This page is written by a non-specialist mainly for his own consumption.

Like in Soviet Union were people were glued to BBC and Voice of America

but generally distrusted any and all information from official media, few

401K investors trust now CNBC, WSJ or other official media channels. Foreign

source like Financial Times, Telegraph, etc and domestic financial blogs

are better, although far from perfect. Still it's hard for a regular 401K

investor to understand what's happening because CNBC divas, corrupt academics/politicians/regulators

(aka financial industry shills) each day are shouting that they knew what

was going on.

The author is a computer specialist, not an economist so his views of

economic events are based on information provided by the Internet. The main

reporting criteria are event that might affect 401k investments and as such

be taken into account in investment decisions. You cannot do good reporting

of complex events without some framework and if you do not adopt one explicitly

you probably will use the worst available among actively marketed. Author

personal preferences are with

institutionalists.

This analytical

framework retains the fundamental assumption of scarcity and hence competition

from neo-classical economy as well as the related analytical tools of micro-economic

theory. It modifies is the rationality assumption and adds historicism,

the dimension of time. It also views institutions as the constraints that

structure human economic behavior. Such constraints can be formal (rules,

laws, constitutions), or informal (norms of behavior, conventions, codes

of conduct). Each also has its enforcement characteristics. Together they

define the incentive structure of societies and economies. See for example

Douglass C. North - Nobel Prize Lecture

IMHO they are the most realistic school of economic thought. In the same

venue neoclassic economists are too petty and detached form reality with

their models that demonstrate both misunderstanding of the economy and misunderstanding

of mathematics (why they cannot switch to Excel or some standard simulation

language, after all and still use liner equations of dubious relevance ?

) Voodoo economists (aka "market fundamentalists" and, especially, supply

side economists) are wrong.

Galbraith argued that industrial production was being devoted to satisfying

trivial consumer needs, in part to maintain employment, and that the United

States should shift resources to improve schools, the infrastructure, recreational

resources, and social services. The key idea here is to provide a better

quality of life instead of an ever greater quantity of imported goods and

wasting huge amount of resources. The term has lost its original ironic

meaning and is now used simply to indicate the USA-style prosperity with

individual autos, McDonalds, etc.

No attempt is made to stay current or post daily. The delay period for

quotes can be a week or more: with the exception of particular crisis moments

the economic situation is evolving extremely slowly anyway and daily postings

are often just a nuisance that complicates seeing the whole picture (information

overload in action :-)

This quote fully apples to 401K investors including myself. For 401K

investors attempts to benefit from the short-term moves of the market are

pretty typical (close to the top buying in case of bubble). But the same

danger exists in buying on dips without understanding the larger picture

as well as attempts to join "sucker rallies" in case of protracted downturn.

Such "impulsive" stock or bond acquisitions often end poorly (they are called

attempts "to catch falling knife" in professional jargon).

This page is written as a reminder of trends that might logically occur

in some (may be not too distant) future in a hope that understanding larger

trends can helps me to avoid attempts to catch a falling knife. I doubt

about my ability to get the return above inflation for the next three years

at least but I would like to avoid additional, unnecessary losses induced

by Bubblevision or market hype. It is also might present the economic situation

in terms more understandable to programmers and IT specialists. Actually

that's pretty sad that neoclassical economics operates with those primitive

(and obscure) linear models, models which bear no or little resemblance

to reality "in a short run" instead of using programs in some standard simulation

language. For example can't those economic professors just learn Excel and

present their hypothesis in Excel models terms ;-). It's actually pretty

funny how they try to use mathematics...

For those who have 401K plans and are concerned about them here is my

list of few things which probably take longer then many expect (this

100% derivative material, you are warned):

News collected below suggest that it makes sense for 401K investor to

be conservative and try to increase cash position those days. It's bad time

to hunt for bargains. Preservation of capital might be the highest possible

achievement in 2008 and 2009 for 401K investors who were put in

Procrustes bed of

randomly selected stock funds and few bond funds in their 401K accounts.

Especially for baby-boomers.

Speculative runs after a slump like we experienced in April, 2008 are

a dangerous thing to follow. Did Fed unlock the credit crunch at this stage?

The answer is no. Did banks solve securitization and over-leveraging problems

? The answer is: "The major banks are barely holding on to life...".

Regular banks should probably be priced for zero growth. Investment

banks are in real trouble due to off-balance accounts and can experience

negative growth as their business model has been broken. Bear Stearns is

kaput and Lehman Brothers is on the ropes...

Another "sucker rally" can follow this July, 2008 slump (it might be

late autumn "president rally" ), but please remember that cash is probably

the king now for 401K investors.

The Telegraph story that highlighted this development provided additional

detail:

Paul Kasriel, chief economist at Northern Trust, says lending by

US commercial banks contracted at an annual rate of 9.14pc in the

13 weeks to June 18, the most violent reversal since the data series

began in 1973. M2 money fell at a rate of 0.37pc...Leigh Skene

from Lombard Street Research said the lending conderve gave up being

interested in money supply in the early 1980s, when new banking

products made the data behave differently. But that hardly seemed

a reason to abandon a useful tool, at least not without trying to

understand how the new instruments affected monetary aggregates.

Instead, the Fed sets target interest rates in a not-terribly-scientific

fashion.

Note that while the Fed still published M1 (narrow money, currency

plus demand deposits) and M2 (M1 plus time deposits, savings accounts,

and non-institutional money market funds), it stopped reporting

M3 (M2 plus large time deposits, institutional money market accounts,

and short-term repos) in March 2006. However, some economists and

services provide estimates,

The Telegraph tells us today that those private calculations

of M3, like the publicly available monetary aggregates, show a sudden

contraction, a deflationary signal. From the

Telegraph:

Data compiled by Lombard Street

Research shows that the M3 ''broad money" aggregates fell by

almost $50bn (�26.8bn) in July, the biggest one-month fall since

modern records began in 1959."Monthly data

for July show that the broad money growth has almost collapsed,"

said Gabriel Stein, the group's leading monetary economist.

On a three-month basis, the M3 growth rate has fallen from

almost 19pc earlier this year to just 2.1pc (annualised) for

the period from May to July. This is below the rate of inflation,

implying a shrinkage in real terms.

The

growth in bank loans has turned negative to a halt since March.

The

growth in bank loans has turned negative to a halt since March.

"It's obviously worrying. People either can't borrow, or

don't want to borrow even if they can," said Mr Stein.

Monetarists say it is the sharpness

of the drop that is most disturbing, rather than the absolute

level. Moves of this speed are extremely rare....

Monetarists insist that shifts

in M3 are a lead indicator of asset prices moves, typically

six months or so ahead. If so, the latest collapse

points to a grim autumn for Wall Street and for the American

property market. As a rule of thumb, the data gives a one-year

advance signal on economic growth, and a two-year signal on

future inflation.

"There are always short-term blips but over the long run

M3 has repeatedly shown itself good leading indicator," said

Mr Stein...

M3 surged after the onset of the credit crunch, but this

was chiefly a distortion caused by the near total paralysis

in parts of the American commercial paper market. Borrowers

were forced to take out bank loans instead. The commercial paper

market has yet to recover

In his speech accepting the Democratic nomination in 1992, a

year in which economic conditions somewhat resembled those today,

Bill Clinton denounced his opponent as someone "caught in the grip

of a failed economic theory." Where Mr. Obama spoke cryptically

in St. Petersburg about a "reckless few" who "game the system, as

we've seen in this housing crisis" - I know what he meant, I think,

but how many voters got it? - Mr. Clinton declared that "those who

play by the rules and keep the faith have gotten the shaft, and

those who cut corners and cut deals have been rewarded." That's

the kind of hard-hitting populism that's been absent from the Obama

campaign...

