government policies

like a higher minimum wage.

Yet what remains unclear is whether Francis has a clear vision for a systemic alternative to the

status quo that he and others criticize. "All these critiques point toward the incoherence of the

simple idea of free market economics, but they don't prescribe a remedy," said Mr. Johnson, of the

Institute for New Economic Thinking.

Francis acknowledged as much, conceding on Wednesday that he had no new "recipe" to quickly change

the world. Instead, he spoke about a "process of change" undertaken at the grass-roots level.

"What can be done by those students, those young people, those activists, those missionaries

who come to my neighborhood with the hearts full of hopes and dreams but without any real solution

for my problems?" he asked. "A lot! They can do a lot. "You, the lowly, the exploited, the poor

and underprivileged, can do, and are doing, a lot. I would even say that the future of humanity is

in great measure in your own hands."

"... Oligarchs compete and alternate with one another over controlling and defining who votes and doesn't vote. They decide who secures plutocratic financing and mass media propaganda within a tiny corporate sector. 'Voter choice' refers to deciding which preselected candidates are acceptable for carrying out an agenda of imperial conquests, deepening class inequalities and securing legal impunity for the oligarchs, their political representatives and state, police and military officials. ..."

"... The politicians who participate in the restrictive and minoritarian electoral system, with its predetermined oligarchic results, celebrate 'elections' as a democratic process because a plurality of voters, as subordinate subjects, are incorporated. ..."

"... The striking differences in the rate of abstention in France, Puerto Rico and the UK reflect the levels of class dissatisfaction and rejection of electoral politics. ..."

"... Corbyn's foreign policy promised to end the UK's involvement in imperial wars and to withdraw troops from the Middle East. He also re-confirmed his long opposition to Israel's colonial land-grabbing and oppression of the Palestinian people, as a principled way to reduce terrorist attacks at home. ..."

"... In other words, Corbyn recognized that introducing real class-based politics would increase voter participation. This was especially true among young voters in the 18-25 year age group, who were among the UK citizens most harmed by the loss of stable factory jobs, the doubling of university fees and the cuts in national health services. ..."

"... In contrast, the French legislative elections saw the highest rate of voter abstention since the founding of the 5 th Republic. These high rates reflect broad popular opposition to ultra-neo-liberal President Francois Macron and the absence of real opposition parties engaged in class struggle. ..."

"... The established parties and the media work in tandem to confine elections to a choreographed contest among competing elites divorced from direct participation by the working classes. This effectively excludes the citizens who have been most harmed by the ruling class' austerity programs implemented by successive rightist and Social Democratic parties ..."

"... The vast majority of citizens in the wage and salaried class do not trust the political elites. They see electoral campaigns as empty exercises, financed by and for plutocrats. ..."

"... Most citizens recognize (and despise) the mass media as elite propaganda megaphones fabricating 'popular' images to promote anti-working class politicians, while demonizing political activists engaged in class-based struggles. ..."

"... Modern "Democracy" is a system for privatizing power and socializing responsibility. The elites get the power, the masses have to take responsibility for the consequences. because, of course, it's a 'democracy.' ..."

The most striking feature of recent elections is not ' who won or who lost' , nor is it

the personalities, parties and programs. The dominant characteristic of the elections is the widespread

repudiation of the electoral system, political campaigns, parties and candidates.

Across the world, majorities and pluralities of citizens of voting age refuse to even register

to vote (unless obligated by law), refuse to turn out to vote (voter abstention), or vote against

all the candidates (boycott by empty ballot and ballot spoilage).

If we add the many citizen activists who are too young to vote, citizens denied voting rights

because of past criminal (often minor) convictions, impoverished citizens and minorities denied voting

rights through manipulation and gerrymandering, we find that the actual 'voting public' shrivel to

a small minority.

As a result, present day elections have been reduced to a theatrical competition among the elite

for the votes of a minority. This situation describes an oligarchy � not a healthy democracy.

Oligarchic Competition

Oligarchs compete and alternate with one another over controlling and defining who votes and

doesn't vote. They decide who secures plutocratic financing and mass media propaganda within a tiny

corporate sector. 'Voter choice' refers to deciding which preselected candidates are acceptable for

carrying out an agenda of imperial conquests, deepening class inequalities and securing legal impunity

for the oligarchs, their political representatives and state, police and military officials.

Oligarchic politicians depend on the systematic plundering Treasury to facilitate and protect

billion dollar/billion euro stock market swindles and the illegal accumulation of trillions of dollars

and Euros via tax evasion (capital flight) and money laundering.

The results of elections and the faces of the candidates may change but the fundamental economic

and military apparatus remains the same to serve an ever tightening oligarchic rule.

The elite regimes change, but the permanence of state apparatus designed to serve the elite becomes

ever more obvious to the citizens.

Why the Oligarchy Celebrates " Democracy "

The politicians who participate in the restrictive and minoritarian electoral system, with

its predetermined oligarchic results, celebrate 'elections' as a democratic process because a plurality

of voters, as subordinate subjects, are incorporated.

Academics, journalists and experts argue that a system in which elite competition defines citizen

choice has become the only way to protect 'democracy' from the irrational 'populist' rhetoric appealing

to a mass of citizens vulnerable to authoritarianism (the so-called ' deplorables' ). The

low voter turn-out in recent elections reduces the threat posed by such undesirable voters.

A serious objective analysis of present-day electoral politics demonstrates that when the masses

do vote for their class interests � the results deepen and extend social democracy. When most voters,

non-voters and excluded citizens choose to abstain or boycott elections they have sound reasons for

repudiating plutocratic-controlled oligarchic choices.

We will proceed to examine the recent June 2017 voter turnout in the elections in France, the

United Kingdom and Puerto Rico. We will then look at the intrinsic irrationality of citizens voting

for elite politicos as opposed to the solid good sense of the popular classes rejection of elite

elections and their turn to extra-parliamentary action.

Puerto Rico's Referendum

The major TV networks (NBC, ABC and CBS) and the prestigious print media ( New York Times,

Washington Post, Financial Times and Washington Post ) hailed the ' overwhelming victory'

of the recent pro-annexationist vote in Puerto Rico. They cited the 98% vote in favor of becoming

a US state!

The media ignored the fact that a mere 28% of Puerto Ricans participated in the elections to vote

for a total US takeover. Over 77% of the eligible voters abstained or boycotted the referendum.

