|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

| Jan | Feb | Mar | Apr | May | June | July | Aug | Sep | Oct | Nov | Dec |

|

|

|

|

9/1/2010 | USATODAY.com

There are no visible picket signs on Wall Street. The U.S. stock market— the world's biggest when measured by the market value of the companies that trade here — still opens for business every trading day. And the 6 o'clock news still lets everyone know if the Dow finishes the day up or down.

Yet, increasingly, investors on Main Street are not playing the stock market game with confidence like they used to, mainly because the game of making money has gotten tougher and more volatile since the financial crisis. Retail investors are buying fewer stocks. They are paring back on stocks and stock funds they already own. Instead, they're moving into safer investments, like cash and bonds.

"Investors are on strike," says Axel Merk, president and chief investment officer at Merk Mutual Funds.

The fear on Wall Street is that this buyer's strike will linger for years, resulting in a lost generation of investors similar to what occurred after steep stock declines in the 1930s during the Great Depression and early 1970s, a recessionary time punctuated by high inflation.

Consider Stacy Harris, 58, from Nashville. While she's not totally out of the stock market, her cash stash has ballooned to 42% of her portfolio. That's twice as big as her slimmed-down stock holdings, now just 21% of her investment pie.

"I'm sitting on an uncomfortable amount of cash," says Harris, editor of Stacy's Music Row Report, an online publication that blogs about the country music scene. "Until things get better, I'm not putting any more money into stocks."

Another member of the shaken-investor class is Bill Woodward of Pittsburgh. He was once an avid stock investor. A decade ago, he used to troll stock chat rooms on the Internet in search of hot stocks. Now, his portfolio is down to three holdings: a dividend-paying oil tanker company, a fund that bets against the real estate market and a penny stock he calls his "lottery ticket."

He couldn't care less about the nearly 5,000 other stocks that trade on major U.S. exchanges. "I have no interest in coming back," says Woodward, 60, who works at a local employment center that helps people find jobs. His distrust of market regulators and his belief that they don't protect individual investors are the top reasons for his anti-stock stance.

It's hip to be conservative

After back-to-back stock market busts in a 10-year span in the 2000s, cocktail party chatter that once centered around get-rich-quick stocks has given way to sober chats about ways to reduce risk, the best places to stash cash and why it makes sense to buy boring bonds instead of sexy stocks. Days like Wednesday, when the Dow skyrocketed 255 points, are offset by months like August, when the Dow suffered its worst August drop since 2001.

Yanking cash out of the stock market for fear of losing it has been the trade of choice for Main Street investors since the start of 2009, when the fallout from the financial crisis made it clear stock prices don't always go up.

"The lost generation is not coming back," says Michael Panzner, who writes the blog Financial Armageddon.

Recent statistics paint a picture of retail investors in retreat. Nothing illustrates Main Street investors' diminished appetite for stocks more than the dollars flowing in and out of mutual funds. Since the beginning of 2008, stock mutual funds have suffered cash outflows totaling roughly $245 billion. In contrast, bond mutual funds have enjoyed inflows of close to $616 billion, according to data from the Investment Company Institute, a mutual fund industry trade group. Similarly, prior to the financial meltdown two years ago, 401(k) investors had seven of every 10 dollars of their retirement money invested in stocks, but that is back below 60%, according to Hewitt Associates.

Anti-stock sentiment is also evident in the soon-to-be-released 2010 Scottrade American Investor Study. While 73% said they still believe the stock market will produce long-term gains, 65% of investors polled said they were "very" or "somewhat stressed" about their current financial situation. The "economy" was the No. 1 source of that stress. Nearly one of three investors (31%) said they were "investing less money" or "investing more conservatively." The most conservative investors of all: Gen Y (18 to 28 years old) and Gen Xers (29-45), the study found.

Bad times for stocks

It's hard to blame individual investors for their growing skittishness toward stocks. They've endured not one but two of the worst stock market downturns in history — within a short 10-year span. The dot-com-inspired stock bubble burst in early 2000, knocking the broad stock market, as measured by the Standard & Poor's 500-stock index, down 49.1% by the time the bear market ended in 2002. That was followed by the 56.8% plunge from 2007-09, when a credit-driven bubble in stocks, real estate and many other assets ended badly.

As a result of the back-to-back bear markets, the Dow Jones industrial average is still trading just 270 points above the 10,000 level, a milestone it first attained to great fanfare back in 1999. Since the Oct. 9, 2007, high, the stock market's value has declined by $5.6 trillion, according to Wilshire Associates. "Investors are saying, 'Why would I want to put money into stocks? I'm still losing money,' " says Charles Biderman, director of research at TrimTabs, a firm that tracks fund cash flows.

Panzner ticks off three other key reasons Main Street investors have suddenly turned very risk-averse:

•Investors are trying to make sense of an unprecedented economic earthquake that has left them feeling blindsided and unsure about their economic futures like never before. Nearly 15 million are unemployed, and many have seen the value of their homes — typically their biggest investment — crater.

•There is a feeling among investors, Panzner says, that the investment "game is rigged" in favor of professional traders and money managers. The belief that the playing field is not level has created intense feelings of animosity toward Wall Street.

•The aging of the Baby Boomers has created a demographic headwind for the stock market."More people will be looking to draw down their savings," Panzner says. "As people get older, they will want to take less risk and protect their nest eggs."

And there's no guarantee that stocks will rebound strongly after major bear markets, as they have tended to do in the past. "Markets don't always go up," Merk warns. For proof, he points to the Nikkei 225, Japan's main blue-chip stock index. The index peaked on Dec. 29, 1989, at 38,915.87 before a multiyear asset bubble burst. On Wednesday, more than 20 years later, the Nikkei closed at 8927.02 — 77.1% below its record high.

Fears of another super swoon are what keep Ron Munn, a 69-year-old retiree from Green Valley, Ariz., up at night.

"As part of the 'Lost Generation,' now is certainly not the time to jump back in the market and possibly become part of the 'Gone Forever Generation,' " Munn says in an e-mail. "Keeping your powder dry with safe cash and bond investments makes sense under the current economic and political situation."

What will get investors back?

Despite all the doom and gloom, not everyone on Wall Street believes that investors will stay away from the stock market for years, if not decades.

"A lost generation? I don't buy it," says Jim Paulsen, chief investment strategist at Wells Capital Management. He says investors always say they hate stocks and that they "don't want to touch a stock" after a sharp downdraft. They said it after the 1973-74 bear market, they said it after the dot-com crash and they are saying it now. "I've heard this all before," he says.

What will bring the Main Street masses back to Wall Street?

Jobs. When hiring picks up, so will consumer and investor confidence. With that will come higher stock prices, Paulsen says."At this point we have ourselves in such a panic that the only tonic to calm mind-sets is you will need two, three and even four months in a row of 200,000-plus jobs created," Paulsen says. "If we get that, you could see a fairly violent move up in interest rates and stocks. But if jobs don't show, the depression mentality is going to grow."

A new bull market. Animal spirits will return when the stock market starts heading higher and your neighbor starts bragging about all the money she made in the market, says Michael Farr of money management firm Farr Miller & Washington. More days like Wednesday, when stocks soared 3%, are needed."We need a bull market somewhere in something," Farr says. "As soon as the guy next door is making a buck, investors' curiosity will be piqued," and they will regain their courage and start investing in stocks again.To drive home his point, he uses a casino analogy: "The reason slot machines have ringing bells and flashing lights" to announce a winner is that it "keeps everyone else pulling their handles. You don't have to be the one that wins, you just have to know someone is winning."

Clarity over government policy. All the question marks on government policy, ranging from taxes to financial regulation, are stifling business decision-making and innovation, Merk argues."A key ingredient to functioning markets is clarity," Merk says. "You need to know what the government is up to. But we just don't have that. Investors will come back to the business of investing when investment can take place based on analysis of businesses, rather than anticipating the next government intervention."