Of course, Mr. Obama hasn't given his own acceptance speech yet.

Al Gore found a new populist fervor in August 2000, and surged in

the polls. A comparable surge by Mr. Obama would give him a landslide

victory...

Bruce Wilder says...

Krugman on politics is tiresome, indeed.

If he has some evidence for his thesis

that the American People long for a populist vision, he should bring

it forward; otherwise, he should shut up. He doesn't

know what would cause Obama to surge ahead in the polls, and should

not be mind-reading the whole electorate, while pretending that

he does.

Obama has managed to draw a clear contrast on income taxes, and

is fighting to keep it from being completely obscured by our incompetent

Media. Larry Bartels is pretty clear that Obama's tax plan, as simple

as it might seem to this blog's readers, is just the kind of thing

American voters get confused about, and the Media proves incapable

of reporting on accurately. Populism is not as easy a campaign theme

as Krugman imagines.

On a number of other populist themes -- the mortgage crisis,

gas taxes, off-shore drilling -- Obama

would run some serious risks of committing himself to bad policy,

if he tries to out-demagogue McCain on these issues.

Does Krugman have any ideas about how to stop "Drill Here, Drill

Now"? I didn't think so.

Obama is ahead in the polls, which indicate -- surprise! -- that

about a third of the electorate has not paid any attention, yet.

A majority of voters in 2004 elected George W. Bush; those people

and their bad judgment haven't gone away, and their numbers, though

diminished, put a floor under McCain's support, and a ceiling on

Obama's.

Clinton's economic populism may have been a lovely thing, but

not nearly as lovely in terms of his electoral chances, as Ross

Perot. Clinton never achieved an actual majority, but he didn't

need to. Obama will have to have an actual majority to beat McCain,

but he's well on track to achieve that.

NLS says...

Bruce Wilder is on point once again. Most folks still haven't

begun to pay attention and haven't even entered the stadium. (For

example, note the traction Jackass Corsi's slash and bash book grabs.)

PK is no doubt a brilliant economist, but doesn't he understand

that injecting doubt and offering hesitation only steepens the hill?

The object of the game is to beat McCain.

Cyrille says...

Bruce Wilder on Obamania is tiresome. Anyone who speaks his mind

for anything but singing the praise of Obama is immediately rebuked.

Krugman asks to state demonstrable facts, Bruce Wilder calls

that asking to out-demagogue McCain. Uh?

Obama's lead in the polls is considerably smaller than his party's,

so surely he must be doing everything perfectly. Still, Krugman

notes that Obama has not had his acceptance speech yet, and that

it could create a surge, but that won't make him less tiresome since

he's a miscreant, he does not blindly worship.

Republican economics should these days be called names that will

get you censored if children might be watching (they should have

for the past 30 years, but now the conclusions are so obvious and

immediate as to be plain to all, even those who reckon that "in

3 years time" is too far to ever happen). Failure to do so is yet

another worrying sign that Democrats have turned into Republican

light.

They have stolen, looted, lied and ruined a country the size

of a continent for the sole benefit of them and their cronies. It's

not demagogue to hold them accountable. And it's crazy to not attack

them on that when the horrible consequences of their acts are the

main thing on everyone's mind (OK, Iraq should be as well, but now

all the media reports are sterilised and very few people in the

US will get first hand experience).

Bruce Wilder says...

str: "Did a dysfunctional primary system give us two mediocre

candidates?"

The primary systems of the two parties are quite different, and

they produced contrasting candidates. Obama is a an excellent, historic

candidate, leading an extraordinarily capable campaign organization,

and an enthusiastic, motivated Party.

McCain is a pretty typical Republican Presidential candidate:

bereft of principles, callow, stupid, a serial liar, he's really

old and he heads a campaign organization staffed from top-to-bottom

with corrupt lobbyists. But, it wasn't a dysfunctional primary process

that produced McCain, anymore than it was a dysfunctional primary

process that produced Richard Nixon, Spiro Agnew, Ronald Reagan,

Dan Quayle, George W. Bush or Richard Bruce Cheney. The Republican

Party is designed to produce liars and fools and crooks, in service

to the plutocracy.

"Crushed by ballooning debts, the regeneration by the banks' own

efforts is becoming impossible ... I bet stocks will decline further

and U.S. bonds will be downgraded." said

Tetsuhisa Hayashi, chief manager of foreign-exchange trading at

Bank of Tokyo-Mitsubishi UFJ Ltd. in Tokyo

Bloomberg.com

``Crushed by ballooning debts, the regeneration by the banks'

own efforts is becoming impossible,'' said

Tetsuhisa Hayashi, chief manager of foreign-exchange trading

at Bank of Tokyo-Mitsubishi UFJ Ltd. in Tokyo, a unit of Japan's

largest lender by market value. ``I bet stocks will decline further

and U.S. bonds will be downgraded. Risk aversion among investors

will cause further yen-buying.''

The Japanese currency may rise to 100 per dollar by year- end,

Hayashi said.

For banks it's looking increasingly difficult to refinance their

debt. Outside Fed oxygen lines are cut and for those of life support

this is it.

Lehman is now expected to report a quarterly loss that analysts

peg as high as $2.6 billion. Recall that last quarter's $2.8 billion

loss was a stunner, nearly ten times the expected level, and a dramatic

departure from the convention of preparing investors for earnings

shortfalls.

Comments

- Looking increasingly difficult to get

oxygen. LEH reportedly having problems shopping its CMBS portfolio.

You think? As the cost of debt rises

(Amex 400 bps off treasury on Friday) the choke hold gets tighter.

Bloomberg goes on to wonder what institutions are worth saving?

Earnings season should be interesting.

Clearly the companies are trying to get out in

front with estimate cuts coming earlier by an inch. The upside

surprise will be credit deterioration which will be accretive

to earnings and help offset some of the charges (what a world!).

The cruches are failing, wheelbarrows

next.

Discredited "free marketers" which got the country in the current

mess try to counterattack using Wall street's "fifth column" of

PPP journalists.

Amity Shlaes, who is a nice example of the genre published apologetic

Five Ways to Wreck a Recovery - washingtonpost.com which twists

major facts about Great Depression. She does not have formal economic

education (bachelor degree in English literature from Yale)

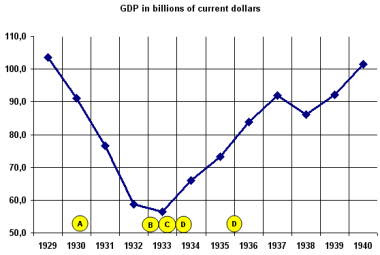

Moon of Alabama used this chart to chat about Schlaes.

GDP numbers according to the Bureau of Economic Analysis (bigger

graph)

GDP numbers according to the Bureau of Economic Analysis (bigger

graph)

A.

Smoot Hawley Tarrif Act In March 1932 the United States Senate

Committee on Banking, Housing, and Urban Affairs established hearings

to investigate the causes of the Wall Street Crash of 1929.B.

Democrats took over Congress in November 1932 and in early 1933

appointed

Ferdinand Pecora as commission counselor. Pecora found many

malpractices on Wall Street and his investigation led to the creation

of the Securities and Exchange Commission. We can put these events

at point B of the GDP chart

C. Hoover's tax decrease in 1929/30 was followed by four years

of decreasing GDP. His "misstep" tax increase was enacted in 1932

and took effect only in 1933, point C in our graph. From there on

GDP went up.