In other words, over three quarters of the Puerto Rican people rejected the sham ' political

elite election '. Instead, the majority voted with their feet in the streets through direct action.

France's Micro-Bonaparte

In the same way, the mass media celebrated what they dubbed a ' tidal wave ' of electoral

support for French President Emmanuel Macron and his new party, 'the Republic in March'. Despite

the enormous media propaganda push for Macron, a clear majority of the electorate (58%) abstained

or spoiled their ballots, therefore rejecting all parties and candidates, and the entire French electoral

system. This hardly constitutes a 'tidal wave' of citizen support in a democracy.

During the first round of the parliamentary election, President Macron's candidates received 27%

of the vote, barely exceeding the combined vote of the left socialist and nationalist populist parties,

which had secured 25% of the vote. In the second round, Macron's party received less then 20% of

the eligible vote.

In other words, the anti-Macron rejectionists represented over three quarters of the French electorate.

After these elections a significant proportion of the French people � especially among the working

class �will likely choose extra-parliamentary direct action, as the most democratic expression of

representative politics.

The United Kingdom: Class Struggle and the Election Results

The June 2017 parliamentary elections in the UK resulted in a minority Conservative regime forced

to form an alliance with the fringe Democratic Unionist Party (DUP), a far-right para-military Protestant

party from Northern Ireland. The Conservatives received 48% of registered voters to 40% who voted

for the Labor Party. However, 15 million citizens, or one-third of the total electorate abstained

or spoiled their ballots. The Conservative regime's plurality represented 32% of the electorate.

Despite a virulent anti-Labor campaign in the oligarch-controlled mass media, the combined Labor

vote and abstaining citizens clearly formed a majority of the population, which will be excluded

from any role the post-election oligarchic regime despite the increase in the turnout (in comparison

to previous elections).

Elections: Oligarchs in Office, Workers in the Street

The striking differences in the rate of abstention in France, Puerto Rico and the UK reflect

the levels of class dissatisfaction and rejection of electoral politics.

The UK elections provided the electorate with something resembling a class alternative in the

candidacy of Jeremy Corbyn. The Labor Party under Corbyn presented a progressive social democratic

program promising substantial and necessary increases in social welfare spending (health, education

and housing) to be funded by higher progressive taxes on the upper and upper middle class.

Corbyn's foreign policy promised to end the UK's involvement in imperial wars and to withdraw

troops from the Middle East. He also re-confirmed his long opposition to Israel's colonial land-grabbing

and oppression of the Palestinian people, as a principled way to reduce terrorist attacks at home.

In other words, Corbyn recognized that introducing real class-based politics would increase

voter participation. This was especially true among young voters in the 18-25 year age group, who

were among the UK citizens most harmed by the loss of stable factory jobs, the doubling of university

fees and the cuts in national health services.

In contrast, the French legislative elections saw the highest rate of voter abstention since

the founding of the 5 th Republic. These high rates reflect broad popular opposition to

ultra-neo-liberal President Francois Macron and the absence of real opposition parties engaged in

class struggle.

The lowest voter turn-out (28%) occurred in Puerto Rico. This reflects growing mass opposition

to the corrupt political elite, the economic depression and the colonial and semi-colonial offerings

of the two-major parties. The absence of political movements and parties tied to class struggle led

to greater reliance on direct action and voter abstention.

Clearly class politics is the major factor determining voter turnout. The absence of class struggle

increases the power of the elite mass media, which promotes the highly divisive identity politics

and demonizes left parties. All of these increase both abstention and the vote for rightwing politicians,

like Macron.

The mass media grossly inflated the significance of the right's election victories of the while

ignoring the huge wave of citizens rejecting the entire electoral process. In the case of the UK,

the appearance of class politics through Jeremy Corbyn increased voter turnout for the Labor Party.

However, Labor has a history of first making left promises and ending up with right turns. Any future

Labor betrayal will increase voter abstention.

The established parties and the media work in tandem to confine elections to a choreographed

contest among competing elites divorced from direct participation by the working classes. This effectively

excludes the citizens who have been most harmed by the ruling class' austerity programs implemented

by successive rightist and Social Democratic parties.

The decision of many citizens not to vote is based on taking a very rational and informed view

of the ruling political elites who have slashed their living standards often by forcing workers to

compete with immigrants for low paying, unstable jobs. It is deeply rational for citizens to refuse

to vote within a rigged system, which only worsens their living conditions through its attacks on

the public sector, social welfare and labor codes while cutting taxes on capital.

Conclusion

The vast majority of citizens in the wage and salaried class do not trust the political elites.

They see electoral campaigns as empty exercises, financed by and for plutocrats.

Most citizens recognize (and despise) the mass media as elite propaganda megaphones fabricating

'popular' images to promote anti-working class politicians, while demonizing political activists

engaged in class-based struggles.

Nevertheless, elite elections will not produce an effective consolidation of rightwing rule. Voter

abstention will not lead to abstention from direct action when the citizens recognize their class

interests are in grave jeopardy.

The Macron regime's parliamentary majority will turn into an impotent minority as soon as he tries

carry out his elite promise to slash the jobs of hundreds of thousands of French public sector workers,

smash France's progressive labor codes and the industry-wide collective bargaining system and pursue

new colonial wars.

Puerto Rico's profound economic depression and social crisis will not be resolved through a referendum

with only 28% of the voter participation. Large-scale demonstrations will preclude US annexation

and deepen mass demands for class-based alternatives to colonial rule.

Conservative rule in the UK is divided by inter-elite rivalries both at home and abroad. '

Brexit' , the first step in the break-up of the EU, opens opportunities for deeper class struggle.

The social-economic promises made by Jeremy Corbyn and his left-wing of the Labor Party energized

working class voters, but if it does not fundamentally challenge capital, it will revert to being

a marginal force.

The weakness and rivalries within the British ruling class will not be resolved in Parliament

or by any new elections.

The demise of the UK, the provocation of a Conservative-DUP alliance and the end of the EU (BREXIT)

raises the chance for successful mass extra-parliamentary struggles against the authoritarian neo-liberal

attacks on workers' civil rights and class interests.

Elite elections and their outcomes in Europe and elsewhere are laying the groundwork for a revival

and radicalization of the class struggle.