A resurgence of dividends. In a world where yield or income is gaining popularity at the same time that yields on government bonds are sinking to or near record lows, investors will be more apt to return to stocks if companies upped their dividend payouts, argues Jason Trennert of Strategas Research Partners."Retail investors have been traumatized by two 50% declines in stocks in the past 10 years, serial misdeeds on the part of Corporate America and Wall Street, and for anyone left, the flash crash," he says. "I've come to the conclusion that only dividends could immediately restore some confidence on the part of the investing public in stocks."

Single-digit P-Es. It might take a scary stock market swoon that knocks the price-to-earnings ratio back to single-digits to create a truly good entry point for investors, Panzner warns. In prior bear markets, stocks bottomed out in October 1974 at a P-E of 7 and in August 1982 at less than 8, InvesTech Research data show. Both lows set the market up for big gains over multiyear periods, including the 18-year bull run from 1982 to 2000. The S&P 500's current P-E, based on projected earnings over the next four quarters, is 12.7, according to Thomson Reuters. The long-term P-E is roughly 15. Getting back to single-digit P-Es is "the best prospect for getting a sustainable recovery," Panzner says. "Stocks have to get so cheap, so washed out and so hated," the only direction is up.

There's one more thing investors like Harris and Woodward would like to see before they would feel comfortable investing aggressively in stocks again: a stiff crackdown by the Securities and Exchange Commission on unscrupulous Wall Street types that prey on individual investors.

Says Woodward: "What would bring me back? Show me that the SEC is back to protecting the little guy."

Adds Harris: "I don't think we want to be in a position again where we have a guy like Bernie Madoff." Madoff orchestrated the biggest Ponzi scheme in history, robbing the financial futures of countless people.

For now, "Everyone is thinking more conservatively," Harris says. "They want to make sure their money is there when they need it."

montanavet3:

"Could investors fleeing stocks become a lost generation?" ++++++++++++++++ Take put the word "investors" and plug in "gambling addicts", and I say good riddance. But the stock market "investing/gambling" firms suck in new suckers every day with their slick TV ad campaigns .... now you even have them pushing AMATURES into CURRENCY trading .....

Sheep to slaughter ..... and the "killers'' laugh all the way to the bank!

John Pombrio:

Y'see, the problem is right there in the story. Stock Price=Profit. Sorry, not true. The price of a share of stock was NEVER meant to be "profitable". The COMPANY was to make the profits and DISTRIBUTE them to the shareholders as DIVIDENDS and with the shareholders helping to cover the risk of doing business. This core idea has been well and truly perverted in the past 20 years. It was the greed and the media that invented the stock market as a "Get Rich Quick" scheme when some of the internet and computer companies rang up such astounding profits in such a short time. Microsoft, Yahoo, Google. All of a sudden, the news started throwing the DOW in our face and how much profit some companies and investors were making. Thus started the great stampede to the stock market. Even boring companies were now faced with "WHERE'S MY PROFIT?" from their shareholders. Well, profits did rise by slashing headcount, acquiring other companies, or perhaps moving expenses to another year. CEO's were given huge incentives to rise the stock price by outrageous bribes of "options". Was all this "profit" good for the COMPANY, its CUSTOMERS, or the SHAREHOLDERS? You wonder why so many companies are now floundering with no trained people, few good customers, and a flat stock price. Will the market recover? I cannot see that happening for 10-15 years. Why? The US baby boomers are the richest generation that has ever lived on this planet. They have been burned badly 4 times in less than 10 years, 2 stock crashes, a housing crash, and finally a staggering loss of jobs. Like my parents who lived through the depression, that is a truly bitter lesson that they will remember for the rest of their lives. It will not be until an entirely new generation that will regard what we have been through as "history" that will start investing again. Hopefully, with a new maturity at the risks involved in investing and with an awareness that a good company to invest in is one that rewards the stockholders with dividends, not hyped up stock prices.

Ontopofit:

"His distrust of market regulators and his belief that they don't protect individual investors are the top reasons for his anti-stock stance."

Exactly, why put your money where a den of theives live?Jackov

:highlySkilled (0 friends, send message) wrote: 29m ago

The problem is that there is no longer a stock market to invest in.... what we have is wall street insiders racing Ferraris on a track they designed (directly connected hi frequency trading robots) and keep messing with in a game that has nothing and I mean nothing to do with investment or reasearch, and the rest of the so called non Wall Street "investors" are subjected to heavy marketing to come rent a Ford Pinto to race blindfold.

In short investment is the wrong name, Wall St is a fixed game for insiders to PLAY using outsider's money.

=============

You can invest directly in businesses or franchises--laundrymats, liquor stores, etc.RidingHigh:

The Stock Market was initially used for companies to raise capital in exchange for ownership - it gradually turned into a gambling parlor.

topdawg:

It's really pretty simple. The average investor on Main Street feels like he's been duped by the Wall Streeters. We play one game, while the big cats on Wall Street play an entirely different game where they know and make the rules. We lose, they win.

As the old saying goes, "Fool me once, shame on me ..................... "

larry elford:

the industry has earned it's "reputational bankruptcy" very well.

It will be safe to invest once again when those who tried to steal our economy are jailed, and those regulators who helped them, (or simply looked the other way) are also jailed for failure to protect the public interest. Until then, white collar crime is simply the best paying occupation in the world.

Larry Elford, Canada http://www.youtube.com/user/investoradvocate?fea ture=mhum

2 minute video on how to become an investment advisor (in canada) 4 minute video on how to commit the perfect crime BREACH OF TRUST, The Unique Violence of White Collar Crime, by a twenty year veteran broker turned whistleblower

NYTimes.com

.. Inequality in the United States has soared to levels comparable to those in Argentina six decades ago — with 1 percent controlling 24 percent of American income in 2007.

At a time of such stunning inequality, should Congress put priority on spending $700 billion on extending the Bush tax cuts to those with incomes above $250,000 a year? Or should it extend unemployment benefits for Americans who otherwise will lose them beginning next month?... ... ...

But there is also a larger question: What kind of a country do we aspire to be? Would we really want to be the kind of plutocracy where the richest 1 percent possesses more net worth than the bottom 90 percent?Oops! That’s already us. The top 1 percent of Americans owns 34 percent of America’s private net worth, according to figures compiled by the Economic Policy Institute in Washington. The bottom 90 percent owns just 29 percent.

... ... ...

And then I see members of Congress in my own country who argue that it would be financially reckless to extend unemployment benefits during a terrible recession, yet they insist on granting $370,000 tax breaks to the richest Americans. I don’t know if that makes us a banana republic or a hedge fund republic, but it’s not healthy in any republic.

pdxtran Minneapolis, November 18th

The right-wing media have encouraged the development of a Stockholm syndrome among middle class and working class Americans.

That is, an awful lot of people who earn closer to $25,000 than $250,000 a year are opposed to letting the Bush tax cuts expire and yet disparage the long-term unemployed and oppose any extension of unemployment benefits, blithely declaring that "there are plenty of jobs out there." They also make snide remarks about labor unions, negating the kind of cooperative efforts that forced the plutocrats of the 1930s through 1950s to share the wealth that their employees' labor had created.

I wonder what sort of psychological process is behind the people thus brainwashed.

Is it a belief that rich people work hard and poor people don't? (Riiight. All those trust fund babies work their fingers to the bone, and all those hotel maids and loading dock workers sit around all day.)

Is it a belief that the rich will create jobs if everyone thinks nice thoughts about the and gives them everything they want? (Thirty years and counting since Reagan first cut taxes on the top incomes. Where are the jobs?)

Is it a misguided jingoism, the kind of salute-the-flag-and-march-around patriotism that they used to teach when I was in grade school, a naive belief that America is always right about everything, and even if not, is always more virtuous than any other country?

Is it magical thinking, conceived in terms of, "If I despise poor people

and revere rich people enough, then God won't let me become poor"?