D.

New Deal beginnings.

Shlaes, according to her Wikipedia entry "has no formal economic

training." That certainly shows. She also seems to have zero training

in history as she is unable to organize the sequence of events in

a coherent way. Events and policies that obviously led to increases

in GDP are attributed as having deepened the depression.

(reformatted by rdan for a quick take....the original is more

detailed and much longer. I personally would not use wikipedia as

an academic source, but liberties are taken and the articles linked

looked reasonably accurate))

Battered US financial groups

will have to refinance billions of dollars in maturing debt

over coming months, a move likely to push banks' funding costs higher

and curb their profitability, say bankers and analysts. The banks'

push to raise capital to offset mounting credit-related losses is

forcing them to pay higher interest rates to entice investors, which

is likely to put pressure on earnings and could lead to higher lending

rates. Last week, groups including Citigroup, JPMorgan and AIG borrowed

almost $20bn in new long-term debt, paying some of the highest rates

ever in order to lock in funding. The wave of refinancing is set

to continue for several months as billions of dollars in bank debt

come due.

This entry was posted by Gwen Robinson

on Monday, August 18th, 2008 at 5:28 and is filed under

Capital markets. You can follow any responses to this entry

through the

RSS 2.0 feed. You can leave a response,

or

trackback from your own site.

Middle-class and lower definitely lost a lot of buying power during

the last two years. And with 3% CD and 5% inflation they are losing

their savings in all accounts: taxable, Roth and 401K.

The Bureau

of Labor Statistics reported yesterday that its primary consumer

price index CPI-U rose 5.6% over the last year. That's the highest

inflation rate in 17 years, the newspapers all

call to our attention. Just how concerned should we be about

these numbers?

Comments

Posted by:

sonia at August

15, 2008 06:35 PM

How shall we define stagflation?

I suggest whenever unemployment is above 5% and when inflation

is above 5% at the same time.

That's June and July 2008. Houston we have stagflation.

Posted by:

One Salient Oversight at August 15, 2008 08:34 PM

Those expecting diminishing inflation,

please contemplate CD rates of 3% (on which the holder must pay

income tax) when the reported CPI is 5.6%. What person

would lend his savings in such a money-losing proposition? Is this

the result of a free market or of a central bank lending out money

that has never been saved but created out of thin air? MZM & M2

are growing a lot faster than GDP & have been for some time.The

central banks of China, Russia, India, Saudi Arabia, et al are behaving

similarly. The global credit bubble,

Bernanke's savings glut, will collapse in due course. But it seems

to me we aren't there yet & therefore are beset by inflation.

Posted by: Anonymous at August 17, 2008 11:57

AM

Posted by: OER at August 15, 2008 10:49 PM

sjp wrote:Inflation is about the price level moving up.

I am bringing this up because the true mechanics of inflation

must be a combination of (among other things) the extension of money/credit

that algernon refers to and the raising of prices that I posited.

One can't just point the finger at money supply expansion as the

root of inflation. It is clearly an important part, but not the

complete picture.

sjp,

I will pass on your incorrect definition of inflation as price

increases to stay on topic.

Can you give me the mechanism where prices can increase with

a constant money supply without reducing consumption? If you have

an economy of $5 and 5 things how can the price of the each thing

move to $1.10 and consumers still consume 5 things with a $5 money

supply?

Posted by: DickF at August 16, 2008 02:28 PM

DickF - they'd put it on their visas!

When economists talk about wage demands being muted, they don't

seem to understand how much American households have gotten into

the habit of taking their future wages out as borrowed money. If

I have the ability to pay 1.10 with a credit card, I can overlook

that shortfall in my real income. By using behavioral patterns which

were true in the 70s but are not true today to connect commodity

prices to wages, economists are overlooking a central feature of

the economy they have wrought. In fact, dissolving limits on credit

has been the only way that the "grand moderation" could be swallowed

by the American public at large. If they had to live within their

real incomes, the increases in the compensation of the wealthiest

group - the CEOS, the hedge funders - would simply be politically

impossible. As credit is squeezed and Americans have to live within

their real incomes, look for inequality to become a much hotter

issue. It is the credit squeeze more than inflation that is going

to jumpstart pressure to raise wages.

DickF: my definition of inflation is a rise in the price

level. The only point I'm making is to dispute algernon's point;

I took algernon's point to be that inflation comes solely from

money supply expansion. I say that's not true.I believe that

the problem subsequently raised with my thought experiment (0

growth, 0 money supply growth, price increases) is that it is

non-equilibrium. What Anonymous suggested makes sense. On the

other hand, the economy might realize that the price increases

weren't warranted and drop the price back down -- this might

be the outcome DickF sees for his scenario. I thought a non-equilibrium

thought experiment might be worth considering, though, since

the jumping off point for this post is that the oil price increases

we saw in the summer have been followed by price decreases:

we are talking about fluctuations about the equilibrium.

I am most interested in Justin's point, that these oil price

fluctuations might inordinately affect consumers' inflation

expectations. It makes me wonder if certain high-profile products

are weighted highly in consumers' belief formation mechanisms.

Have oil price shocks been associated with shocks to consumers'

inflation expectations, and is this association stronger than

the association with other commodities?

Posted by: sjp at August 17, 2008 02:21 PM

DickF asks "Can you give me the mechanism where prices can increase

with a constant money supply without reducing consumption?"Simple,

the rate of circulation of money can increase or decrease. Thus

even if the supply of money remains the same prices can change.

And of course, there are many types of virtual money that can step

into the gap, taking the place of money, debit accounts, credit

accounts, loans of all descriptions etc.

Posted by:

bill j at August

18, 2008 03:54 AM

Roger,Your comment about Visas did make me laugh, but understand

that credit works within an economy unless the government facilitates

credit expansion with an increase in the money supply so credit

in itself does not create inflation.

sjp,

Inflation is a decline in the value of money. It may lead to

a rise in the price level, but a rise in the price level is not

inflation. This is a huge misconception in economic circles that

leads to serious misunderstandings.

If you introduce other elements into your thought experiment

such as consumption preferences then yes you can create a scenario

where such price increase might be accomodated, but the thought

process must be deeper than a fixed money supply with rising prices.

That simply is not possible without external input meaning consumption

preferences, saving preferences, etc.

This is important to understand because without the complicity

of the monetary authorities an economy cannot experience inflation.

Understand that a change in consumption preferences is not inflationary.

bill j,

A change in circulation of money does not exist in a vacuum.

There must be other changes such as consumption preferences for

this to happen. Dig deeper.

So now we have magazine covers fretting over oil, pundits everywhere

calling for $200 oil, and BusinessWeek articles "Bracing For Inflation"

in spite of a slowing world economy. These are all contrarian indicators.

And as goes oil, so goes the CPI. So unless there is a breakout

of War in the Mideast, the oil bust may be deeper and longer lasting

than anyone thinks.

While even moral hazard hawks generally agree that some sort

of government intervention would be needed in the event of financial

trouble at Fannie and Freddie, the most compelling reason was that

the US, chronically dependent on foreign funding, would be ill advised

to treat its money sources badly.

Of the GSEs' $5.2 trillion in debt (their own corporate bonds

plus MBS),

$1.3 trillion is in the hands of foreign investors and central banks.