In the final analysis class rule is not decided via elite elections among oligarchs and their

mass media propaganda. Once dismissed as a 'vestige of the past', the revival of class struggle is

clearly on the horizon.

A much needed analysis by Mr. Petras. Here in Brazil it is becoming increasingly apparent that

extra-electoral manifestations are the only path left for the destitute classes. The only name

to which the Left seems able to garner votes is the eternal Luiz da Silva, who has pandered to

Capital all through his political career, and will possibly become inelectable anyway, by upcoming

criminal convictions.

"In the final analysis class rule is not decided via elite elections among oligarchs and their

mass media propaganda. Once dismissed as a 'vestige of the past', the revival of class struggle

is clearly on the horizon."

Globalism is the new Feudalism. In the U.S. the serfs still think they are "middle class".

Only the working class can help the working class. This truism is being re-learned.

We see in any country with a district voting system how democracy does not function: USA, GB

and France.

The Dutch equal representation system is far superior, the present difficulties of forming a government

reflect the deep divisions in Dutch society.

These deep divisions should be clear anywhere, now that the struggle between globalisation and

nationalism is in full swing.

The vast majority citizens (sic) in the wage and salaried class do not trust the

political elites. They see electoral campaigns as empty exercises, financed by and for plutocrats.

And they'd be correct.

What amazes me is how many "professional" people still smugly retain faith in an obviously

rigged and parasitic system even as their independence is relentlessly eroded. Also, most of them,

even the non-TV watchers, seem to slurp the usual propaganda about who the enemies supposedly

are.

Self reflection obviously ain't their shtick. Maybe there's comfort in denial and mythology.

The DUP would be very quick to insist that they are not para-militaries. As would their Tweedledee,

Sinn F�in (invariably referred to as 'Sinn-F�in-I-R-A' by the Unionist factions; not even banter).

It is undeniable that in the past they have had links to UVF/UDA, both straight-up rightwing

paramilitary thug outfits formed to mirror and combat the Provisionals and latterly the Continuity

IRA and self-styled "Real IRA" nationalist/socialist thugs. And presumably do so to this day.

"Everybody knows" that each political group is pretty much furtively hand-in-glove with their

respective heavy mobs, and who's in which one. It's a wee tiny place, the Six Counties.

Corbyn has definitely struck a rich vein of popularity (if not populism) among the "don't vote

it just encourages them" tendency, and a healthy majority of wealthy and not so wealthy young

Brits. Listen to the Glasto crowd. He gets this everywhere now in public (and maybe at home, IDK).

Remarkable transformation for somebody who only few years ago was a dull grey teadrinker from

Camden Council, with a half-century-old cardigan and a Catweazle beard.

Even The Demon Blair could never raise this sort of adulation.

I want to like the article, but Petras gives three examples, all of which are bad examples

for different reasons.

In the case of Puerto Rico, opposition parties campaigned, not for people to vote and to vote

against the government position, but to abstain altogether. This is a long standing political

tactic of opposition parties and other examples can be found. Its not used that often because

its usually a better tactic to just try to get people to get out and vote against the government.

However, it can work if there is a minimum turnout requirement for the election to be valid, which

is often the case in referenda and seems to be here. But this is evident of people rejecting the

government position, not the entire system. Voters obviously responded to the pro-Commonwealth

status campaign. By the way, usually referenda on things like independence, or in this case statehood,

get unusually high turnout, it was the opposite this time because of the opposition tactic.

On the other hand, in the 2017 French elections there really was a high amount of non-organized

or dis-organized abstention on the part of pissed off voters. The problem with Petras account

is that this was in fact widely covered in French media and by French political analysts, with

commentary along the lines of "these people must be really pissed off not to vote!".

In the recent UK elections turnout was both quite high and increased, so I have no idea wtf

Petras is talking about here.

If the examples used weren't so ridiculously bad the article could be OK I guess.

High abstention rates occur when big chunks of the electorate suspect that the elections are

rigged, usually by means of vote counting fraud, but effective or legal restrictions on who can

run or who can vote can do the job. The rigging might even take the form of discarding ballots,

which is the most common form in the US, which means turnout would be recorded as low even if

people tried to vote!

Keep in mind that with universal suffrage, it seems consistently that about a quarter of the

electorate has no interest in participating in electoral politics whatever the situation. If forced

to vote by law, they will spoil their ballots, vote for parties that campaign to end the democratic

system, or not vote anyway and suffer whatever legal penalties are imposed. Reasonably healthy

democracies can get to turnouts of around 70% fairly consistently. Anything less should be taken

as evidence of widespread electoral fraud.

Modern "Democracy" is a system for privatizing power and socializing responsibility. The

elites get the power, the masses have to take responsibility for the consequences. because, of

course, it's a 'democracy.'

Bottom line: political systems are to a great extent irrelevant. Putting your faith in any

system: monarchy, socialism, representative democracy, parliamentary democracy, checks and balances,

etc., is a mistake. There is (almost) no system that cannot be made to muddle through if the elites

have some consideration for the society as a whole. And there is absolutely no system that cannot

be easily corrupted if the elites care only about themselves.

In nearly the whole of S America elections just reflect the struggle between two or more

groups of rich people for power.

The same could be said for the revolution of 1776, and it continues in the US today.

I said, "No, there is a great difference. Taft is amiable imbecility. Wilson is willful

and malicious imbecility and I prefer Taft."

Roosevelt then said : "Pettigrew, you know the two old parties are just alike. They are both

controlled by the same influences, and I am going to organize a new party " a new political

party " in this country based upon progressive principles.

"Roosevelt then said : "Pettigrew, you know the two old parties are just alike. They are both

controlled by the same influences "

- R. F. Pettigrew, "Imperial Washington," The story of American Public life from 1870 to

1920 (1922), p 234

I recommend not voting because it is not ethical to send a non-corrupt person to Washington.

The United States is too powerful.

Good recommendation and for a good reason.

I'd say that it's unethical to send anyone to Washington since there is too much wealth and

power concentrated in the hands of too few, ethical or not.

In fact, the record shows that few men are worthy to wield much power at all and a system such

as we have is almost guaranteed to produce hideous, irresponsible monsters if not downright sadistic

ones (like Hillary, for instance).

Instead of talking about draining the swamp, we should have flushed the toilet long go. Now

we have to live with the stench.

The primary reason why lots of working class people don't vote is because they dislike the

liberal policy combinations offered by the elite-controlled political parties. Most working class

people are socially conservative and economically moderate, while most wealthy, educated people

are socially and economically liberal, so mainstream political parties only offer liberal policy

packages.

Modern representative democracy was designed in the late 19th Century to allow for some democratic

representation for the middle class while protecting the bourgeois elites from the rule of the

mob. That may have been a reasonable concern at the time, but it now means tyranny of the liberal

elites.

The solution is to reduce the power of political parties, either by making political parties

more accountable to their grass roots supporters or getting rid of political parties and directly

electing government ministers.

@eD A well informed comment without the kind of Marxist or other blinkers on that Petras wears.

But I question the last sentence. Electoral fraud could work to add votes as well as destroy or

lose them and vigilance is needed anyway. Are there highly numerate and worldly wise psephologists

with adequate research funding who are acting plausibly to keep a check on the way the bureaucratic

guardians of our electoral processes do their job? (All sorts of factors could make a big difference

in the proportion who vote. Is it part of the culture one was bro�ght up in to believe that one

had a duty to do one's modest best to participate? Are there a lot of elections at sometimes inconvenient

times within a short space of time? Is there a genuine problem deciding between the only candidates

who might win on either grand moral or national policy grounds or even simple self interest? Is

it assumed only one candidate can possibly win the seat? That last is one of the few arguments

for proportional representatiion because a dutiful voter who has a preference for one party will

make his infinitesimal contribution by voting).

Even Australia with its 80 to 90+ per cent turnouts to vote in sometimes complicated elections

with mixed Alternative Vote/Preferential and proportional representation for the different houses

of parliament (and not much "informal" voting as protest) exhibits the growing weaknesses of democracies.

That is, as I propose to write in another comment, the corruption of respect for the oligarchs

(whether traditional upper and upper middle classes or labour bosses), the replacement of the

class that went into politics as a duty by professiinal calculating careerists � plus opportunistic

extremists � and the growth of a sense of entitlement which ptobably adds up by now to 150 per

cent of all that is or can be. Thanks to China's huge appetite for Australian resources and products

Australian democracy can stagger on with scope even for absurd fantasies e.g. about Australia's

proper level of masochism in rejecting coal for energy when it can make absolutely no difference

to Australia � except to make it poorer.

@unpc downunder Your version of history differs from mine. 1832 and even 1867 in the UK still

built in some protection from the unpropertied lower orders (and 100 per cent from women � publicly

anyway) but Australian colonial suffrage was typically the alarming manhood suffrage with only

property qualification for some upper house elections as a break on the masses' savage expropriatory

instincts � not too much to be feared amongst ambitious colonial strivers in fact. The general

assumption that everyone with an IQ of 100 and a degree in Fashionable Jargon-ridden Muddled Thinking

is as worth listening to as anyone from the tradional educated bougeois or landed elite has inevitably

put politics into the hands of the ruthless, often arriviste careerists.

Please think again about your last par. which I suggest is a prescription for (even worse)

disaster. The idea of getting rid of political parties (how?) is as unrealistic as having the

bored populace vote directly for membership of the executive government who, in parliamentary

systems at least, have to command legislative majorities to be effective. And why do you think

responsiveness to those few who join political parties is likely to benefit the wider public when

you consider what has been wrought in the UK Labour Party by election of the leader by a flood

of new young members wlling to pay �3 to join!! I believe the Tories have also moved in that idiotic

direction. Imagine even the comparatively simple business of making motor cars being headed by

a CEO who had campaigned for votes amingst all workers who had been employed for more than 4 weeks

with promises of squeezing shareholders and doubling wages.

@jilles dykstra Your observation seems to depend for its truth on people (and you?) seeing

politics and national life as a zero sum game with no chance of increase in wealth or other good

things of life. That seems to be a logical attitude only in countries which sre still Malthusian

like say Niger with its TFF of 7! Is that a tealistic assessment of 2017 South America, or most

of it?

@jilles dykstra We see in any country with a district voting system how democracy does not

function: USA, GB and France.

The Dutch equal representation system is far superior, the present difficulties of forming a government

reflect the deep divisions in Dutch society.

These deep divisions should be clear anywhere, now that the struggle between globalisation and

nationalism is in full swing. I had in mind your comment when writing part of my last par in #17

which I won't repeat.

But allow me to expŕess astonishment at the idea that a truly sovereign nation benefits from

an electoral system which so represents irreconcilable differences in society that a government

cannot be formed. The Netherlands comfortable position as a minor feature of the EU makes it perhaps

less of a problem than, at least potentially, it is for Israel. Whenever Israel handles anything

really stupidly it is a good bet that it is during wrangling over putting together a majority

government.

Another problem with PR well illustrated by Israel that you don't mention is that citizens

have no local member who has to show that he cares about his constituents' concerns and actually

gets to know about them. That, for the average citizen has to be a really important matter. In

Australia we have just seen a pretty dodgy Chinese government aligned businessman/ donor to the

New South Wales Labor Party rewarded with nomination to a winnable place in the PR election of

the Senate. There is no way he would be put forward to win votes in a local electorate of thousands

of voters rather than millions.

We have just witnessed one of the most significant steps toward a one world

economic system that we have ever seen. Negotiations for the Trans-Pacific Partnership

have been completed, and if approved it will create the largest trading bloc

on the planet. But this is not just a trade agreement. In this treaty, Barack

Obama has thrown in all sorts of things that he never would have been able to

get through Congress otherwise. And once this treaty is approved, it will be

exceedingly difficult to ever make changes to it. So essentially what is happening

is that the Obama agenda is being permanently locked in for 40 percent of the

global economy.

The United States, Canada, Japan, Mexico, Australia, Brunei,

Chile, Malaysia, New Zealand, Peru, Singapore and Vietnam all intend to sign

on to this insidious plan. Collectively, these nations have a total population

of about 800 million people and a combined GDP of approximately 28 trillion

dollars.

In hailing the agreement, Obama said, "Congress and the American people

will have months to read every word" before he signs the deal that he described

as a win for all sides.

"If we can get this agreement to my desk, then we can help our businesses

sell more Made in America goods and services around the world, and we can

help more American workers compete and win," Obama said.

Sadly, just like with every other "free trade" agreement that the U.S. has

entered into since World War II, the exact opposite is what will actually happen.

Our trade deficit will get even larger, and we will see even more jobs and even

more businesses go overseas.

But the mainstream media will never tell you this. Instead, they are just

falling all over themselves as they heap praise on this new trade pact. Just

check out a couple of the headlines that we saw on Monday�

Overseas it is a different story. Many journalists over there fully recognize

that this treaty greatly benefits many of the big corporations that played a

key role in drafting it. For example, the following comes

from a newspaper in Thailand�

You will hear much about the importance of the TPP for "free trade".

The reality is that this is an agreement to manage its members' trade

and investment relations - and to do so on behalf of each country's most

powerful business lobbies.

Packaged as a gift to the American people that will renew industry and

make us more competitive, the Trans-Pacific Partnership is a Trojan horse.

It's a coup by multinational corporations who want global subservience to

their agenda. Buyer beware. Citizens beware.

The gigantic corporations that dominate our economy don't care about the

little guy. If they can save a few cents on the manufacturing of an item by

moving production to Timbuktu they will do it.

Over the past couple of decades, the United States has lost tens of thousands

of manufacturing facilities and millions of good paying jobs due to these "free

trade agreements". As we merge our economy with the economies of nations where

it is legal to pay slave labor wages, it is inevitable that corporations will

shift jobs to places where labor is much cheaper. Our economic infrastructure

is being absolutely eviscerated in the process, and very few of our politicians

seem to care.

Once upon a time, the city of Detroit was the greatest manufacturing city

on the planet and it had the highest per capita income in the entire nation.

But today it is a rotting, decaying hellhole that the rest of the world laughs

at. What has happened to the city of Detroit is happening to the entire nation

as a whole, but our politicians just keep pushing us even farther down the road

to oblivion.

Just consider what has happened since NAFTA was implemented. In the year

before NAFTA was approved, the United States actually had a trade surplus

with Mexico and our trade deficit with Canada was only 29.6 billion dollars.

But now things are very different. In one recent year, the U.S. had a combined

trade deficit with Mexico and Canada of

177 billion dollars.

And these trade deficits are not just numbers. They represent real jobs that

are being lost. It has been estimated that the U.S. economy loses

approximately 9,000 jobs for every 1 billion dollars of goods that are imported

from overseas, and one professor has estimated that cutting our trade deficit

in half would create

5 million more jobs in the United States.

Just yesterday, I wrote about how there are

102.6 million working age Americans that do not have a job right now. Once

upon a time, if you were honest, dependable and hard working it was easy to

get a good paying job in this country. But now things are completely different.

Why aren't more people alarmed by numbers like this?

And of course the Trans-Pacific Partnership is not just about "free trade".

In one of my

previous articles, I explained that Obama is using this as an opportunity

to permanently impose much of his agenda on a large portion of the globe�

It is basically a gigantic end run around Congress.

Thanks to leaks, we have learned that so many of the things that Obama has

deeply wanted for years are in this treaty. If adopted, this treaty

will fundamentally change our laws regarding Internet freedom, healthcare,

copyright and patent protection, food safety, environmental standards, civil

liberties and so much more. This treaty includes many of the rules

that alarmed Internet activists so much

when SOPA was being debated, it would essentially ban all "Buy American"

laws, it would give Wall Street banks much more freedom to trade risky

derivatives and it would force even more domestic manufacturing offshore.

The Republicans in Congress foolishly gave Obama

fast track negotiating authority, and so Congress will not be able to change

this treaty in any way. They will only have the opportunity for an up or down

vote.

I would love to see Congress reject this deal, but we all know that is extremely

unlikely to happen. When big votes like this come up, immense pressure is put

on key politicians. Yes, there are a few members of Congress that still have

backbones, but most of them are absolutely spineless. When push comes to shove,

the globalist agenda always seems to advance.

Meanwhile, the mainstream media will be telling the American people about

all of the wonderful things that this new treaty will do for them. You would

think that after how badly past "free trade" treaties have turned out that we

would learn something, but somehow that never seems to happen.

The agenda of the globalists is moving forward, and very few Americans seem

to care.

First of all, because NAFTA means jobs. American jobs, and good-paying

American jobs. If I didn't believe that, I wouldn't support this agreement.

Freddie

Many of those NeoCon Bibi lovers and Jonathan Pollard conservatives love

TPP and H1B Ted Cruz. Ted is also a Goldman Sachs boy.

Squids_In

That giant sucking sound just got gianter.

MrTouchdown

Probably, but here's a thought:

It might be a blowing sound of all things USA deflating down (in USD

terms) to what they are actually worth when compared to the rest of the

world. For example, a GM assembly line worker will make what an assembly

line worker in Vietnam makes.

This will, of course, panic Old Yellen, who will promptly fill her diaper

and begin subsidizing wages with Quantitative Pleasing (QP1).

Buckaroo Banzai

If this gets through congress, the Republican Party better not bother

asking for my vote ever again.

Chupacabra-322

Vote? You seem to think "voting" will actually influence actions / Globalists

plans which have been decades in the making amoungst thse Criminal Pure

Evil Lucerferian Psychopaths hell bent on Total Complete Full Spectrum World

Domination.

Yea, keep voting. I'll be out hunting down these Evil doers like the

dogs that they are.

Buckaroo Banzai

I have no illusions regarding the efficacy of voting. It is indeed a

waste of time.

What I said was, they better not dare even ASK for my vote.

Ignatius

Doesn't matter. Diebold is so good at counting that you don't even need

to show up at the polls anymore. It's like a miracle of modern technology.

Peter Pan

Did the article say 40%?

I imagine they meant 40% of whatever is left after we all go to hell

in a hand basket.

Great day for the multinationals and in particular the pharmaceutical

companies.

"... While cheaper fuel is a boost to consumer spending power in much of the developed world, it is also a disinflationary force that reinforces bets on loose monetary policy in Europe, Japan and China, even as the Federal Reserve proceeds with glacial tightening. ..."

While cheaper fuel is a boost to consumer spending power in much of the developed world,

it is also a disinflationary force that reinforces bets on loose monetary policy in Europe, Japan

and China, even as the Federal Reserve proceeds with glacial tightening.