If they'd just look overseas (something that conservatives are loath to do), Americans could see the negative effects of income inequality.

The countries with the highest income inequality are terrific places to be rich. The super rich in those countries can buy clean water, education, medical care, and electricity privately, purchase anything they want cheaply, and hire servants for next to nothing. However, these countries are decidedly unpleasant for the 99% who can't afford to live in gated communities and also tend to have some of the world's highest crime rates and least stable political systems. Countries with high levels of inequality are dangerous places to live, especially if the lower classes have lost all hope of improving their lives by legal means.Tim Bal

Mr. Kristof is 100% right, but I would go a step further: our tax and trade policies promote this “hedge fund” characteristic.

The lower the tax on high income, the lower the disincentive to pay obscenely high income. There is a reason that CEOs made a lot less under Eisenhower: the top rate hit 92%. So, every dollar earned over $3.2 million (in 2010 dollars for joint tax returns; or joint income over $400,000 in 1952 dollars) was taxed at 92%, leaving only 8 cents for the CEO. So, corporate boards thought twice about essentially giving a raise to Uncle Sam.

This also was a disincentive to send millions of American jobs overseas. Since most of the profit in doing so would end up in the U.S. Treasury, there was no incentive to trade American jobs for CEO income.

Therefore, President Obama should veto any extension of the Bush tax cuts, and strive to raise the top tax rate to over 90%. CEOs would still be rich, as they were under Eisenhower, but the rest of us would benefit from a sane trade policy and the return of 20 million jobs to our nation. Not to mention the other benefits of lower budget and trade deficits. nuzumVery nice turn-of-the-tables Mr. Kristof. Thanks for doing a little fact-gathering and reporting that America is actually a tad worse than traditional banana republics. The operative word here is fact. Maybe you need to do another contest where you take dyed-in-the-wool, tax-obsessed TeeGOPers on a tour of the world. Show them how great public transportation can be in Europe or Asia, show them how awful conditions can be in rural Mexico or Guatemala or Sierra Leone, show them how communist China is out Adam Smithing capitalist America. Show them the horrors of loosely regulated polluters like in Hungary or in parts of Russia or India. Show them the Autobahn and lunch in a beer garden. Make sure they meet lots of people who can speak good English and also make them try from time to time to communicate with locals who don't know English. Show them things that put America in perspective. We have some great things and we have some awful things.

But politicians continually tell Americans that they are the greatest superhumans on the planet. Politicians stroke our egos, make us feel superior, when deep down inside I think most of us know the truth. We are just people.

People being usured out of our pitiful temp-job wages and nickel and dimed by insurance companies and bank account fees. We watch our tax dollars prop up mega businesses and financial hucksters and those same businesses return the favor by not refinancing mortgages and outsourcing jobs and lobbying against increases in minimum wages or health care or environmental protection or worker safety, etc. We are still seeing record profits from oil companies and banks. These two "industries" are our national problem and our national disgrace. Oil companies pump crude from national lands and then sell it back to us at $3 per gallon. They get subsidies to explore for more ways to do this. Banks get to borrow money from Us the People for almost 0% and then they lend it back to us at 20% or 30% in credit cards or 6% as a mortgage. Of course they won't refinance mortgages at 4%, they are making 6% now. If you have a mortgage that is too small, say under $150k then you are really out of luck. Your paperwork will never find the right slot. It simply won't ever see the light of day. Financial services only give you service if you have $500k in their system. Otherwise get ready to resubmit your paperwork multiple times and then get denied for a refinance that would lower your monthly payments. You were paying the high monthly payments on time, but apparently the bank thinks you won't be able to afford the lower monthly payments if they approve a refinance at a lower rate.

If evil is the absence of good, then I guess I know where evil resides.

Sorry I digressed, but the American myth is really annoying.

PLB

Napoleon Bonaparte, on bankers in general:

Money has no motherland; financiers are without patriotism and without decency; their sole object is gain.

from Liaquat Ahamed, Lords of Finance, the Bankers Who Broke the World

Hassan Azarm

Paul

The Bankers DNA is the main constant here as the times change they repeat the same sorry horror show albeit with different set of actors....

WE need Gene therapy/mutation for the Bankers and their political clients/benefactors/puppets.

Failing that I suggest straight jackets...

taopraxis:

Napoleon is also quoted as having said this: "Never interrupt your enemy when he is making a mistake," That comment captures the reasons why I do not think a revolution will ultimately be needed to topple the financial titans from their lofty perch.

Either the pyramid is expanded exponentially until the money becomes worthless or the banks and sovereigns default on their debts.

If the latter, then the endgame is more protracted, because the big players will endeavor to manage the default process. Markets will eventually panic either way, as the authorities have already lost too many pieces to reliably control the situation. The debts are simply too large to be unwound in an orderly restructuring.

The central banks are trapped, doomed to be hoisted on their own petard. Interest rates will eventually soar and the affected economies involved will be forced into the inevitable default/devaluation crisis.

Pay now or pay later.There is no exit from objective mathematical reality. The financial doomsday device was triggered a long time ago and there is no way to turn it off. Free thinkers are as prepared as they can be and have already stepped aside. The lemmings of the world are stampeding, oblivious, as always, as lemmings tend to be. Once they've vaulted the cliffs, things can get back to normal. A new generation and a new age will be born.

Economist's View

Matt Young:

First: 'Even if you attribute half of the rise in unemployment to structural factors, that still leaves between 2% and 3% of the rise in unemployment to cyclical problems.'

So the post introduces the possibility of structural problems in the economy.

But, half the economy is government itself, state, local, federal and transfer payments.

Hence, there may actually be a structural problem, and if we found one it likely would appear in the administration.

How would that structural problem appear? Maybe, politicians, in the administration, running around saying the government has a structural budget problem and unable to act without fixing it.

Maybe Obama actually is dealing with a long term structural problem in the federal budget, a possibility we might consider.

calmo said in reply to Matt Young...

Thanks for the reply, sure to make someone like anne scurry to the BLS and produce a barge full of stats on how exactly the gov slice has grown over the successive administrations...but not me...all these willing workers...I cannot crowd them out.

"First"..volley back to you, I suppose...waitin for your "Secondly", is me.

"So the post introduces the possibility of structural problems in the economy."

I would say this is a gracious given, (moreover, a pretext for action) not an introduction...and therefore grounds to chase (I would put Big Dog bakho on this, you?) down that 2 or 3%. Are you arguing that this is not the right chase or that gov cannot give chase or that, no matter how infinitesimal the structural component, it rules? It almost sounds like you are sayin, the budget will not allow this action. Ok, volley done.

Ok, with current 10% UE and the decompolation of that as much as 3% structural...leaves us with the cyclical 7%, --about twice the pre-recession levels, yes? Agree, ex-BLSly, (--somewhat empirically and somewhat more than merely anecdotally ...the information/views I get/form/fudge/factor here is pretty tight).

Matt Young said in reply to calmo...

ken melvinIf there is a structural problem it is likely hammering the Obama administration officials into desperation. So, the answer is Obama cannot act, he is in a fiscalidity trap.

The large states are near bankruptcy. The stimulus fix helped a bit by sending taxes from the feds to the states. But the problem is still there, unless the central government makes state subsidies permanent, the states are still headed toward bankruptcy. Structural

Summers @ Center for American Progress, Discussion on Jobs 4/3010From about 3:06 to 3:15 on the video

Social Consequences of downturn:

- Calls to domestic hotline up 50%:

- Loss of job: 2nd (close) only to death of a spouse, equivalent to divorce

Scope:

- Worse since WWII

- Normal Relationship of GDP to Unemployment did not hold

- Unemployment 1-1.5% greater than would normally be expected.