The speed with which the powers that be cobbled together a support

program was seen in some circles as an admission of the importance

of reassuring our friendly overseas credit suppliers.

If that was the motivation, it isn't working. As we and others

noted, spreads on

GSE debt have risen to 215 basis points over Treasuries, only

a tad shy of the pre-Bear crisis level of 238 basis points. And

remember, they have reached this stratospheric levels despite the

Paulson rescue package, despite an alphabet soup of new Fed facilities

that accept GSE paper as collateral (as the discount window did)

now in place (although there were raspberries all around for the

bailout bill, due to its failure to make any changes in the operation,

management, or policies of the GSEs and its lack of specificity

as to triggers and what mechanism would be used).

And the reason? A big factor is that

foreign central banks are exiting GSE debt and have pulled back

significantly from purchases of new paper. This vote

of no confidence appears likely to force the Administration's hand

and lead it to take more concrete measures to prop up Freddie's

and Fannie's balance sheets. They are not about to risk a spike

in mortgage rates and further trouble in the housing markets with

elections approaching.

From

Reuters:

An extraordinary Treasury capital infusion may be needed to

restore faltering foreign demand for debt issued by Fannie Mae

and Freddie Mac, the two top home funding sources that the government

is willing to rescue to save the housing market.The companies

rely heavily on overseas investment, often up to two-thirds

of each new multibillion-dollar note offering, to help pare

funding costs and keep mortgage rates low.

But foreign central banks have dumped nearly $11 billion

from their record holdings of this debt in four weeks, to $975

billion, and won't return in force before it's clear if -- and

how -- the government will back Fannie and Freddie, some analysts

say....

The bonds these companies issue in the $4.5 trillion agency

MBS market are near or worse than the weakest levels, set in

March before the government engineered the sale of failing Bear

Stearns to JPMorgan.

... ... ...

Overseas investors took an atypical back seat in Fannie Mae's

three-year note sale this week.

Central banks bought just 37 percent of the $3.5 billion

issue, down from 56 percent in May's $4 billion offering of

the same maturity. Asia accounts took just 22 percent of the

notes, down from 42 percent in May....

Comments

Looks like a weak article which generated interesting comments.

The key question is whether peak oil will negatively influence international

trade. It is clear that distance now matters more.

Will the rising price of oil reduce international trade as some

have suggested? According to this research, which uses a gravity

model of international trade to answer the question, thpntries trade

more on international markets today than ever before � both in absolute

terms and as a proportion of their national output. How can we explain

this phenomenal increase in international trade over the past few

decades? Will the recent

rise in oil prices

reverse this trend of globalisation?

History provides us with a natural comparison. Beginning in the

nineteenth century, the world saw a remarkable rise in international

trade that came to a grinding halt during World War I and later

on in the wake of the Great Depression. This "first

wave of globalisation" from about 1870 until 1913 led to a degree

of international integration � measured by trade-to-output ratios

� that many countries only achieved again in the mid-1990s.

Taking a comparative perspective, we juxtapose the first wave

of globalisation from 1870 to 1913 and the second wave after World

War II. We also study the retreat of world trade during the interwar

period from 1921 to 1939. We are interested in the driving forces

behind these trade booms and trade busts. Was it changes in global

output or changes in trade costs that explain the evolution of international

trade?

Comments

- Trance says...

- "for example, consumers have managed oil prices at almost five

times the going price before the 70s inflation."

but this is done

at the cost of diminishing discretionary income (which is worse

in Europe than US). This discretionary income would otherwise go

elsewhere in the economy. This money now goes into only one pocket,

the oil industry.

- Bruce Wilder says...

- "they find that there is little systematic evidence to suggest

that the maritime transport revolution was a primary driver of the

late nineteenth century global trade boom. Rather, the most powerful

force driving the boom was the secular rise in incomes across countries."

"the key innovations in the shipping industry were induced technological

responses to the heightened trading potential of the world."

I think one would have to have a much better model of international

trade, to sort this out reliably. Talking rather generically and

bloodlessly about "the secular rise in incomes" seems almost a distraction.

What drives trade, international and local, are the productivity

gains from specialization. These gains from specialization can rest

on a variety of quite different bases. By focusing on "international"

trade in particular, we are focusing on goods, where the productivity

gains from specialization are extreme. In common parlance, there

might be a monopoly of technical knowledge, extreme economies of

scale or external economies, or a gift of nature, which can be exploited

in only rare places. Not very many people will find it worthwhile

to go more than a few blocks to get a haircut, even though most

people will go to a professional barber or hairstylist. On the other

hand, prospecting for oil in one's backyard, or refining it one's

self, is rarely worthwhile. Nor do people go to a local craftsman

for a television or cellphone.

The period, 1870-1913, marks the

Second Industrial Revolution, a misnamed third or fourth phase

of industrial revolution that began in Britain in the 18th century.

Steamships were rather famously a central part of this phase --

their ability to keep to a schedule as important as their speed

and capacity, and the ability to adapt them to more efficient means

of carrying specialized cargoes (oil tankers, refrigerated ships,

etc)

In addition, the industrial revolution was widening its geographical

scope in three important respects. First, the industrial revolution

was spreading out, to the Low Countries, Switzerland, France, the

U.S. and Germany. After 1820, the industrial revolution was no longer

occurring in one country only, and it was accelerating. Moreover,

after 1870, the industrial revolution was involving more and more

industries, moving from textiles and steam engines and railroads,

to steel, oil, chemicals, electricity, with leadership often passing

to countries other than Britain.

And, thirdly, as the industrial revolution drove economic growth,

it drove demand for the fruits of the earth, sucking up everything

from guano and bananas to copper and petroleum from distant places.

The ability to wrest enormous factor productivity gains from

specced by the extent of the market, then we shouldn't be surprised

to see the rise of national consumer markets in response to transportation

and communication innovations: this is the period in which J. Walter

Thompson invented magazine advertising (1877), and brandnames emerge,

Nabisco (1901) and Coca-Cola (1886) and Lucky Strike (1871, 1907),

Colgate toothpaste (1872) and Palmolive soap (1898).

Somehow, for me, "the secular rise in incomes" doesn't quite

cover it.

If one is not going to be serious about analyzing what drives

trade, I don't see how empty statements projecting that trends can

continue really mean anything.

The right thing is to think seriously about distinguishing between

the factors driving trade in commodities and fruits of the earth,

and what drives trade in manufactured goods, and, finally, what

drives trade in services. Underlying all of this is what drives

specialization.

Peak oil implies no further gross increases in trade in raw petroleum.

Similar considerations apply to many raw mineral products, like

copper and zinc, and other commodities. Industrial development and

rising population in the Persian Gulf will also result in more trade

in petroleum products, as the expense of raw petroleum.

Peak oil also implies rising relative cost of jet fuel -- air

travel is going to get more expensive, and with vacation travel

to exotic places. (Recreational and business travel is a significant

part of international trade.)

The kind of intense specialization, which yields enormous factor

productivity enhancement, typically involves a coordination and

control, which entails communication. Communication advances were

important complements to the increasing speed and falling cost of

transporation in 1870-1913, as well as now.

A useful analytical exercise might focus on whether falling communication

costs, increasing capability imply more or less physical trade in

goods. McDonald's, Toyota, IKEA, Lenovo -- are the limits to economies

of scale of physical product in one place such that, say, all the

corkscrews in the world should be made in one place?

Or, does falling costs of communication and control imply more

widely distributed physical production of manufactured goods and

less physical transport?