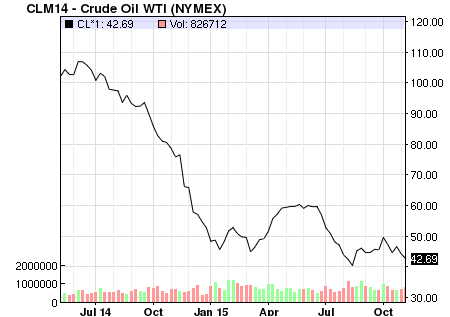

Oil prices are ending the year how they began - under pressure.

...Already, investment is

estimated to have dropped by 20% in 2015, and that is just the beginning.

This unfolding collapse of oil and gas investments, of course, will ricochet through the

capital goods and heavy construction sectors with gale force. Eventually, annual investment

may decline by $250 to $400 billion before balance is restored, meaning that what were windfall profits

and surging wages and bonuses in these sectors just a year or two back will evaporate in the years

ahead.

... ... ...

... as the credit bubble begins to shrink it means that profits, incomes, balance sheets

and credit-worthiness are all shrinking, too. So is the related GDP.

But now the days of heady accumulation of "sovereign wealth" in Saudi Arabia, Norway, Kazakhstan

and dozens of commodity producers in between is over and done. What is happening is that these funds

are entering a cycle of liquidation which is unprecedented in financial history.

Indeed, the data for Saudi Arabia, Qatar, Kuwait, the UAE and other members of the Gulf Cooperation

Council (GCC) is stunning. During the global credit boom they amassed sovereign wealth funds totaling

$2.3 trillion. But with deficits now estimated at 13% of GDP and rising, the level of asset liquidation

is soaring.

Thus, if crude oil prices recover to $56 per barrel next year, the GCC states will need to liquidate

$208 billion of investments.

... ... ...

In a word, the unnatural Big Fat Bid of the sovereign wealth funds is going All Offers as oil

and commodity producers struggle to fund their budgets.

... ... ...

Jack Burton

ENERGY Sector "what were windfall profits and surging wages and bonuses in these sectors just

a year or two back will evaporate in the years ahead."

This is already crushing Canada and North Dakota, whose actual oil field cut backs are only now

beginning as they tried to produce their way out of the debt crisis. But the hedges have run out,

prices seem glued to the basement and NOW the time has come to eliminate the expeditures. That

mean people losing jobs all up and down the line.

Stockman is brilliant here, as always.

I was watching "The Big Short" last night too. Excellent film. Very historic and everyone should

watch it.

"... the ideal markets that would produce Pareto Optimal allocations don't actually exist ..."

"... moving from actually existing non-ideal markets to ideal markets WOULD NOT BE Pareto Optimal even if it was possible to do so, which it isn't. ..."

"... In short, Pareto Optimality is a just so story that has absolutely no bearing on the real world other than as an ideological justification for tons of bullshit. ..."

"... The next step in graduate students' indoctrination is to teach them that although Pareto Optimal reallocations are implausible, you can get around that with a "principle of compensation." The principle, too is based on a same yardstick fallacy. But never mind the Pareto Optimality smokescreen and the compensation smokescreen have constrained economists to think in terms of doing what is best for the wealthiest. Funny how that happens. ..."

"Graduate students of economics learn, early in their careers, that markets allocations are Pareto

Optimal."

What they don't learn is that

1. the ideal markets that would produce Pareto Optimal allocations don't actually exist

and

2. moving from actually existing non-ideal markets to ideal markets WOULD NOT BE Pareto Optimal

even if it was possible to do so, which it isn't.

In short, Pareto Optimality is a just so story that has absolutely no bearing on the real

world other than as an ideological justification for tons of bullshit.

The next step in graduate students' indoctrination is to teach them that although Pareto Optimal

reallocations are implausible, you can get around that with a "principle of compensation." The

principle, too is based on a same yardstick fallacy. But never mind the Pareto Optimality smokescreen

and the compensation smokescreen have constrained economists to think in terms of doing what is

best for the wealthiest. Funny how that happens.

The next step in graduate students' indoctrination is to teach them that although Pareto

Optimal reallocations are implausible, you can get around that with a "principle of compensation."

The principle, too is based on a same yardstick fallacy. But never mind the Pareto Optimality

smokescreen and the compensation smokescreen have constrained economists to think in terms

of doing what is best for the wealthiest....

Richest in U.S. Shape Private Tax System to Save Billions

By NOAM SCHEIBER and PATRICIA COHEN

The very wealthiest families are able to quietly shape tax policy that will allow them

to shield millions, if not billions, of their income using maneuvers available only to several

thousand Americans.

Supposing I understand the essay, Roger Farmer is just writing the logical justification

to Herbert Spencer's (never Charles Darwin's) "survival of the fittest" rationale that Spencer

made wildly popular after Darwin published "On the Origin of Species."

Spencer was the successful ultimate justifier of British "sun-never-setting-on-the-Empire"

capitalism. Spencer sold a biological justification, Farmer is selling a logical justification

of Empire.

No, I think Farmer is dissing Pareto Optimality and using "sunspots" as sarcasm. He seems

to do it in a way that opens up space for countless side arguments that leave Pareto

Optimality unscathed.

The bottom line is that NO ONE would have ever paid any attention to the not just

"weak" but nonsensical concept if it didn't serve the function of justifying and ultimately

glorifying great inequalities of wealth and income.

;

I understand the argument and I am entirely right:

Roger Farmer is just writing the

logical justification to Herbert Spencer's (never Charles Darwin's) "survival of the

fittest" rationale that Spencer made wildly popular after Darwin published "On the Origin

of Species."

Spencer was the successful ultimate justifier of British "sun-never-setting-on-the-Empire"

capitalism. Spencer sold a biological justification, Farmer is selling a logical justification

of Empire capitalism.

I needed to be sure the argument was as empty morally as I supposed initially, but I

supposed correctly. The Roger Farmer essay is an amoral logical justification of imperial

capitalism. Plato's "Republic" conceived amorally. ;

Farmer is dissing Pareto Optimality and using "sunspots" as sarcasm. He seems to do it

in a way that opens up space for countless side arguments that leave Pareto Optimality

unscathed.

The bottom line is that NO ONE would have ever paid any attention to the

not just "weak" but nonsensical concept if it didn't serve the function of justifying

and ultimately glorifying great inequalities of wealth and income.

[ Agreed completely, but this argument runs with mine. ]

Farmer is dissing Pareto Optimality and using "sunspots" as sarcasm. He seems to do it

in a way that opens up space for countless side arguments that leave Pareto Optimality

unscathed....

[ The issue is that Roger Farmer leaves Pareto Optimality unscathed,

and this is an essential point. The essay is beyond the morality of now, but there is

no beyond. ]

"... the ideal markets that would produce Pareto Optimal allocations dont actually exist ..."

"... moving from actually existing non-ideal markets to ideal markets WOULD NOT BE Pareto Optimal even if it was possible to do so, which it isnt. ..."

"... In short, Pareto Optiimality is a just so story that has absolutely no bearing on the real world other than as an ideological justification for tons of bullshit. ..."

"... The next step in graduate students indoctrination is to teach them that although Pareto Optimal reallocations are implausible, you can get around that with a principle of compensation. The principle, too is based on a same yardstick fallacy. But never mind the Pareto Optimality smokescreen and the compensation smokescreen have constrained economists to think in terms of doing what is best for the wealthiest. Funny how that happens. ..."

"Graduate students of economics learn, early in their careers, that markets allocations are Pareto

Optimal."

What they don't learn is that

1. the ideal markets that would produce Pareto Optimal allocations don't actually exist

and

2. moving from actually existing non-ideal markets to ideal markets WOULD NOT BE Pareto Optimal

even if it was possible to do so, which it isn't.

In short, Pareto Optimality is a just so story that has absolutely no bearing on the real

world other than as an ideological justification for tons of bullshit.

The next step in graduate students' indoctrination is to teach them that although Pareto Optimal

reallocations are implausible, you can get around that with a "principle of compensation." The

principle, too is based on a same yardstick fallacy. But never mind the Pareto Optimality smokescreen

and the compensation smokescreen have constrained economists to think in terms of doing what is

best for the wealthiest. Funny how that happens.

The next step in graduate students' indoctrination is to teach them that although Pareto

Optimal reallocations are implausible, you can get around that with a "principle of compensation."

The principle, too is based on a same yardstick fallacy. But never mind the Pareto Optimality

smokescreen and the compensation smokescreen have constrained economists to think in terms

of doing what is best for the wealthiest....

Richest in U.S. Shape Private Tax System to Save Billions

By NOAM SCHEIBER and PATRICIA COHEN

The very wealthiest families are able to quietly shape tax policy that will allow them

to shield millions, if not billions, of their income using maneuvers available only to several

thousand Americans.

Supposing I understand the essay, Roger Farmer is just writing the logical justification

to Herbert Spencer's (never Charles Darwin's) "survival of the fittest" rationale that Spencer

made wildly popular after Darwin published "On the Origin of Species."

Spencer was the successful ultimate justifier of British "sun-never-setting-on-the-Empire"

capitalism. Spencer sold a biological justification, Farmer is selling a logical justification

of Empire.

No, I think Farmer is dissing Pareto Optimality and using "sunspots" as sarcasm. He seems

to do it in a way that opens up space for countless side arguments that leave Pareto

Optimality unscathed.

The bottom line is that NO ONE would have ever paid any attention to the not just

"weak" but nonsensical concept if it didn't serve the function of justifying and ultimately

glorifying great inequalities of wealth and income.

;

I understand the argument and I am entirely right:

Roger Farmer is just writing the

logical justification to Herbert Spencer's (never Charles Darwin's) "survival of the

fittest" rationale that Spencer made wildly popular after Darwin published "On the Origin

of Species."

Spencer was the successful ultimate justifier of British "sun-never-setting-on-the-Empire"

capitalism. Spencer sold a biological justification, Farmer is selling a logical justification

of Empire capitalism.

I needed to be sure the argument was as empty morally as I supposed initially, but I

supposed correctly. The Roger Farmer essay is an amoral logical justification of imperial

capitalism. Plato's "Republic" conceived amorally. ;

Farmer is dissing Pareto Optimality and using "sunspots" as sarcasm. He seems to do it

in a way that opens up space for countless side arguments that leave Pareto Optimality

unscathed.

The bottom line is that NO ONE would have ever paid any attention to the

not just "weak" but nonsensical concept if it didn't serve the function of justifying

and ultimately glorifying great inequalities of wealth and income.

[ Agreed completely, but this argument runs with mine. ]

Farmer is dissing Pareto Optimality and using "sunspots" as sarcasm. He seems to do it

in a way that opens up space for countless side arguments that leave Pareto Optimality

unscathed....

[ The issue is that Roger Farmer leaves Pareto Optimality unscathed,

and this is an essential point. The essay is beyond the morality of now, but there is

no beyond. ]

"... Emerging market companies with debt in dollars and revenue in sinking local currencies could struggle as the Fed begins what is expected to be a series of interest rate increases. ..."

Added to that, growth in global trade has slowed considerably and a decline in raw material prices

was posing problems for economies reliant on commodities, while many countries still had weak financial

sectors as the financial risks increase in emerging markets, she said.

"All of that means global growth will be disappointing and uneven in 2016," Lagarde said, noting

that mid-term prospects had also weakened as low productivity, ageing populations and the effects

of the global financial crisis dampened growth. In October, the IMF forecast that the world economy

would grow by 3.6% in 2016.

... ... ....

Emerging market companies with debt in dollars and revenue in sinking local currencies could

struggle as the Fed begins what is expected to be a series of interest rate increases.

Lagarde warned that rising US interest rates and a stronger dollar could lead to companies defaulting

on their payments and that this could "infect" banks and states.

"... The obvious candidate for this dark force [correlation between (rising) inequality and (low) growth] is crony capitalism. When a country succumbs to cronyism, friends of the rulers are able to appropriate large amounts of wealth for themselves -- for example, by being awarded government-protected monopolies over certain markets, as in Russia after the fall of communism. That will obviously lead to inequality of income and wealth. It will also make the economy inefficient, since money is flowing to unproductive cronies. Cronyism may also reduce growth by allowing the wealthy to exert greater influence on political policy, creating inefficient subsidies for themselves and unfair penalties for their rivals. ..."

"... The real problem is that money does not go to where it should go, as we see for example in the United States. The money does not flow into the real economy, because the transmission mechanism is broken. That is why we have a bubble in the financial system. The answer is not to tighten monetary policy, but to reform monetary policy so as to ensure that the money gets to the right place... ..."

"... As Stiglitz notes, the transmission mechanisms are broken. Economists trickle down monetary policy might work in theory, but not in practice, as we have seen for the last seven years, when low rates dont trickle down and were wasted instead on asset speculation by the 1%. ..."

"... Reform of the Fed, and the end of cronyism are essential to making sure that the stimulus of low rates gets to Main Street, to ordinary people, and not primarily to asset speculators. ..."

"... The recent decision by the Fed to raise interest rates is the latest example of the rigged economic system. Big bankers and their supporters in Congress have been telling us for years that runaway inflation is just around the corner. They have been dead wrong each time. Raising interest rates now is a disaster for small business owners who need loans to hire more workers and Americans who need more jobs and higher wages. As a rule, the Fed should not raise interest rates until unemployment is lower than 4 percent. Raising rates must be done only as a last resort - not to fight phantom inflation. ..."

"... And in one sentence Summers illustrates exactly why we dodged a bullet in not appointing Summers to be Fed Chair. Preserving the power of the Fed is not the most important policy. Changing the Fed composition so that it is more consumer friendly and not dominated by Wall Street interests is the most important policy change needed. ..."

"... the Balkanized character of US banking regulation is indefensible and would be ended. The worst regulatory idea of the 20th century-the dual banking system-persists into the 21st. The idea is that we have two systems one regulated by the States and the Fed and the other regulated by the OCC so banks have choice. With ambitious regulators eager to expand their reach, the inevitable result is a race to the bottom. ..."

"... Summers is also calling for higher capital requirements. Excellent stuff! ..."

This is the beginning of a long response from Larry Summers to an op-ed by Bernie Sanders:

The Fed and Financial Reform

� Reflections on Sen. Sanders op-Ed

: Bernie Sanders had an

op Ed in the New York Times

on Fed reform last week that provides an opportunity to reflect

on the Fed and financial reform more generally. I think that Sanders is right in his central

point that financial policy is overly influenced by financial interests to its detriment and

that it is essential that this be repaired.

At the same time, reform requires careful reflection if it is not to be counterproductive.

And it is important in approaching issues of reform not to give ammunition to right wing critics

of the Fed who would deny it the capacity to engage in the kind of crisis responses that have

judged in their totality been successful in responding to the financial crisis.

The most important policy priority with respect to the Fed is protecting it from stone age

monetary ideas like a return to the gold standard, or turning policymaking over to a formula,

or removing the dual mandate commanding the Fed to worry about unemployment as well as inflation.

...

JohnH said...

Disagree!!! There is more to this than just interest rates. There is the matter of how the policy

gets implemented--who gets low rates. Currently the low rates serve mostly the 1%, who profit

enormously from them. Case in point: Mort Zuckerberg's 1% mortgage!

"The obvious candidate for

this dark force [correlation between (rising) inequality and (low) growth] is crony capitalism.

When a country succumbs to cronyism, friends of the rulers are able to appropriate large amounts

of wealth for themselves -- for example, by being awarded government-protected monopolies over

certain markets, as in Russia after the fall of communism. That will obviously lead to inequality

of income and wealth. It will also make the economy inefficient, since money is flowing to unproductive

cronies. Cronyism may also reduce growth by allowing the wealthy to exert greater influence on

political policy, creating inefficient subsidies for themselves and unfair penalties for their

rivals."

As we know (although most here steadfastly ignore it) the Fed is rife with crony capitalism.

As Bernie pointed out, 4 of the regional governors are from Goldman Sachs. Other examples are

abundant. Quite simply, the system is rigged to benefit the few, minimizing any potential trickle

down.

If a broad economic recovery is the goal, ending cronyism at the Fed is likely to be far more

effective that low interest rates channeled only to the 1%.

JohnH said in reply to JohnH...

Stiglitz:

The real problem is that money does not go to where it should go, as we see for example

in the United States. The money does not flow into the real economy, because the transmission

mechanism is broken. That is why we have a bubble in the financial system. The answer is not to

tighten monetary policy, but to reform monetary policy so as to ensure that the money gets to

the right place...

Small and medium enterprises cannot borrow money at zero interest rates -

not even a private person, I wish I could do that (laughs). I'm more worried about the loan interest

rates, which are still too high. Access for small and medium enterprises to credit is too expensive.

That's why it is so important that the transmission mechanism work..."

http://www.cash.ch/news/alle/stiglitz-billiggeld-lost-kein-problem-3393853-448

And let's not forget consumer credit rates, which barely dropped during the Great Recession

and are still well above 10%. Even mortgage lending, which primarily benefits the affluent, have

been stagnant for years despite historically low rates.

As Stiglitz notes, the transmission mechanisms are broken. Economists' trickle down monetary

policy might work in theory, but not in practice, as we have seen for the last seven years, when

low rates don't trickle down and were wasted instead on asset speculation by the 1%.

Reform of the Fed, and the end of cronyism are essential to making sure that the stimulus of

low rates gets to Main Street, to ordinary people, and not primarily to asset speculators.

Peter K. said in reply to JohnH...

Bernie Sanders:

"The recent decision by the Fed to raise interest rates is the latest example of the rigged

economic system. Big bankers and their supporters in Congress have been telling us for years

that runaway inflation is just around the corner. They have been dead wrong each time. Raising

interest rates now is a disaster for small business owners who need loans to hire more workers

and Americans who need more jobs and higher wages. As a rule, the Fed should not raise interest

rates until unemployment is lower than 4 percent. Raising rates must be done only as a last

resort - not to fight phantom inflation.

"

The financial system reform legislation in 2017 will also need to include these matters:

1.

Licensure fees and higher and more differential income taxation rates based on the type of financial

trading ratios the entities have (in order to direct more emphasis to real-economy lending and

away from speculative and leveraged positions used in the financial asset trading marketplaces,

so hedge funds probably would face the highest rates in income taxation). For a certain period

after enactment these added taxes would be payable by the banks using their excess reserves, which

will simply be eliminated until the reserve accounts return to the historically normal period

when excess reserves were very small (there would no longer be a need for IOER, as the excess

would be eliminated by operation of the taxation statutes). Attaching added ways & means statutes

to all the financial service entities also serves to 'cover' some more of huge financial risk

held by society and produced by them while the success of this huge sector actually contributes

to the financing of self-government - which is also an indirect way to attach high Net Worth being

used).

2. New statutory provisions need to reach any and all entities in the financial community regardless

of definitions based on the functions they serve or provide (or the way they are named - so yes,