- Fewer people required to meet production reqmnt’s for increased demand.This means fewer jobs for the less educated worker;

- 40 yrs ago, at any given time, 1 in 20 adult males were out of workToday, at any given time, 1 in 5 adult males are out of work

- 5 yrs from now, after the recovery, at any given time, we can expect 1 in 6 adult males to be out of work, and 1 in 10 of those with college.

Causes:

- Technology (automation) less labor required to produce more

- Off shoring of low tech jobs due to globalization.

latimes.com

Three weeks ago the euro was hitting 11-month highs against the dollar, and a favorite meltdown scenario centered on the demise of the greenback. Now, it's the euro that is sinking fast — it fell to $1.324 on Friday from $1.367 a week ago and $1.421 on Nov. 4 — and it's no longer taboo in Europe to discuss ending the 12-year-old experiment with the common currency.

Whether that would be catastrophic for the global economy or even for Europe is far from clear. But it's understandable that anyone who's anticipating financial Armageddon would view the euro's sudden slide as confirmation.

It's human nature to see our present situation, and the future, through the prism of our recent experiences. After living through what was (or is) for many people the worst economic nightmare of their lives, it's not surprising that we're now constantly looking over our shoulders, fearful that another crisis is imminent.

In the economy and markets, "People are afraid that every little dip is going to be a collapse," Ritholtz said.

We all know that the U.S. economy has been badly wounded by the Great Recession. We know that the unemployment rate is 9.6% — 17% if you count the underemployed and those who have stopped looking for jobs.

The Internet also echoes with the pleas of about 2 million long-term unemployed who face a cutoff of jobless benefits Tuesday if Congress fails to vote for an extension.

It's painfully difficult to reconcile their plight with the fact that 140 million or more Americans are expected to be out in force shopping this weekend, hoping to give a decent holiday to their kids or other loved ones.

It's also difficult to reconcile the ongoing struggles of many small businesses with government data this week showing that U.S. companies' earnings reached an annualized rate of $1.66trillion in the third quarter, the highest ever before adjusting for inflation.

The psychologically unsatisfying reality is that the Great Recession has further bifurcated the economy. Most people still are working, yet for many it will be a long time before they get another job, if they ever do. Many companies are more efficient than ever and are sitting on mounds of cash, but their success often is overshadowed by stories of other businesses hanging on by a shoestring.

The question, then, is whether the "haves" can offset the "have-nots" to a great enough degree to keep the recovery going.

This is where the zombie bears concede nothing to the economic optimists.

The recovery is a sham, the bears say, because the global economy's dive in 2008 and early 2009 was halted by massive financial intervention by governments and central banks worldwide: unprecedented money-printing and rock-bottom interest rates.

With Europe's debt crisis flaring again, and with the Federal Reserve this month committing to spending nearly $900 billion more to buy U.S. Treasury bonds by mid-2011, it's clear that governments' previous efforts weren't enough. They've been trying to solve a debt problem by papering it over with more debt.

"The worries about things falling apart stem from the sense that we haven't really fixed anything," said John Hussman, an economics PhD who heads the $9-billion Hussman Funds in Maryland.

While he says it makes no sense for the U.S. government to impose austerity measures on the economy at this stage of the recovery — the route that Europe is taking — he still believes the Fed's policy is "reckless."

Even so, Hussman said, "I'm not expecting the economy to fall off a cliff," in part because of the corporate sector's financial strength. "Many companies' balance sheets are liquid; they can handle a lot of pain," he said.

But for the global economy overall, the debt buildup of the last 30 years remains the paramount issue. One way or another, the debt has to be resolved.

Governments and central banks want us to believe that the debt load can be worked down over time without destroying the economy and the financial system in the process. They're counting on the spending of the haves around the world to make up for the drag on the economy from the have-nots (including the hopelessly debt-ridden).

The zombie bears are certain that the worst lies ahead, and that consumers and investors should prepare accordingly — although how exactly to prepare is a matter of debate.

"We need a deleveraging, deflationary depression, and in three to five years we're going to have a much better economy," said Michael Pento, senior economist at Euro Pacific Capital in New York.

"We just have to go through hell in the meantime."

Angry Bear

First, there was Fred Schwed's Where are the Customer's Yachts?, which is still the standard bearer for why Money Managers are overpaid.

Now (via the NYT) there is The Investment Answer (preface here [PDF]).

The Prologue opens more Matt Taibbi than Jason Zweig:

Wall Street brokers and active money managers use your relative lack of investment expertise to their benefit...not yours

Of course, they have a method That Will Work to solve this, which looks suspicuously like what those Active Money Managers say they do. And what you would think Economic Theory would tell you to do, which may be why they have the endorsement of Eugene ("the markets are too efficient") Fama among many others.

Perhaps it's time for economists to model why economic theory doesn't work?

The last time people realized their money managers were taking them for a ride, the market basically sat still for a generation. Whether this dying text is a leading indicator is left as an exercise, though not an academic one.

Mish's Global Economic Trend Analysis

Please consider PBOC Researcher Calls on U.S. to Sell Gold, People’s Daily Says The U.S. should cut its government spending and sell some gold reserves to balance its budget and fund its recovery, the People’s Daily overseas edition reported, citing Xia Bin, an adviser to the People’s Bank of China.

The U.S. has to resolve its “twin deficits” in the government budget and the current account, Xia was quoted as saying. Three ways that may help the U.S. achieve that target include reducing military expenses, selling part of its gold reserves and relaxing some export limits on technology, he said.

“The U.S. has more than 8,000 tons of gold reserves; why can’t it sell some of it since the country wants to raise funds for economic recovery but doesn’t want to add more burden to the fiscal deficit,” Xia told the newspaper.

Here's the punch line, "the PBOC researcher didn’t mention whether China would be willing to purchase any gold from the U.S." Ya think not?

November 7, 2010

Andy Xie arguing that QE2's only impact is that it shows how the U.S. is checkmated by countries unwilling to let their currencies appreciate.

It seems that nobody wants to appreciate. Most major economies will do something to keep their currencies down. That is checkmate for the US. Without the devaluation benefit on rising exports, QE just leads to inflation, first through rising oil prices. The American people are suffering from declining housing prices and high unemployment. If the gasoline price doubles, the country may not be stable. How would the elite react? Probably more of the same.

The world is heading towards high inflation and political instability. It's only a matter of time before there is another global crisis. The first sign would be a collapsing treasury market. The Fed is controlling the yield curve through its QE program. But, it is irrational for other investors to play this game. The only reason to stay in is that the Fed won't let the market fall. But, the underlying value is evaporating with rising money supply and the inflationary consequences. When all the investors realize this, they will run for the exits and the Fed won't be able to stop the stampede. If it prints enough money to take over the whole market, the people with freshly minted dollars would surely want to convert their money into other assets. The dollar would collapse too.

The world seems on course for another crisis in 2012. The same people who caused the last crisis are still in charge. They'll get us into another. Iceland is sending its former prime minister to court for causing the banking crisis. A worse fate awaits the people who are causing the next crisis.

More here.

Mish's Global Economic Trend Analysis

Bloomberg reports Microsoft Record-Low Coupon Punishes Investors.I would suggest the opposite of Goldman's forecast. I expect low-quality junk to get hit, perhaps seriously hit as the recovery stalls.Spreads in 2011 are likely to tighten most on debt from high-quality financials, low-quality non-financials and bonds maturing between five and seven years, Goldman strategists Charles Himmelberg, Alberto Gallo, Lotfi Karoui and Annie Chu wrote in a Nov. 19 report.

“Our rates team expects long-dated Treasuries to move higher on economic recovery, both in the U.S. and globally, and the normalization of U.S. inflation expectations, with yields on the 10-year rising to 3.3 percent by the end of 2011,” the strategists wrote. “We expect total returns on tight-spread credit to underperform accordingly, with high-quality names suffering the most.”