If we could leverage computers to design a washing machine plant,

to flexibly build several different models or designs of washing

machines, would we care to import washing machines from Sweden or

Italy or China, and would they want to import washing machines from

Benton Harbor, Michigan?

How does the financial interact with trade? If a country fails

to invest in the production capacity to make and export goods and

services in sectors where the gains in total factor productivity

are greatest, how does that affect the terms of trade? Median incomes?

If not "protectionism", what is an organizing principle for a national

strategy? (Is there nothing more convincing that pieties about education,

and taxcuts for plutocrats?)

- robertdfeinman says...

- Perhaps the analysis is backwards. The rise of highly efficient

production produced an excess of manufactured goods (or at least

the capacity to make them). This then led firms to seek markets

elsewhere. Because of the efficiency trade costs were not enough

to deter this trend.

As trade increased the efficiency of trade also improved and

its costs dropped as well. The depression caused a loss of markets

and trade dropped. The "protectionism" was a political attempt to

fix something which was misguided effort, just like offshore drilling

is the wrong fix now. The lack of markets caused a drop off in innovation

so trade costs stopped dropping, then the wars intervened and destroyed

productive capacity and markets.

In the latest round, the cycle has repeated, this time there

has been a new set of innovations in IT and supply chain management

and a corresponding rise in efficiency with containerization and

high speed ships. Both these improvements have now stalled so other

factors have started to become more important.

The response to this has been yet another set of political nostrums

designed for their ear appeal to the public, rather than for their

efficacy.

Just a conjecture...

- roger says...

- Huh, is this economics of numerology:

"To answer that question

we set up a gravity model of international trade. This model borrows

Isaac Newton's insight that the gravitational force between two

planets in space is inversely related to their physical distance.

Instead of planets, we consider countries whose "gravitational force"

is the amount of their bilateral exports and imports. Instead of

physical distance, bilateral trade is impeded by trade costs such

as transportation costs, tariffs and language barriers."

Wow, and this is considered serious economics! Why not borrow

their model from, say, Revelations, where the antichrist - protectionists

- put a bar code on their followers heads, with the bar code being

legislation designed to discourage trade. It would make the same

amount of sense.

This doesn't even achieve a low level of chicanery.

- dissent says...

- "overall, history gives us little reason to expect a sharp and

fundamental reaction of international trade in response to changes

in transportation costs."

The problem

with this argument is that all prior history took place prior to

peak oil. Transportation costs will be impacted by peak oil in a

historically anomalous fashion.

Krugnam understanding of politics is definitely limited, but the

observation that there will be more intense struggle for limited natural

resources might be true...

Is the "second great age of globalization" about to end?:

The Great Illusion, by Paul Krugman, Commentary, NY Times:

...as I was reading the latest bad news, I found myself

wondering whether this war is an omen - a sign that the second

great age of globalization may share the fate of the first

... ... ...

But then came three decades of war, revolution, political

instability, depression and more war. By the end of World War

II, the world was fragmented economically as well as politically.

And it took a couple of generations to put it back together.

So, can things fall apart again? Yes, they can.

Consider ... the current food crisis. For years we were told

that self-sufficiency was ... outmoded..., that it was safe

to rely on world markets for food supplies. But when the prices

of wheat, rice and corn soared, Keynes's "projects and politics"

of "restrictions and exclusion" made a comeback: many governments

rushed to protect domestic consumers by banning or limiting

exports, leaving food-importing countries in dire straits.

... ... ...

Angell was right to describe the belief that conquest pays

as a great illusion. But the belief that economic rationality

always prevents war is an equally great illusion. And today's

high degree of global economic interdependence, which can be

sustained only if all major governments act sensibly, is more

fragile than we imagine.

Lee A. Arnold says...

The illusion? Keynes' Londoner had no inkling that the reason

he could telephone products from around the world was because

of the British Empire's militarism and imperialism? This seems

a bit disingenuous on JMK's part. Or maybe sarcastic? Then the

very next thing: Your history quiz: Where were the first British

troops sent when Archduke Ferdinand was shot? Answer: To Basra

-- because the German and British navies had both just converted

from coal to oil, and Germany was going to extend the Orient

Express past Constantinople to take all the petroleum in the

area out by rail. When Ferdinand was shot, everything went up

into the air... Starting the ninety-year (so far) resource war.

Now the U.S. is run by climate-denying gasoholics and the American

public apparently hasn't guessed the possibility that their

leaders have handed Iraq to Iran's best friends and the Shi'ites

are merely standing-down and smiling until the Americans leave.

So it looks like Bush and Cheney must change the regime in Iran,

in order to exit Iraq. No wonder David Kilcullen, Petraeus'

counterinsurgency consultant, called the invasion "fucking stupid."

(Later changed to an "extremely serious strategic error.") With

which the entire foreign policy community (except for the numbnuts

neocons) and all the military analysts heartily agree. The U.S.

could be tied-down there for generations. But but but Victory

looms large, baby! So the Russians take a piece, while the right-wing

howls it's totally unjustified. Well of course it is, you dumbasses.

And the Russians might have done it anyway. But you throw things

up in the air, all sorts of people start grabbing.

Alex Tolley says...

But the belief that economic rationality always prevents war

is an equally great illusion. And today's high degree of global

economic interdependence, which can be sustained only if all major

governments act sensibly, is more fragile than we imagine.

Anyone with the slightest sense of history does not have these

illusions. All the knowledge gained in the last 100 years that could

be used to understand how best to manage human affairs is overridden

by base human nature. In our (US) own milieu, we have at least half

the population that is effectively anti-science and prefers to make

emotional decisions and votes for political candidates that do the

same thing. The US congress routinely votes on emotional or ideological

lines only. I see no evidence that the rest of the world is any

less irrational.

A very important book now available for free..

Yet gold crashes. It has failed to deliver on its core promises

as a safe-haven and inflation hedge, at least for now. Why?

Four possible answers:

1) Nobody seriously believes that Russia will over-play its

hand. The world could not care less about Georgia anyway. Ergo,

this is a bogus geopolitical crisis.

2) The inflation story is vastly exaggerated in the OECD

core of countries that still make up 60pc of the global economy.

The price of gold is already looking beyond the oil and food

spike of early to mid 2008 (a lagging indicator of loose money

two to three years ago) to the much more serious matter of debt-deflation

that lies ahead.

3) The seven-year slide of the dollar is over as investors

at last wake up to the reality that the global economy is falling

off a cliff. Indeed, the US is the only G7 country that is not

yet in or on the cusp recession. (It soon will be, but by then

others will be prostrate). As an anti-dollar play, gold is finished

for this cycle.

4) The entire commodity boom has hit the buffers. Looming

world recession (growth below 3pc on the IMF definition) trumps

the supercycle for the time being.

Gold has fallen from $1030 an ounce in February to $807 today

in London trading. It has collapsed through key layers of technical

support, triggering automatic stop-loss sales.

The Goldman Sachs short-position that

I have been observing with some curiosity has paid off.

For gold bugs, the unthinkable has now happened. The metal has

fallen through its 50-week moving average, the key support line

that has held solid through the seven-year bull market. This week

is not over yet, of course. If gold recovers enough in coming days,

it could still close above the line.

Courtesy of my old colleague Peter Brimelow - whose columns on

gold are a must-read - note that

Australia's Privateer point and figure chart has also broken

its upward line for the first time since 2002. This is serious technical

damage.