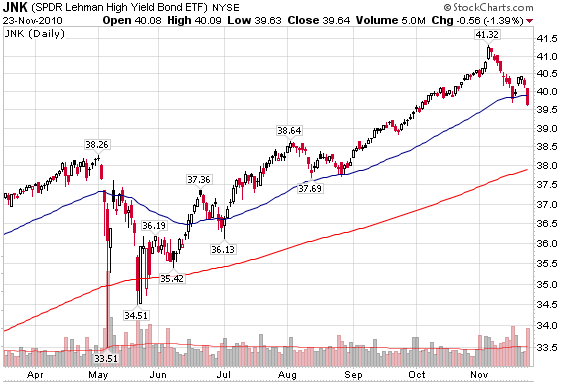

JNK - Lehman High Yield Bond ETF

click on chart for sharper imageThe JNK ETF is a good proxy for low-quality "junk".

Nearly everyone is underestimating the likelihood of a significant selloff in corporate bonds, especially junk, not because of a strengthening economy, but because of a weakening economy and rising default risk.

Corporate bonds in general, and junk bonds in particular have been a one-way bet since mid-May. If the corporate bond market cracks, it will take the equities market down with it in a serious way.

Comments

CreditCrumbs:

It looks like we are following the path of Japan, but appearance can be deceiving!

The reason for their persistent deflation is because they did QE but after a few years their QE was unwound. We will not have that luxury. We do not have sufficient domestic savers to ever unwind QE. QE2 will lead to QE3, then to dollar crash, unless China revalued their RMB before we reach that point. Our terminal path is not persistent deflation, but persistent inflation.

black swan:

Mish says:

"Japan is now in debt to the tune of 200%+ of GDP. It build bridges to nowhere hoping to cure deflation. It is madness. All Japan has to show for massive fiscal stimulus is debt."

Maybe Japan has a little more to show for all that stimulus. Guess it all depends on what a country decides to spend its money on. Consider:

United States' unemployment rate stands at 9.6 percent (real rate closer to 20 percent) Japan's unemployment rate fell to 5.0 percent in September from 5.1 percent in August

The US homicide rate is more than 11 times higher than Japan's

The US incarceration rate is 14 times higher than Japan's

Number of illegal immigrants in the US: 11 million plus Number of illegal immigrants in Japan: effectively zero

Nope, Japan and the US ain't twins separated at birth. More

Show user's profile Mark comment as offensive URL of this comment

Get a widget like this Like this comment? [yes] [no] (Score: 1 by 1 vote)Community assigned karma score: 0 by 0 replydeleteeditmoderate

Lisajean says:Today, 2:30:06 PM“Blackswan, but as Prechter often points out, we have much more bad credit out there than Japan ever had. The credit implosion will be much much worse for us.

Bill Lumbergh:

Bernanke is so far down the road of papering over problems that to do anything else now would be an admission that his cure is in fact the disease. As such I would expect more of the same until something completely goes haywire rendering his actions useless. Of course by the time this happens trying to take personal preventative measures may be a bit late.

RoRoTrader:

Nice lead into the surreptitious trade war underway.

And, no fucking around here.......the Chinese are wanting to be paid for the UST iou one way or another. Quick calculation says Bejing can rally public opinion

What is worse than admitting to a creditor that I cannot pay the bill when due? Bernanke et al appear to be the experts at ripoff, of whoever, Chines or American for that matter..

Interesting.......what are rare earth minerals worth as a puzzle piece in the context of the big picture?

ddtuttle

The chinese spent decades in the international dog house. During that time they developed a very truculent approach to perceived threats and slights; they pushed their hand to the limit. And nobody really cared. Thiry years on the Chinese are becoming very powerful, yet still take a kind loud, sledgehammer approach to the inevitable shoving that goes on between super powers. They have not always wielded their new power gracefully.

The USA is still the most powerful country in the world, and should not cower before anybody, no matter how many tons of rare earths they have. The chinese are playing chicken with the country that beat the Japanese and the Germans on opposite sides of the world at the same time. They may think we've gone soft in in the head and in resolve. I think they are due for a lesson in hard ball.

The US still controls the reserve currency of the world, the dollar. This is a double edged sword, and cuts both ways. The global economy runs on dollars, and to maintain this status we must flood the internation markets with dollars to keep adequate supplies of liquidity. The only way you can do this is to be a net debtor. This is seriously inflationary, although it does "export" that inflation to the people it is benefitting. One way to look at it is that there is a dollar funding nearly every international transaction. That's a lot of dollars, most of which the US doesn't need for itself.

Regardless of how you feel about globalization, we have been provider of the credit created money that made it happen. The chinese are a major beneficiary of all that liquidity, which operated like a loan that allowed developing economies (like China's) to get on their feet.

Of course, this is unsustainable; the USA cannot fund the liquidity of the world forever. The reserve status of the dollar must give way so we don't print ourselves into oblivion, which is obviously happening right now.

However, The Yuan is NOT ready to replace the dollar. The idea that a currency that doesn't even float could become the new reserve is ridiculous. They can only consume about 1/20th of what they produce, so they need to export or die. The creator of the reserve currency must, by definition, be a net debtor, and the bigger the better. Once the Chinese understand that (they probably already do), they wouldn't want the Yuan anywhere near reserve status, they could not withstand the inflation, exported or not. The Chinese have taken a very selfish and small minded posture, keeping as much profit for themselves as possible. They have not "grown up" and become a mature responsible members of the international financial world.

Don't get me wrong I have tremendous respect and admiration for what the Chinese have accomplished in an incredibly short period, but they seem reluctant to go from small mercantilist economy to one of the benevolent patriarchs in the global power play. The wealth a country receives from the world may be theirs, but they didn't create it.

I remember when the Japanese were so wealthy, they were going to buy the world. Rent Black Rain and Rising Sun again if you've forgotten. To me China looks like a replay of Japan's ascendency in the 1970s and 1980s. They have the same aging demographic that Japan had, they made a fortune manufacturing everything. The Japanese made better cars than we could, and eventually put GM out of business. We survived.

And our reaction to China is equally paranoid and xenophobic as it was to Japan. China is blowing a world class construction and real estate bubble, that must collapse on them just like ours did on us, and Japan's did on them. Their mistakes are not the same as ours, we sold houses to people who couldn't afford them, then sold the toxic mortgage several times over. The chinese build cities no one lives in. They over build to satisfy perverse political incentives, we over built to satisfy perverse financial incentives. The third act ends the same way.

Now, I'm no fan of The Bernank, but the other side of this argument gets way too much attention. The situation is, as always, vastly more complex. Already Bernanke's strategy is causing serious inflation in China. And he's not done. As the dollar goes down, the inflationary effect is felt much more strongly in China than here. He's deliberately pushing them to the brink, to force them to behave responsibly, like super power they have become.

If the world abandons the dollar in a panic driven flight to hard assets and commodities. it will create hyper-inflation in every currency. Nobody benefits from that. The Chinese have no incentive to make their 2.5 Trillion of dollar reserves worthless. Consider that the Chinese are scurrying around the global trying to lock up future oil production. We have been doing that for 70 years. The Saudis have been trading oil futures (to us) for gold futures for decades. We have ALREADY locked up huge amounts of future oil production. The Chinese are just trying to catch up.

The US is making some really serious mistakes, but we always have. We blunder our way to success, mostly because we just keep trying. My point here is that this is becoming a game of very hard ball, and we still hold plenty of cards. That story, right or wrong, doesn't get told.

WSJ.com

Federal Reserve Chairman Ben Bernanke's $600 billion quantitative easing program has been roundly criticized in this country and around the world. So why is he doing it? Does he know something the rest of us don't?

Mr. Bernanke claimed earlier this month in a Washington Post op-ed that "higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending." But, as Mr. Bernanke must know, the Japanese have been trying to influence their stock market for 20 years, with little effect on their economy.

For a long time, including during the Bush administration, the Fed has been manipulating markets to disguise economic facts that the world must face and adapt to in order to get moving again

I notice a persistent cognitive dissonance in policy circles.

On the one hand, it's taken as an axiom in these circles that the hysterical behavior that led to this situation was, at least in part, the result of normal psychology: in boom times, people join in ever less rational behavior, making ever riskier "bets," as they perceive others profiting from ever riskier bets. According to this widely accepted model, this behavior continues until a "correction" arrives. At that time, the least prudent pay the piper for their excess as the economy corrects.

On the other hand, when the correction does present itself, the policy makers try to spackle over it: in this case, via monetary policy. It's one thing to devalue the dollar a bit to compensate for a relatively aberrant and short-term economic problem. It's another to try to fix fundamental and deep economic problems with these tools. It simply won't work. Devaluing assets in the books of irresponsible banks will do nothing to correct the behaviors that contributed to the problem in the first place. Nothing in the Fed's history, Wall Street's history or the banks' history indicates innate prudence or prescience. Letting them, and those who used them, off or softening their landing will only encourage more of the same behavior when the economy "reheats." The next time, the behavior will only be that much worse.

To put it another way, if a house (or office building) is only worth $1 in the open market, the owner will only get $1 for it. Devaluing the dollar so that it will sell for $2 fixes nothing.

Very misleading to say the Dow is down 254 points since the Fed's announcement. Andy Kessler of all people knows full well the massive move in equities throughout Sept. and Oct. was due to the markets discounting QE2 after Bernanke's Jackson Hole speech in August. Markets did not wait for the official announcement.

"Mr. Bernanke must believe that real estate (residential and commercial) would quickly drop, endangering banks."

In other words, he's looking to create inflation in housing, rather than letting the market find an equilibrium in housing prices and start to clear inventory.

Propping up prices, whether it be by manipulating interest rates, skewing lending standards, injecting more "liquidity," or shifting risk from lenders to taxpayers is how bubbles are created and propagated. At some point, the market WILL win out over the best-laid schemes of government types. So, why delay and worsen the inevitable?

It's classic 'not on my watch' syndrome. He is so busy trying to avoid the eventual market floor 'on his watch' that he is missing an opportunity to actually fix the problem 'on his watch'.

Agreed that real estate is still headed down, and that the Fed is now in a continual bailout mode to save the banks. The huge displacement caused by ZIRP and QE1&2 is stripping wealth from traditional lenders including pension funds, insurance companies that offer annuities, endowments, and individual savers. This will end very badly. Someday we will learn that we cannot fool the market, and eliminate correction pain by government spending and central bank interest rate and credit manipulation.

That QE2 is intended as a bank bailout was obvious the day of the announcement. The Fed wants a "bear steepening" of the yield curve, which helps promote bank 'profitability' and flushes money out of the long bond and into equities. This has an inflationary effect - we will all pay for bank 'profitability' (be dam*ned).

The question remains whether the Fed will be able to maintain a steep curve, or if the vigilantes will orchestrate a "bear flattening." The bond market is fragile and there are many opptys for shorts - the muni bond market is just the latest target.

The point remains: when will they all learn that the deleveraging process needs to run the full course? Cheap tools won't solve the problem, they will only extend it and make it worse. Seems as if they were never taught that failure can lead to success......

What's missing in this discussion is the problem of our national debt. We will incur debt in 2011 at about a rate of $110 billion / month, coincidentally about the same as the QE2 program. Demand for US debt has softened substantially and would soften further if we attempted to push that level of debt into the private sector. I'm only guessing, but I estimate that 10 year Tbill rates would easily reach the high single digits, at least 500 basis points higher than today.

The results on the US economy would be devastating. First, it would increase the annual deficit even more. Much or our debt is now at the short end of the yield curve, so it would not take long before we had to re-finance most of our existing debt at these new higher rates -- $13trillion times 500 basis points would ultiimately add over $600 billion per year to the deficit. That added amount would force interest rates up even more, creating a "death spiral".

Second, any variable mortgages (and other loans) that haven't yet gone delinquent would quickly do so. "Look dear, we got a letter from the bank and starting next month the interest rate on our mortgage is 15%". Not a pretty picture.

Third is the impact on bank balance sheets / reserves, where a steep rise in interest rates would plummet the value of all their assets, not just MBSs. The stock market would also suffer, as a steep rise in Tbill rates would devastate the value of an S&P500 paying about 2.5% dividends.

I'm no fan of Bernanke, but I've said before and still believe that he had no choice but QE2, and that QE3 must follow later this year.

The solution is to drastically cut government spending, quickly reducing the deficit (raising taxes, on the "rich" or anyone else, will have a much smaller impact on the deficit than the current static scoring models predict; much of the higher rates will be offset by lower growth). Bernanke's great crime as head of the Fed, first under Bush and now under Obama, was to put up no fight to the massive growth in govt spending. The Fed could have used its illusion of independence to take a principled stand; I don't believe that concept is in Bernanke's dictionary.

You can see the 10 year heading to high single digits? If rates back up 500 bps like you say then you're right, housing plummets, balance sheets implode, stock markets tumble. Where will that money that money go? What happened the last time housing and the markets turned south? You seem to be only fixated on the supply side of the equation.

The current political trend is towards balanced budgets not increased deficits. Extending unemployment benefits did not even pass this week. That limits the supply side of the equation. Our deficit is not only the result of the money the government spent and is spending but also the gross tax revenue shortfalls at every level.

I see many people on these blogs comment that rates have to go up but I would argue that rates will continue to fall. Total credit is contracting and the government has already borrowed and spent most of it's "dry powder." More government borrowing and spending isn't out of the question however, if rates back up like you say there will be plenty of money rushing into the Treasury market to fund it. No matter what posturing your read about our fiscal situation, we are still looked at as the best of the worst when there is a flight to safety.

Last I looked, average maturities for US debt was 6-7 years. That means that with no new deficits, we have to sell over $2 trillion of debt every year. We are already seeing in the Muni bond markets how a glut of supply is driving prices down and yields up. If we add the $1.3 trillion dollar deficit to the $2 trillion of "roll-over", that will have to have a signifantly adverse effect on price. I'm estimating it would drive 10-year notes up to 6 - 8%, but that is based on minimal data analysis. It is consistent with 10-year rates through most of the 1990s; my memory is that 10 year rates didn't drop below 6% until around 1998 or 1999, and then went back over 6% in 2000/2001.

You are right in pointing out the we are "the best of the worst". But we are also the biggest of the worst. The world can absorb high Greek and Irish debt because their GDPs are so small. If the US debt hits a tipping point, there can be no IMF or Eurozone bailout. Being the best of the worst may buy us some time, but that is only valuable if we use it wisely.

I disagree with your assessment that the "current political trend is toward balanced budgets". The special commission identified $300-400 billion of deficit reduction per year, and most of that isn't realized until 5+ years out. Our current deficit is $1.3 trillion. CBO assessment of the deficit for the next 10 years assume things like full expiration of the Bush tax cuts, and that ObamaCare is deficit neutral. I suspect that a more reasonable assessment of deficits over the next 10 years would be at least double the current CBO estimates.

Until we are willing to confront the cost of entitlements (SS, Medicare, govt pensions, etc. at all levels of government are equal to almost 25% of GDP), which make up about 60% of total govt spending, then I can give no credence to the various committees and promises.

You are also right that growth can be a big part of closing the budget deficit, but growth requires investment -- into capital markets through cuts in tax rates and/or through direct govt investment in very specific initiatives (history says the former has greater short-term impact). I do not see a government willing to tackle either of those things.

Its an interesting discussion and a roundabout way of reaching the conclusion that the Fed has very limited monetary options right now, and that unless we fix our fiscal problems all the Fed can hope to do is buy a little time.

Frank, We are on the same page with the effectiveness of monetary policy and the the implications of Fiscal policy. There is no question that the government has a role to fill here with the private sector contracting. To clarify; the government should be injecting money into the economy but in a way that the country as a whole gets a long term return for it. This idea that they should just start giving it away and throwing it down a black hole is crazy. It is difficult to pay back money from malinvestment regardless if it is government or private investment. The difference is who is stuck with the bill.