So have we reached the moment when gold bugs must start questioning

their deepest assumptions. Have they

bought too deeply into the "dollar-collapse/M3 monetary bubble"

tale, ignoring all the other moving parts in the complex global

system? Nobody wants to be left holding the bag all

the way down to the bottom of the slide, long after the hedge funds

have sold out.

Well, my own view is that gold bugs

should start looking very closely at something else: the implosion

of Europe. (Japan is in recession too)

Germany's economy shrank by 1pc in Q2. Italy shrank by 0.3pc.

Spain is sliding into a crisis that looks all too like the early

stages of Argentina's debacle in 2001. The head of the Spanish banking

federation today pleaded with the European Central Bank for rescue

measures to end the credit crisis.

The slow-burn damage of the over-valued euro is becoming apparent

in every corner of the eurozone. The

ECB misjudged the severity of the downturn, as executive board member

Lorenzo Bini-Smaghi admitted today in the Italian press.

By raising interest rates into the teeth of the storm

last month, Frankfurt has made it that much more likely that parts

of Europe's credit system will seize up as defaults snowball next

year.

As readers know, I do not believe the eurozone is a fully workable

currency union over the long run. There was a momentary "convergence"

when the currencies were fixed in perpetuity, mostly in 1995. They

have diverged ever since. The rift between North and South was not

enough to fracture the system in the first post-EMU downturn, the

dotcom bust. We have moved a long way since then. The Club Med bloc

is now massively dependent on capital inflows from North Europe

to plug their current account gaps: Spain (10pc), Portugal (10pc),

Greece (14pc). UBS warned that these flows are no longer forthcoming.

The central banks of Asia, the Mid-East,

and Russia have been parking a chunk of their $6 trillion reserves

in European bonds on the assumption that the euro can serve as a

twin pillar of the global monetary system alongside the dollar.

But the euro is nothing like the dollar. It has no European government,

tax, or social security system to back it up. Each member country

is sovereign, each fiercely proud, answering to its own ancient

rythms.

It lacks the mechanism of "fiscal transfers" to switch money

to depressed regions. The Babel of languages keeps workers pinned

down in their own country. The escape valve of labour mobility is

half-blocked. We are about to find out whether EMU really has the

levels of political solidarity of a nation, the kind that holds

America's currency union together through storms.

My guess is that political protest will mark the next phase of

this drama. Almost half a million people have lost their jobs in

Spain alone over the last year. At some point, the feeling of national

impotence in the face of monetary rule from Frankfurt will erupt

into popular fury. The ECB will swallow its pride and opt for a

weak euro policy, or face its own destruction.

What we are about to see is a race to the bottom by the world's

major currencies as each tries to devalue against others in a beggar-thy-neighbour

policy to shore up exports, or indeed simply because they have to

cut rates frantically to stave off the consequences of debt-deleveraging

and the risk of an outright Slump.

When that happens - if it is not already happening - it will

become clear that the both pillars of the global monetary system

are unstable, infested with the dry rot of excess debt.

The Fed has already invoked Article 13 (3) - the "unusual and

exigent circumstances" clause last used in the Great Depression

- to rescue Bear Stearns. The US Treasury has since had to shore

up Fannie and Freddie, the world's two biggest financial institutions.

Europe's turn will come next. We will discover that Europe cannot

conduct such rescues. There is no lender of last resort in the system.

The ECB is prohibited by the Maastricht Treaty from carrying out

direct bail-outs. There is no EU treasury. So the answer will be

drift and paralysis.

When EU Single Market Commissioner Charlie McCreevy was asked

at a dinner what Brussels would have done if the eurozone faced

a crisis like Bear Stearns, he rolled his eyes and thanked the Heavens

that so such crisis had yet happened.

It will.

Gold bugs, you ain't seen nothing yet. Gold at $800 looks like

a bargain in the new world currency disorder.

[Aug 14, 2008] Making Markets Work for Everyone

This is an important post that shows how free market retoric was

abused to enrich few at the expence of many...

Greg Anrig via Brad DeLong:

Greg Anrig on the GOP, by Brad DeLong: He smells a wind

from out of the west:

McCain's Problem Isn't His Tactics. It's GOP Ideas.:

At long last, the conservative juggernaut is cracking up.

From the Reagan era until late 2005 or so, conservatives

crushed progressives like me in debates as reliably as the

Harlem Globetrotters owned the Washington Generals. The

right would eloquently praise the virtues of free markets

and the magic of the invisible hand. We would respond by

stammering about the importance of regulation and a mixed

economy, knowing even as the words came out that our audience

was becoming bored.

Conservatives would get knowing laughs by mocking bureaucrats.

We would drone on about how everyone can benefit from the

experience and expertise of able civil servants. ... They

offered tax cuts. We talked amorphously about taxes as the

price of a civilized society. ...

But now, seemingly all of

a sudden, conservatives are the ones who are tongue-tied,

as demonstrated by Sen. John McCain's limping, message-free

presidential campaign. McCain's ongoing difficulties in

exciting voters aren't just a tactical problem; his woes

stem largely from his long-standing adherence to a set of

ideas that simply haven't worked in practice.

The belief system and finely crafted policy pitches that

enabled the right to dominate the war of ideas for the past

30 years have produced a relentless succession of governing

failures, from Iraq to Katrina to the economy to the environment.

Largely as a consequence, the public's attitude toward

government -- Ronald Reagan's b�te noire -- has shifted.

A recent Wall Street Journal/NBC News poll found that, by

a 53-to-42 percent margin, Americans want government to

"do more to solve problems"; a dozen years ago, respondents

opposed government action by 2 to 1. Meanwhile, Republican

constituency groups' long-standing determination to put

aside their often significant differences and band together

to support GOP candidates is fracturing: The libertarian

darling Ron Paul and the evangelical Christian leader James

C. Dobson are among the Republican bigwigs who haven't so

far endorsed McCain. ...

As I listen to leading voices and thinkers on the right

pondering the condition of their ideology, it is increasingly

clear to me that they face a fundamental dilemma -- one

that cannot be resolved anytime soon and that might well

leave the conservative movement out to pasture for as long

as we progressives have been powerlessly chewing grass.

That choice is whether to stick with rhetoric and policies

wedded to free markets, limited government and bellicose

unilateralism, or to endorse a more robust role for the

public sector at home while relying more on diplomacy and

international institutions abroad.

Either way, conservative Republicans seem destined

to have a much harder time winning elections for the foreseeable

future. Just ask McCain how much fun he's having.

The single theme that most animated the modern conservative

movement was the conviction that government was the problem

and market forces the solution. It was a simple, elegant,

politically attractive idea, and the right applied it to

virtually every major domestic challenge -- retirement security,

health care, education, jobs, the environment and so on.

Whatever the issue, conservatives proposed substituting

market forces for government -- pushing the bureaucrats

aside and letting private-sector competition work to everyone's

benefit.

So they advocated creating health savings accounts, handing

out school vouchers, privatizing Social Security, shifting

government functions to private contractors, and curtailing

regulations on public health, safety, the environment and

more. And, of course, they pushed to cut taxes to further

weaken the public sector by "starving the beast." President

Bush has followed this playbook more closely than any previous

president, including Reagan, notwithstanding today's desperate

efforts by the right to distance itself from the deeply

unpopular chief executive.

But in practice, those ideas have all failed to deliver...

Conservatives will contest that "President Bush has followed

this playbook more closely than ... Reagan." They'll try to

argue that the problem is the Bush administration, not conservative

ideas. In fact, liberals

make this argument too:

[T]he free-market, supply-side crowd... had behind them

the authority of a vast academic establishment, ranging

from Friedrich von Hayek to Milton Friedman to such contemporaries

as Gary Becker and Robert Mundell... The academic economics

of the 1970s lined up behind the right-wing politics of

the 1980s for a reason. Reaganomics had a logic. ... Deregulation,

above all, would substitute the invisible hand of the "efficient

market" for the dead hand of bureaucracy.

The judicial coup of December

2000 that installed Bush and Cheney brought back some of

Reagan's men and his most extreme policies - tax cuts for

the wealthy, big increases in military spending, aggressive

deregulation. But it didn't bring back the

ideas. Instead, it became clear that Bush and Cheney had

no real ideas, no larger public justification. They cut

taxes to enrich their supporters. ... They were willing

to have the government spend like a drunken sailor in 2003/4

to boost the economy before the election. ...

It was very interesting to me that some of the first

to sense this loss of public purpose were the very conservatives

who had swept in with Reagan. The nemeses of my youth, people

like Bruce Bartlett, Paul Craig Roberts, the late Jude Wanniski,

went over into hard opposition..., at the core they felt

that Bush had no conservative convictions.

The free market rhetoric still has power even when it offers

false hopes. In previous campaigns we heard how tax cuts would

pay for themselves. Cut taxes and get the government out of

the way, the argument goes, and output will grow so much that

taxes will actually rise. That, of course, didn't happen. This

campaign, it's offshore drilling. Offshore drilling won't lower

oil prices, that's a false hope, yet the cry that government

imposed environmental restrictions are causing higher prices

has had some success. Let the market work, we hear, and it will

solve the problem. There are other of signs that politicians

are not yet ready to abandon the free-market message. When it

comes to health care reform, the Obama campaign fears the word

mandates for a reason, and prefers to push a plan that

has "many private health insurance options." Talk of raising

taxes and increasing the size of government is avoided, and

Democrats step very lightly around free trade. The idea that

the market works still has resonance.

So my instinct is different.

Markets do what we expect them to do - they allocate resources

efficiently - when they operate under the proper conditions.

Those conditions include lack of market power among market participants,

the lack of political influence, having the proper regulatory

structure in place, and so on. Using anti-government ideology,

conservatives have undermined rather than supported the market

system, and that's the important message. Take deregulation

as an example. There were certainly places where government

overreached, and removing regulations in those cases was needed,

but thoughtlessly stripping away any rule or regulation pertaining

to business that you encounter is not the way to create a market

system that functions optimally.

I want Democrats to make it clear that we aren't opposed

to markets, not at all, and to say it forcefully. In fact, we

like markets so much we want to fix the ones that are broken

from so many years of neglect by Republican administrations.

We want to make markets work for everyone, not just a few at

the very top who are able to work the system to their advantage.

We have a pretty good idea of what it takes for markets to function

well, and it requires active government involvement to create

the conditions and supporting institutions for markets to flourish.

That type of government oversight has been absent under Republican

administrations - see the financial meltdown - and it's up to

Democrats to step up and fill the void.

The confusion here is simple, I think. Free markets - where

free simply means minimal government involvement - are not necessarily

the same as competitive markets. There is nothing that says

what many interpret as freeing markets - lifting all government

restrictions - will give us competitive markets, not at all.

Government regulation (as well as laws, social norms, etc.)

is often necessary to help markets approach competitive ideals.

Environmental restrictions that force producers to internalize

all costs of production make markets work better, not worse.

Rules that require full disclosure or that impose accounting

standards help to prevent asymmetric information and improve

market outcomes. Breaking up firms that are too large prevents

exploitation of monopoly power (or prevents them from becoming

"too large to fail") which can distort resource flows and distort

the distribution of income. Making sure that labor negotiations

between workers and firms are on an equal footing doesn't move

markets away from an optimal outcome, just the opposite, it

helps to move us toward the efficient, competitive ideal, and

it helps to ensure that labor is rewarded according to its productivity

(unlike in recent years where real wages have lagged behind).

There is example after example where government involvement

of some sort helps to ensure markets work better by making sure

they are as competitive as possible.

I don't think it's necessary to give up on the idea of the

market system as the best means of allocating resources in most

cases. But markets can and do fail and it's up to the government

to provide the foundation markets need to perform well (or,

in cases where market failures are substantial such as in health

care and social security, to step in and take a more active

role). That's what has been missing under Republican leadership,

the understanding of how to provide the foundation needed for

markets to work for everyone. Democrats need to stress how that

will change under their leadership, how they will improve the

ability of the economy to function in a way that serves the

interests of all participants in the economy rather than favoring

some groups over others.

[Aug 14, 2008] The Heart of the Economic Mess

The Federal Reserve Board's "beige book" for June and July offers

a clear explanation for why the economy has slowed to a crawl.

It shows American consumers cutting

way back on their purchases of everything from food to cars to appliances

to name-brand products. As they do so, employers

inevitably are cutting back on the hours they need people to work

for them, thereby contributing to a downward spiral.

The normal remedies for economic downturns are necessary. But

even an adequate stimulus package will offer only temporary relief

this time, because this isn't a normal downturn.

The problem lies deeper. Most Americans

can no longer maintain their standard of living. The only lasting

remedy is to improve their standard of living by widening the circle

of prosperity.

The heart of the matter isn't the collapse in housing prices

or even the frenetic rise in oil and food prices. These are contributing

to the mess but they are not creating it directly. The basic reality

is this: For most Americans, earnings

have not kept up with the cost of living. This is

not a new phenomenon but it has finally caught up with the pocketbooks

of average people. If you look at the earnings of non-government

workers, especially the hourly workers who comprise 80 percent of

the workforce, you'll find they are barely higher than they were

in the mid-1970s, adjusted for inflation. The income of a man in

his 30s is now 12 percent below that of a man his age three decades

ago. Per-person productivity has grown considerably since then,

but most Americans have not reaped the benefits of those productivity

gains. They've gone largely to the top.

Inequality on this scale is bad for many reasons but it is also

bad for the economy. The wealthy devote a smaller percentage of

their earnings to buying things than the rest of us because, after

all, they're rich. They already have most of what they want. Instead

of buying, the very wealthy are more likely to invest their earnings

wherever around the world they can get the highest return.

This underlying earnings problem has been masked for years as

middle- and lower-income Americans found means to live beyond their

paychecks. But they have now run out of such coping mechanisms.

As I've noted elsewhere, the first coping mechanism was to send

more women into paid work. Most women streamed into the work force

in the 1970s less because new professional opportunities opened

up to them than because they had to prop up family incomes. The

percentage of American working mothers with school-age children

has almost doubled since 1970 - to more than 70 percent. But there's

a limit to how many mothers can maintain paying jobs.

So Americans turned to a second way

of spending beyond their hourly wages. They worked more hours.

The typical American now works more each year than he or she did

three decades ago. Americans became veritable workaholics, putting

in 350 more hours a year than the average European, more even than

the notoriously industrious Japanese.

But there's also a limit to how many hours Americans can put

into work, so Americans turned to a third coping mechanism. They

began to borrow. With housing prices rising briskly through the

1990s and even faster from 2002 to 2006, they turned their homes

into piggy banks by refinancing home mortgages and taking out home-equity

loans. But this third strategy also had a built-in limit. And now,

with the bursting of the housing bubble, the piggy banks are closing.

Americans are reaching the end of their ability to borrow and lenders

have reached the end of their capacity to lend. Credit-card debt,

meanwhile, has reached dangerous proportions. Banks are now pulling

back.

As a result, typical Americans have

run out of coping mechanisms to keep up their standard of living.

That means there's not enough purhasing power in the economy to

buy all the goods and services it's producing. We're finally reaping

the whirlwind of widening inequality and ever more concentrated

wealth.

The only way to keep the economy going over the long run is to

increase the real earnings of middle and lower-middle class Americans.

The answer is not to protect jobs through trade protection. That

would only drive up the prices of everything purchased from abroad.

Most routine jobs are being automated anyway. Nor is the answer

to give tax breaks to the very wealthy and to giant corporations

in the hope they will trickle down to everyone else. We've tried

that and it hasn't worked. Nothing has trickled down.

Rather, the long-term answer is for us to invest in the productivity

of our working people -- enabling families to afford health insurance

and have access to good schools and higher education, while also

rebuilding our infrastructure and investing in the clean energy

technologies of the future. We must also adopt progressive taxes

at the federal, state, and local levels. In other words, we must

rebuild the American economy from the bottom up. It cannot be rebuilt

from the top down.

NEW YORK (CNNMoney.com) -- John McCain's call for a big push

into nuclear power can certainly be met - if the country is willing

to pay more for power and tolerate the safety risks.

Earlier this week McCain, the presumptive Republican nominee

for president, said he wants to build 45 more nuclear power plants

to make the country more energy independent. That would add significantly

to the nation's current fleet of 104 active plants, which produce

about 20% of the nation's power.

The advantages to nuclear power are primarily two-fold: It doesn't

emit greenhouse gases, and it is a reliable form of electricity

produced from uranium - a fairly abundant domestic resource.

McCain and others have been touting nuclear energy as a possible

replacement for foreign oil, if and when the country shifted to

electric cars.

The utility industry is behind the construction of more nuclear

plants.

"We have been saying for years that we have to not only preserve

our current fleet [of nuclear plants], but enlarge it significantly,"

said Jim Owen, a spokesman for the Edison Electric Institute.

NEW YORK (CNNMoney.com) -- Nearly two-thirds of U.S. companies and

68% of foreign corporations do not pay federal income taxes, according

to a congressional report released Tuesday.The Government Accountability

Office (GAO) examined samples of corporate tax returns filed between

1998 and 2005. In that time period, an annual average of 1.3 million

U.S. companies and 39,000 foreign companies doing business in the

United States paid no income taxes - despite having a combined $2.5

trillion in revenue.

The study showed that 28% of foreign companies and 25% of U.S.

corporations with more than $250 million in assets or $50 million

in sales paid no federal income taxes in 2005. Those companies totaled

a combined $372 billion in sales for the largest foreign companies

and $1.1 trillion in revenue for the biggest U.S. companies.

The GAO report, which did not name any specific companies, said

that some corporations reported zero

income before deducting expenses while others said they had zero

net income after deducting expenses. Either way,

those companies reported no tax liability, the GAO said.

... ... ...

The study was requested by Sens. Byron Dorgan, D-N.D, and Carl

Levin, D-Mich., in an attempt to determine if corporations are abusing

so-called transfer prices.

Transfer prices are charges on transactions between subsidiary

companies within a larger corporate group. Companies may try to

lessen their U.S. tax hit by improperly transferring income to foreign

subsidiaries in countries with lower rates.

The GAO study did not attempt to determine if companies were

abusing transfer prices, but it said that potential abuse of transfers

could reduce the amount of taxes companies pay in the United States.

"The tax system that allows this wholesale tax avoidance is an

embarrassment and unfair to hardworking Americans who pay their

fair share of taxes," Dorgan said in a statement.

How confident are you in the stock market?

| Very |

25% |

|

| Somewhat |

48% |

|

| I've pulled out all my money

|

27% |

|

[Aug 12, 2008] paper-money.blogspot.comThe

Almost Daily 2� - The Next Three Shoes

"I believe that there is a good chance that the S&P 500 will

re-test and drop below the lows set after the collapse of the dot-com

era." What will happens with poor "all stock" 401K investors if the

author is right ?

August 08, 2008Here's my crack at Nostradamusian macroeconomic analysis.

In my estimation the next three systemic shocks will come in the

form of job loss, the foreclosure driven and fiscally irresponsible

government bailout of Fannie and Freddie and a prolonged secular

bear market meltdown of the stock market.

All of these events, if fully materialized, would likely combine

to present the most significant test of Americans' faith and confidence

in their institutions and way of life seen in many generations.

First, although it has been generally the consensus opinion that

the job market will hold up better during this recession as a result

of the weak job growth seen during the last expansion (i.e. less

jobs gained = less jobs to lose), I beg to differ.

My model (simple extrapolation of 90s recession with some tweaks)

puts the unemployment rate at roughly

7% by next March and where we go from there will

depend largely on the other two shoes.

I believe the real job loss from

the 90s-era consumption boom and bust was simply postponed by the

2000s-era credit-debt boom.

Having no other alternative, Americans will now have to face

the reality and own up to their personal fiscal irresponsibility

and tighten belts causing business confidence to erode and inevitably

leading to substantial job loss.

Next, in what has to be the worst fiscal policy blunder in our

history, the federal government has now positioned itself directly

in the line of fire of the largest financial meltdown of modern

times.

Fannie and Freddie are insolvent

and, having operated as an essentially absurd and fraudulent arbitrage

scam in conjunction with sham co-conspirator mortgage originators

like Countrywide Financial for over a decade, are essentially dead

guarantors walking.

Foreclosures are on the verge of explosive growth as near-prime

and prime underwater households relent to the weight of the current

economic crisis.

Treasury Secretary Paulson's promise of bailout of the GSEs will

carry a tremendously high cost for taxpayers and further exacerbating

the economic malaise and erosion of Americans' confidence and sense

of social fairness.

Finally, I believe that there is

a good chance that the S&P 500 will re-test and drop below the lows

set after the collapse of the dot-com era.

This would represent a logical, yet truly significant, failure

of the private sector as the expansion of the 2000s fully gives

way, blending into the dot-com meltdown

forming a secular bear market trend the likes of which we have not

ever seen.

This would, in a sense, be a GM-ization (NYSE:GM)

of the broader stock market and result in a blaring spotlight being

shined on the ludicrousness of constructing a multi-decade economic

expansion based almost entirely on discretionary consumption and

technological hysteria.

"Reid says banks may lose a total of $1.2 trillion when the books

are closed on the Age of Froth".

As the Age of Froth unwound, inflation became

an even greater ravager of personal wealth.

Aug. 11 (Bloomberg) -- One of the most humbling challenges we scribes

face is to attach a meaningful name to an era.

How do you describe a time of obscenely

easy credit; stock and housing bubbles; stratospheric Wall Street

profits, outlandish banker salaries and general prosperity?

Now that the post-bubble age is prompting painful bailouts as

the world economy reels from a credit crunch and writes down bad

debts, it's time to consider what I call the Age of Froth.

Not only will the aftermath of this epoch be ripe with

bankruptcies, foreclosures and bailouts, it will be a time of great

reckoning. Building equity and saving will be vital.

I derive the concept of froth from former Federal Reserve Chairman

Alan Greenspan, who told Congress on July 20, 2005, that ``the

apparent froth in the housing markets appears to have interacted

with evolving practices in mortgage markets.''

Greenspan's

remarks coincided with the peak of the bubble, when U.S. median