I don't question your budget figures or your data, just the out come of higher rates. It seems to me our current system has a built in check for higher rates. Higher rates create the problems we discussed earlier. When that happens money rushes out of risky assets and into safe assets. (The US for now)

Until we get true price discovery of all assets resulting from the biggest credit boom in history, I can't see where the demand for more credit comes from at these higher rates you talk about.

Calculated Risk

From Bond Girl: Some thoughts on the muni marketI have been somewhat hesitant to write about the recent sharp correction in the muni market, mainly because I do not like wasting my time.I think it is important to understand that these supply issues are what is driving the muni market - not an imminent default.

...

My opinion, for whatever it is worth to you, is that there are a handful of factors – mostly unrelated to the relative creditworthiness of muni issuers – that have provoked this correction. These factors are related, and they will likely contribute to volatility going into next year.The first, obviously, is a supply glut. The pending expiration of the Build America Bond (BAB) program has pulled supply forward, and this is going to seesaw over the next several weeks. Since the BAB program was initiated, most issuers have structured their new issues with the sense that they will go to either the tax-exempt or taxable market, whichever is more advantageous at the time. It has been almost completely a supply management game since the market for these bonds was established and munis became truly bifurcated.

...

By allowing muni issuers to sell taxable bonds, the BAB program opened the market up to investors like pensions and foreign investors, who otherwise would not benefit from a tax exemption on the interest income on the bonds and would find tax-exempt yields unappetizing. This program has relieved the supply pressure on the market for essentially two years now, keeping interest rates low.

What is going on now is that muni issuers are scrambling to get deals done to take advantage of the program before it expires, and this is pulling the number of new issues that would ordinarily be coming to market forward. So the looming expiration of the BAB program is creating the very conditions it was created to alleviate. Issuers are very conscious of this fact, and that is why a large number of deals are getting pulled. As more issues get pulled and supply is reduced, there will be some relief on rates, which I think is what happened today. But you can expect that muni issuers will be dancing around this until the program expires at the end of the year, so there will likely be significant volatility. There is also considerable uncertainty as to how supply issues will play out in the first quarter of 2011.Byzantine_Ruins:

TagsCalculatedRisk wrote:

I'm not saying there won't be a default, but the recent sharp decline happened for clear reasons.

However, in the longer scope, there's clearly going to be yield pressures. Even if they continue to permit taxable issues and the issuers can arb the bifurcated market, it seems like deteriorating creditworthiness -- especially given the parlous finances of the muni insurers -- is going to lead to muni bond market exposure to yield spikes. .

Rob Dawg wrote:

Very well said. As with any economic segment it is very important to avoid confirmation bias. Looking for trend in noisy data is a subtle business.

Bond Girl reminds us of many of the factors in the bond universe that have little to do with what we think of as risk default premia.

rich

I think Meredith Whitney has the answer pegged better than Bond Girl.

Supply/demand is a much smaller factor driving munis down than is the end of multiple federal support systems for transferring money form federal govt. to states and localities. The election results triggered the muni bond selloff. Stimulus support to states/localities will end next summer, according to Meredith.Byzantine_Ruins:

Outsider wrote:

It is a reflection of how one-sided today’s class war has become that Warren Buffet has quipped that “his” side is winning without a real fight being waged.

That because the blues will stand by their man regardless of his merits (q.v. red team defense of Bush II) while there are endless guys with six and seven figure net worths stupid enough to think when someone shouts "class warfare" they're on the "rich" side. Single-Digit Millionaires are just another marketing demo.

zero hedge

Making The Last Use Of Reserve Currency Status

I suspect many in the mainstream academia haven't realized what QE2 is. It is the last use of the dollar's reserve currency status, intended or otherwise.

In a fiat currency system, inflation should be the only risk, because fighting deflation should be trivial -- just print money. This is a fundamental advantage of a fiat system over the old gold standard. Unfortunately for the US, the dollar's reserve status means the geopolitical border is not the dam holding the water as in other countries. As Fed pours in more water, it leaks right out to lowlands (good investment destinations) all over the world. Given the current economic prospects in the world, the result is that QE2 cannot stoke inflation in the US, but causes very unwelcome interference in exactly the other places in the world where inflation is a big concern.

It's small wonder all the growth EM economies are engaging in the low-grade currency war of capital control. To them, this is a defensive war for survival against the invading army of dollars. If the low-grade war proves insufficient, they would escalate the defensive posture. They have to.

Another consequence, intended or not, of QE2 + reserve status is that all growth economies are under tremendous pressure of currency appreciation. Some may be able to resist it and muddle through until an easier day; others will have to cave in, therefore caught in the catch 22 of either raging inflation or shrinking economy, or both. And, of all the growth economies, China arguably has the most capacity and strongest political will to resist appreciation. In such a scenario, if the intended target of Fed's fury is China, as hinted not so subtly by Bernanke, "collateral damage" would once again be the main theme, as has been in all recent offensives launched by the US.

In summary, Fed's dogged efforts in stoking inflation have caused and will continue increasing the risk of bringing all growth EM economies to a halt, significantly increasing policy risks in the rest of the world as each country tries desperately to deal with the capital tsunami, and all the while with huge doubt in whether it could reach its domestic goal of stimulating employment and housing. In other words, Fed is screwing the world for a slim chance of helping the US economy.

This is emphatically NOT a moral criticism. But it does represent a significant abandonment of the responsibilities on Fed's part as the issuer of world reserve currency.

Let's go back a little in history. Right on the heels of WWII victory, in 1944 US dictated Bretton Woods that established the dollar as a proxy for gold in the free world. The "proxy" part was only convenience, of course, as to be expected and proven by Nixon in 1971. The arrangement made sense: the US would provide security blanket, and the rest of free world would pay for it by accepting and holding the green paper printed by the US. It's the same idea as gangs collecting protection fee in NY, no cynicism intended.

Fast forward to Berlin Wall collapse. Now the fundamental premises of the dollar's reserve status were gone. Europeans quickly realized this change and created the Euro; why should they continue paying for protection when there's nothing to protect against? The US has made numerous fantastic efforts in creating threats (by "creating" I don't necessarily mean create; often times you just have to doze off for a second and the enemy will help you out): perpetual terrorism, WMD in Iraq, perpetual war in Iraq and Afghanistan/Pakistan, Iran, North Korea, China, even Somali pirates (now it gets really pathetic). But none of them could ever live up to the high expectations set by USSR.

After 10+ years of trying, it's become clear that this is futile. Nothing works; none of those idiots could do it. But with the reserve currency status comes its responsibilities. Win-win is BS-BS; there's no free lunch after all. The time has come to end Bretton Woods II.

Now Zoelick's surprise proposal of a new gold standard makes perfect sense.

With QE2 the Fed is saying: Ah fuck it, you don't like USD as the reserve currency? Well guess what? We don't like it, either. So let's drop it and from now on it's every man on his own. Good luck.

Good luck everybody. We all need it.Beatscape

One of the prerequisites of a reserve currency is that the float is sufficiently large to handle cross border transactions of any size. So it is a bit ironic that QE2 actually helps the USD maintain its status as THE global reserve currency. One of the messages from the Bernank is that resistance is futile--we will overwhelm the world with a tsunami of dollars. Eventually, this could backfire. But for now it further cements the USD as the world's reserve currency.

rwe2late:

I disagree with Bo Peng's claim that the US PTB do not like the dollar reserve status. "We don't like it, either."

The reserve or petrodollar status underpins the whole global empire.

Foreigners help pay for their own US military occupation, and even for the economic war against them. The petrodollar requirement for oil (and other commodity) purchases enables a global extortion racket, and partly explains the US insistence on Mideast control and dominance. For the cost of fiat dollars, the US theoretically "owns" the goods and resources of the world. The bizarro fiat economics compels other nations to push up the demand for dollars even as the US prints more of them.

No, although the US PTB may want to default on dollar-denominated debts, I do not think US leaders want to lose control of their global financial racket, any more than when they defaulted on their gold denominated debts.

Look to NATO and the IMF for the possible future.

MachoMan:

Just another argument from induction. If we've learned anything over the last two+ years, it should have been to throw out the history books and rework the models. This thesis presumes that demand for dollars exists in perpetuity, foreigners demand to be enslaved, and the ability to pay for our industrial military complex lasts long enough to make a transition to a "world" currency (even though this status is already held by the dollar and the U.S. is presently in the driver's seat, but would have to cede some degree of control to make the transition). In short, the fuel runs out before we get to escape velocity.

In the end, isolationism will prevail and, as credit contracts, so does trade interaction. The camel is in the tent wrecking shit already.

by Oh regional Indian:

++ Ironically funny, Macho.

And that is quite an interesting train of thought, military might lasting just long enough for One world currency to be introduced, then a ton of breathing space for these guys to re-group.

It would explain their willingness to leave so many soldiers in far away bases at serious risk of supply chain disruption. Maybe they'll just be cut adrift, without the codes of course. Or become self-sufficient subsidiaries of the United Nations Corporation..

ORI

http://aadivaahan.wordpress.com

B9K9:

There is no thesis, other than to utilize the banking system as a means of controlling power. All else are simply palliatives used to soothe the global herd. Strip away the rhetoric, and what we have is naked aggression & imperial conquest. Who in the US of A wants to be viewed no differently than Nazi Germany & Imperial Japan?

MachoMan:

Yup. The good thing, for us, is that implementation, monitoring, and management of the banking system is too dynamic for humans, despite our egos telling us with such power we inherently have the intelligence to control it. I say good thing, but obviously it could end very, very badly (strong likelihood of massive social upheaval, political unrest, even the changing of borders and allies)...

but what I mean is that eventually we (morts) grow exhausted on their treadmill, pass out, hit our heads on the ground, and wake up off the treadmill. Of course, the entirety of our recovery is spent trying to get us back on the treadmill, but luckily we naturally have a skeptical and weary period before eventually capitulating. In other words, just because we are apathetic to change is not necessarily dispositive of whether change will occur (inevitability upon contraction). Hopefully we are skeptical of the sales pitch for a very long time following our bump on the head.

Barrons.com

The manager of the third-largest mutual fund focusing on junk bonds is buying stocks while cutting back in his portfolio’s primary area.

“I don’t see the value in the high-yield market,” said Mark Notkin, manager of the Fidelity Capital & Income Fund (FAGIX).

In an interview with Bloomberg, he added that stocks seem a better investment and that the rally in junk bonds is over.

Other bond managers and analysts agreed with Notkin.

His fund has the third-most assets, according to the report. It only trails American Funds High-Income Fund (AHITX) and the Vanguard High-Yield Corporate Fund (VWEHX).

But in the past five years, Notkin’s returns have beaten all other rivals, according to the report.

It seemed to be the only decision that was not made in a panic. It adhered to the rules of capitalism — when your company is insolvent, it goes into reorganization or dissolution. The brutal, Darwinian rules of the market and of bankruptcy applied — not the influence of lobbyists, or special favors from Senators. The Treasury Secretary’s former gig was not running an auto company, he ran a Wall Street bank — so there could be no special favors expected to come from that quarter either.

Instead, Uncle Sam’s involvement was to provide Debtor-in-Possession financing. The bankruptcy plan was obvious: Wipe out shareholders, give bond holders a haircut, fire management, pare the company down to a sustainable size without sentiment.

This was what was done. A turnaround plan was created and executed. If the company met its milestones, the firm would be taken public, which would allow the government to significantly reduce its stake and exposure to GM. The Fed also helped, keeping financing rates at ultra low levels.

The long term stock sale plan would lead to the taxpayers being made nearly whole. All told, it was a wild success. Malcolm Gladwell argued that Rick Waggoner should get more credit and Steve Rattner less, for GM’s effective turnaround; many of the new models that are now doing so well were first created and planned for under Waggoner’s tenure 5 years ago.

So what is arguably the most successful bailout of the 2007-2010 era was in fact a non-bailout: It was a bankruptcy reorganization that eliminated the most toxic aspects of a century old rust bucket of a company. The new firm has clean books, is well capitalized, is without crushing debt, has a less onerous labor contract, pension and health care obligations. Its hard not to see how this was anything but a ginormous winner for all involved.

Which brings me to the Banks.

Currently, the United States has a weakened financial sector. Many of the largest Banks are technically insolvent, but thanks to an accounting rule change, are not required to admit this simple mathematical fact. They are carrying an enormous amount of bad loans on their books. They are sitting on several million REOs — bank owned foreclosures for which there is essentially no market. This shadow inventory of houses amounts to years worth of sales, not mentioning the depressing effect the excess supply will have on prices.

The reckless lending of the 2000s was merely the tip of the iceberg. From start to finish, the engaged in all manners of irresponsible behavior. When a company’s actions are so reckless it compromises the firm’s ability to survive, why would we expect it to have performed any of its other duties competently? They didn’t, which is why we have learned about how poorly the banks not only made these loans, but also administered, securitized, serviced, and foreclosed on them. The entire process was reckless, it was done on the cheap, riddled with errors, fraud and felonious behavior.

It has become a national embarrassment.

The bank bailout plan was ill conceived and poorly executed. Trillions were thrown at them before Uncle Sam had any idea as to how much debt was actually on the books. What were once considered decent holdings were eventually revealed to be highly toxic assets.

Recapitalizing the banks is a huge priority. But after the first round of trillions were given away to the banks, the public was disgusted. The politicians lost their appetite for overt bailouts. But the banks were still under-capitalized, their balance sheets were still laden with junk. A direct transfer of taxpayer monies was out of the question.

An easy backdoor was found: Arbitrage the Fed and Treasury. Zero interest rates and QE allowed giant Wall Street banks to borrow at no cost from the Fed, and then turn around and lend this same zero cost money back to the Treasury at 3% or so. Do this for another 10 years or so, and the banks would be recapitalized. By then, maybe there might even be a market for all those REOs. Sure, that would mire the nation in a decade long Japanese-like slump. Hey, at least the bonuses would be paid on time.

The motto of the bank bailouts: To hell with the banking system, save the banks!

The results should not be surprising. The banks remain in a weakened condition, perilously at risk for additional problems in RE. Despite the massive liquidity, Credit still remains tight. If financing is the fuel that drives the economy, the US is running on fumes.

Wall Street has returned to business as usual. The Street is nothing if not savvy. Just as a shark detects blood in the water, the Street can smell weakness and exploit it like no other industry. Once they figured how to play chicken — mutual assured destruction – with the entire global economy, there would be no restraining them.

~~~

Compare the differences between the banks and GM/Chrysler, and will see the full folly of how we rescued the financial sector.

Instead of letting insolvent banks fail, we turned over the keys to the castle. We could have fired the incompetent management that caused the problems — but most of these execs are still in the same highly placed positions in their firms. In terms of senior personnel, the industry is literally unchanged.

- Bad debt? Still on the books.

- Sufficient capital? Many years away.

- Business model? The same highly leveraged reckless strategy that got them into trouble in the first place

- Regulatory Oversight? A modest improvement which the newly elected, bought and paid for Congress, seems hellbent on overturning.

If you want to understand why we should never have bailed out the banks, just look at the differences between the Auto and Banking industries. One is healthy, with a likely cost of near zero. The other remains a debacle, whose costs are incalculable are likely to be an economic drag for years if not decades.

Too bad the minds behind the bank bailouts did not have the foresight to appreciate the full advantages of prepackaged bankruptcy for the sector . . .

naked capitalism

November 18, 2010

Koshem bos: