“Regulatory bodies, like the people who comprise them…mellow, and in old age…they

become, with some exceptions, either an arm of the industry they are regulating or senile.”

John Kenneth Galbraith

Money! Backroom Deals! Secrecy! Political Power! Captured Government! Scandal! Suspicion!

Major Money!

"Americans live in Russia, but they think they live in Sweden."

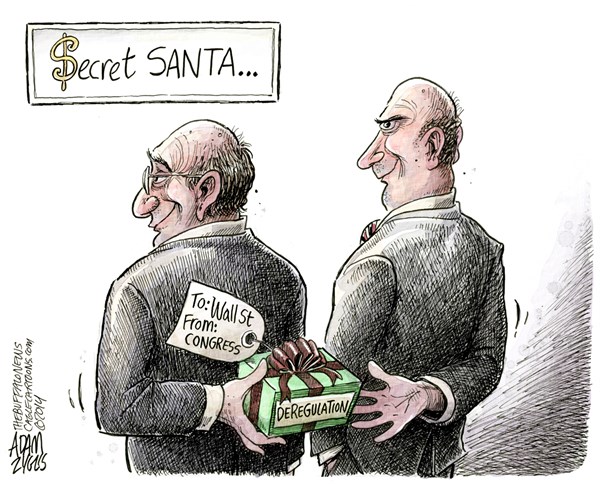

GS makes money by manipulating the system in a quasi-legal, morally corrupt

manner. They challenge all the rules and use the Revolving Door between regulator and regulated

to deliver legal bribes. Society needs better regulators and regulations to protect themselves

from parasites like the GS Vampire Squid.

GS is one of the chief proponents of "Free

Market" ideology. Free Market" is short for "Free to rip off the "Market" . The words "to rip

off" are omitted when they sell the "Free Market" ideology and are reserved for the back rooms

and jokes in private email. The rubes are too dim to get it or else think they are the scammers

and not the scammed.

Immanuel Wallerstein asked an interesting question: is the current iteration of global capitalism

became so dysfunctional that it spells doom for the USA and it's role in the world as well as misery

for American people? The current social system (aka " the current iteration of global capitalism') is

called neoliberalism, or

casino capitalism. It is both ideology and social practice.

As Greenspan noted "an ideology is a conceptual framework with the way people deal with [social]

reality." (in reply to

REP. HENRY WAXMAN)

This second Gilded Age is characterized by rampant speculation and complete dominance of financial

oligarchy over the rest of society (Is

There Capitalism After Cronyism The American Conservative) while the government regulators are intentionally

(or "institutionally" -- "by design") asleep or looking the other way. In other words regulators are

now completely captured by the big banks and are nothing more then stooges of financial oligarchy.

Often they are former staffers of big bands or supporting Wall Street law firms ("criminals with law

degree"), or corrupt academicians on temporary assignment in the particular government body. We all

remember operation of silencing of Brooksley Born

in which prominent role was played by completely corrupt academician

Lawrence Summers and Goldman Sacks'

mole in the government -- Robert Rubin

Wallerstein and his colleagues tried to answer this question in the book

Does Capitalism Have a Future?Thier line on thinking can be simplified to the following statement:

When capital became unable of reaping large and fairly secure profits from manufacturing it like

water tries to find other ways, and first of all criminal. In other words it start criminalizing

finance. From this point of view corruption of regulators is simply "the other way" of reaping

large and fairly secure profits in new "permanent stagnation" condition of "Peak Capitalism", which

entails less use of more expensive fossil fuels ("end of cheap oil").

Some economists even hypothesize that the US economy can expand only

with oil prices below $60 per barrel.

From another point of view, as economist Joseph Schumpeter noted, capitalism is not a

steady-state system. It is unstable system in which population constantly experience and then try to

overcome one crisis after another. Joseph Schumpeter naively assumed that the net result is

reimaging itself via so called “creative destruction". But what we observe now it "uncreative

destruction". In other words casino capitalism is devouring the host. We see that casino capitalism resort of non-creative,

semi-criminal ways of maintaining the rate of profits. Actually this is what the

US elite

did with the country systematically since late 70th.

If we think about capitalism as a set of overlapping networks of power and influence at some point

this destruction not only can be far less "creative" then Schumpeter expected. It can be outright criminal

resembling the way organized crime operates (The

City Of London Has Turned Britain Into A Civilized Mafia State). For example, it can demonstrate

itself in pre-planned, "on-purpose" destruction of the legal framework of the modern state via capture

and corruption of regulators. In other words we see that human society can suffer from something like

"social cancer", when social organism is destroyed in order for tumor sells to grow. And by tumor here

I mean speculative finance and financial oligarchy. Again this is a social system and as such

it does not depend on particular people in power. As Prince Kropotkin observed about prison guards of

Petropavlovsk jail in Sanct Petersburg "People are better then institutions". In a very deep way the

ability to control speculation in the finance sector now became the central problem of any society that

wants to survive in longer term. The idea that speculative behavior is entrepreneurial in nature and

accelerates real economic growth is the fatal error of social judgment (Do

Safer Banks Mean Less Economic Growth ) . But as with cancer the key question is

Can It

Be Contained ?

While under casino capitalism all this "un-creative destruction" is done in order to preserve the

level of profits which with end of cheap energy is impossible obtain

via manufacturing. That does not exclude periods of "return of good times" when overinvestment in energy

led to dramatic drop of oil prices: as soon as weaker players are eliminated the situation gradually

returns to the "new normal". We observed two such periods since the

neoliberalism became world dominant

social system. One immediately after dissolution of the USSR and the second is the current period of

low oil prices which started in late 2014.

If we think about capitalism as a set of overlapping networks of power and influence at

some point this destruction can be far less "creative" then Schumpeter expected. For example it

can demonstrate itself in pre-planned, "on-purpose" destruction of the legal framework of the

modern state via capture and corruption of regulators. In other words we see that human society

can suffer from something like "social cancel", when social organism is destroyed in order for

tumor sells to grow. And by tumor seeks I mean speculative finance. In a very deep way the ability

to control speculation in the finance sector now became the central problem of any society that

wants to survive in longer term.

The idea that speculative behavior is entrepreneurial in nature and accelerates

real economic growth is the fatal error of social judgment (Do

Safer Banks Mean Less Economic Growth ) .

If we assume the big finance business model is somewhat similar to cancer, it is logical that they

need to attack and immobilize the immune system in order to be able to grow fast. Corruption of regulators

also can be viewed as a part of positive feedback loop created in

the society by growth of financial sector. As such this is a systemic, institutional problem,

not the problem of individual corrupt individuals. It is really an immanent, defining feature of

neoliberalism as a social-economic system. In no way it is result of the action of few "bad

apples". Much of is institutional and is related to the the structure of regulation of financial sector,

which under neoliberalism is specifically designed to encourage capture.

As an immanent feature of neoliberal regimes it is also used as a universal "can opener" for more

powerful neoliberal nations to get to the resources of weaker neoliberal nations, and, especially, countries

governed by "resource nationalists".

Accusations of widespread corruption are typical precursor to staging a neoliberal

color revolution in such

countries.

In a sense, the USA is probably most corrupt country in the world as neoliberal regime is strongest

and the most mature in this country (

Why the Fed Is So Wimpy,

by Justin Fox):

Regulatory capture — when regulators come to act mainly in the interest of the industries they

regulate — is a phenomenon that economists, political scientists, and legal scholars have been

writing about for decades. Bank regulators in particular have been

depicted as

captives for years, and have even taken to

describing themselves as such.

The key feature of neoliberal regime is that large transnational corporation are the key political

players which keep Congress and all regulatory agencies of short leash. Or, more correctly, government

and top brass of internationals intermarry. The mixture of mechanisms used (revolving door, lobbyism,

assigning cronies as heads of regulatory agency (Bush II favorite strategy)) can change with the time

but the net result is always the same. As Senator Dick Durbin noted about the Congress

Banks Frankly Own The Place. It's more correctly to say "transnationals own the country".

Started by Carter and continued by Reagan deregulation quickly exhausted its positive momentum of

fighting excessive bureaucracy and government waste and become the way of stealth imposition of

neoliberalism (also known as casino capitalism) on the society. Fundamentally, crony

capitalism and corruption are two sides of the same neoliberal coin be it USA, or Russia, or Brazil.

Fundamentally, crony capitalism and corruption are two sides of the same neoliberal coin

be it USA, or Russia, or Brazil.

The rampant deregulation implemented in the USA in 90th (dismantling Del Deal, immanent due to the

growth of financial sector and its political influence) and "free market capitalism" (as if "free

markets" ever existed; government always control the market via control of the currency; in turn large

market players often control the government) is really side effect of a larger problem: systemic instability

of financial sector. Old mechanisms of purging excessive size of financial sector via anti-Semitism

and expulsion of Jews no longer work.

As soon as the political establishment became openly committed to laissez-faire, they essentially

invite financial sector to hijack the political power in the society ("Quiet

coup"). And financial sector tries to protect their political power by imposing a pretty draconian

regime in the form of the

National Security

State, to exclude any chances of forming a meaningful opposition to their dominance. At this point

mousetrap with cheese in form of "free market" propaganda is closed. After that banksters became completely

immune from public scrutiny and prosecution, as 2008 events proved to the whole world. In a sense all

three last US administrations (Clinton, Bush II and Obama) were/are essentially sock puppets of financial

oligarchy.

The political appointees to federal regulators as the tool for blocking regulation was the key feature

of Casino Capitalism, the variant of neoliberal regime established

in the USA. And their actions are among of the most important contributions to the financial crisis.

Due to this practice, the regulators were captured by the very businesses they were required to regulate.

The chairperson of the Commodities Futures Trading Commission, for example, exempted important parts

of Enron's business from regulation and, just weeks later, joined Enron' board. It has been the rule,

not an exception, for retired regulators to get jobs as auditors of financial firms and become lobbyists.

Incumbent regulators have difficulty in conducting effective supervision because of intensive lobbying

from their former superiors.

In 1887, Congress passed an act to regulate the US railroad industry. The legislation originated

in the demands of farmers and merchants for protection against the “robber barons”.

Despite this background, railroad interests supported the bill. Charles Adams, president of the

Union Pacific Railroad, explained his reasoning to a sympathetic congressman, John D. Long. “What

is desired,” he wrote, “is something having a good sound, but quite harmless, which will impress

the popular mind with the idea that a great deal is being done, when, in reality, very little is

intended to be done.”

On the whole, he got what he wanted. The Interstate Commerce Commission established by the act

was chaired by a lawyer with experience of the railroad industry – acquired, naturally, by acting

on behalf of his railroad clients. When, a decade later, the Supreme Court ruled that a rate-fixing

agreement between railroads was illegal, the ICC was crestfallen: surely, the commission said, it

should not be unlawful to confer, to achieve what the law enjoins – the setting of just and reasonable

rates. Soon after, Congress approved legislation making it a criminal offence to offer rebates on

tariffs the ICC had approved, and the commission thereafter operated as the manager of a railroad

cartel.

One feature of regulatory capture is that the regulators of an industry start viewing it through

the eyes of its principal actors, and to equate the public interest with the financial stability of

these institutions. Sometimes such capture is clearly corrupt, as when regulators are directly or indirectly

(via revolving door mechanism) are paid by the corporations they oversee. But the truth is that the

largest contributors to congressional campaign funding are financial services industries, pharmaceuticals

and energy. So they, by definition, have substantial political cloud in neoliberal state.

Sometimes the mechanism is more subtle and acts as "adverse selection" : new appointees are screened

as for being "business-friendly", the prerequisite which also smells of corruption.

Greenspan is a nice example of

such political appointee; but Dugan,

Cox (Our

Corrupt Federal Regulator) and many others, who so far managed to escape jail, were equally destructive.

Generally, bureaucratic institutions always try to preserve the problem to which they are the solution.

So efficiency of regulators is always less then desired. In other words there is no, and can never

be in principle, an ideal regulator.

But institutions undermined by political appointees essentially became a turncoats and the

part of the problem, not the part of the solution. In other words from regulators they became enablers

of criminal behavior. As simple as that. All this was done under the smoke screen of

neoliberalism, which starting from

70th became dominant ideology in the USA and elsewhere.

Simon Johnson, an

MIT professor

and former IMF

chief economist has been a critic of the Bush/Obama bailout from the start, but his devastating essay

in the May issue of the Atlantic,

"The Quiet Coup," may

be the clearest explanation of regulatory capture in the USA, the country that became just richer variant

of a classic "banana republic":

Squeezing the oligarchs... is seldom the strategy of choice among emerging-market governments.

Quite the contrary: at the outset of the crisis, the oligarchs are usually among the first to get

extra help from the government, such as preferential access to foreign currency, or maybe a nice

tax break, or — here’s a classic Kremlin bailout technique — the assumption of private debt obligations

by the government.

Under duress, generosity toward old friends takes many innovative forms. Meanwhile, needing

to squeeze someone, most emerging-market governments look first to ordinary working folk—at least

until the riots grow too large.

Simon Johnson says:

So let's say that you have excessive regulation to start with, you bring that down to a sensible

level, and then the guys making a ton of a money use that to undermine sensible regulation.

What he's describing is a "Peter Principle" of economics: in a classic cycle over-regulation is first

reduced to meaningful regulation and then due to growth of influence (and profits) of financial oligarchy

it inevitably reduced to a level of incompetence and at this point seize to effectively regulate the

system. After spectacular crash excessive regulations are reinstalled and cycle starts again.

"Peter Principle" of economics: in a classic cycle over-regulation is first reduced to

meaningful regulation and then due to growth of influence (and profits) of financial oligarchy

it inevitably reduced to a level of incompetence and at this point seize to effectively regulate

the system. After spectacular crash excessive regulations are reinstalled and the cycle starts

again.

Here is relevant quote from Simon Johnson's paper:

The Bailout Proves the Banks Own the Politicians

The bailout proves the banks own the politicians. The only way we will ever get another Teddy

Roosevelt would be to get a wealthy independent elected President who only wants one term and would

use his elected mandate to push his agenda against the corporate power structure.

Here he forgot the possibility of repetition of the destiny of JFK. Also neoliberal ideology (like

Marxism in the past in the USSR and its satellites) "infects" regulators making them organically

unable to perform actions the contradicts it: in this case drastic anti-banks actions. This is a variant

of Cognitive Regulatory Capture

It is interesting to note that the trend toward regulatory capture in the past was recognized by

nobody else as Stalin, who instituted "purges" explicitly to prevent too complacent behaviour of government

bureaucrats who with time forget about the goals of their institutions and are more and more driven

by their own profit and privileges motives. While extremely cruel, this was pretty effective methods

for keeping regulators in check.

An excellent definition of intellectual capture was given by Greenspan in 2009:

"Well, remember that what an ideology is a conceptual framework with the way people deal with

reality. Everyone has one. You have to. To exist, you need an ideology. The question is whether it

is accurate or not. "

That means that independence of regulators is not a panacea. They are influenced by dominant ideology

like everybody else. So intellectual capture is prevalent even among the most nominally independent

regulators, as to live in the society and be free of dominant ideology is very difficult or if want

to be successful impossible. Under neoliberalism that gives rise to a very dangerous view: What’s good

for Wall Street must be great for the real economy. For example independent central banks, will pursue

neoliberal policies if top brass is captured by neoliberal ideology. The regulators may be independent

at first, but if they share the ideology (and in this case this is a neoliberal ideology) they invariably

fall under the spell —one way or another — of the people they are supposed to control.

Here is a pretty telling dialog reproduced in

Democracy Now

REP. HENRY WAXMAN: Dr. Greenspan, you had an ideology, you had a belief, that free,

competitive — and this is your statement: “I do have an ideology. My judgment is that free,

competitive markets are by far the unrivaled way to organize economies. We’ve tried regulation.

None meaningfully worked.” That was your quote.

You had the authority to prevent irresponsible lending practices that led to the subprime mortgage

crisis. You were advised to do so by many others. And now our whole economy is paying its price.

Do you feel that your ideology pushed you to make decisions that you wish you had not made?

ALAN GREENSPAN: Well, remember that what an ideology is a conceptual framework with

the way people deal with reality. Everyone has one. You have to. To exist, you need an ideology.

The question is whether it is accurate or not. And what I’m saying to you is, yes, I’ve found

a flaw. I don’t know how significant or permanent it is, but I’ve been very distressed by that

fact.

But if I may, may I just finish an answer to the question previously posed?

REP. HENRY WAXMAN: You found a flaw in the reality —-

ALAN GREENSPAN: Flaw in the model that I perceived as the critical functioning structure

that defines how the world works, so to speak.

REP. HENRY WAXMAN: In other words, you found that your view of the world, your ideology,

was not right. It was not working.

ALAN GREENSPAN: That it had a -— precisely. No, that’s precisely the reason I was shocked,

because I’ve been going for forty years or more with very considerable evidence that it was working

exceptionally well.

UNIDENTIFIED: I want to thank you on behalf of the committee.

So like Marxists pointed long ago "ideas became a material force, when they capture minds of

people". That means that the virtues of independence become even more questionable once we factor

in the politics. Will an independent regulator or central bank be less prone to political influence

from powerful lobbies? That seems doubtful. In his famous article Simon Johnson tells a an interesting

and pretty surprising at this time

observation: the

U.S. has been afflicted by a version of the crony capitalism that has been the scourge of so many emerging

markets, except that Wall Street has bought its influence and power not by only and exclusively by bribery

but more by financing and shaping the dominant ideology of our times -- neoliberalism (The

Quiet Coup - Simon Johnson - The Atlantic, May 2009).

This process of ideological capture he called a

Quiet coup. Here are some

quotes from Dani Rodriks post (Dani

Rodrik's weblog Simon Johnson's morality tale) which discusses the article and point out some questionable

attribution of wisdom to IMF, which is an institution that is a key part of pushing neoliberalism to

other countries:

In a primitive political system, power is transmitted through violence, or the threat of violence:

military coups, private militias, and so on. In a less primitive system more typical of emerging

markets, power is transmitted via money: bribes, kickbacks, and offshore bank accounts. Although

lobbying and campaign contributions certainly play major roles in the American political system,

old-fashioned corruption—envelopes stuffed with $100 bills—is probably a sideshow today, Jack

Abramoff notwithstanding.

Instead, the American financial industry gained political power by amassing a kind of cultural

capital—a belief system. Once, perhaps, what was good for General Motors was good for the country.

Over the past decade, the attitude took hold that what was good for Wall Street was good for the

country. The banking-and-securities industry has become one of the top contributors to political

campaigns, but at the peak of its influence, it did not have to buy favors the way, for example,

the tobacco companies or military contractors might have to. Instead, it benefited from the fact

that Washington insiders already believed that large financial institutions and free-flowing capital

markets were crucial to America’s position in the world.

The solution, to Simon, is equally clear. Finance needs to be cut down to size. What

the U.S. needs is what the IMF would have told any country:

The challenges the United States faces are familiar territory to the people at the IMF. If

you hid the name of the country and just showed them the numbers, there is no doubt what old IMF

hands would say: nationalize troubled banks and break them up as necessary.

... ... ...

The second problem the U.S. faces — the power of the oligarchy — is just as important as the

immediate crisis of lending. And the advice from the IMF on this front would again be simple:

break the oligarchy.

As with any story built around clear villains easy solutions, there is something in this account

that is quite unsatisfying. For one thing, I think it puts the blame too narrowly on the bankers.

Yes, there can be little doubt that banks badly misjudged the risks they were taking on. But

they were aided in all this by the broader economics and policymaking community -- not because the

latter thought the policies in question were good for bankers, but because they thought these would

be good for the economy. Simon himself says as much. So why pick on the bankers? Surely the blame

must be spread much more widely.

And I find it astonishing that Simon would present the IMF as the voice of wisdom on these

matters--- the same IMF which until recently advocated capital-account liberalization for some of

the poorest countries in the world and which was totally tone deaf when it came to the cost of fiscal

stringency in countries going through similar upheavals (as during the Asian financial crisis).

Intellectual capture can also occur on the level below ideology. Every regulatory agency is dependent

for information on the businesses it regulates. Many of the people who run regulated companies would

be affronted by any suggestion that their activities do not serve the public good. But the truth is

that few members of the public ever make contact with a regulatory agency; almost always, they need

to deal with the professionals from industries they regulate. It does not requires a considerable effort

of imagination to understand that any industry tried to use this leverage. So even the regulator with

the best intentions comes to see issues eventually start to see the issue from the prism of the framework

that was formulated by the corporate officers and professional he deals with on daily basis.. You need

to have pretty abrasive or independent type of personality and considerable intellectual curiosity to

discount this influence. And these are not the qualities often sought, or found, in regulators.

The IMF’s latest working paper —

A Fistful of Dollars: Lobbying and the Financial Crisis (Deniz Igan, Prachi Mishra, and Thierry

Tressel IMF, December 2009) — shows how the powerful mechanism of lobbing created the alliance between

Wall Street and Washington policymakers. In other words it convert social system into corporatism. Like

military industrial complex, financial oligarchy understands pretty well that money spend on lobbing

are money well spend: the most aggressive, the most reckless banks have the

greatest

return in bailout monies.

Lobbyists are an important mechanism for silencing and subverting federal regulators.

Existence of revolving door is a perfect tool for keeping regulators at bay. See Frank Partnoy famous

book

Infectious Greed that explains how and why large scale financial malfeasance happens. And why it

is hardly ever punished. Here is one quote:

"In July 2005, Public Citizen published a report entitled "The Journey from Congress to K Street":

the report analyzed hundreds of lobbyist registration documents filed in compliance with the Lobbying

Disclosure Act and the Foreign Agents Registration Act among other sources. It found that since 1998,

43 percent of the 198 members of Congress who left government to join private life have registered

to lobby.

A similar report from the Center for Responsive Politics found 370 former members were in

the "influence-peddling business", with 285 officially registered as federal lobbyists, and 85 others

who were described as providing "strategic advice" or "public relations" to corporate clients."

Tremendous resources in their disposal permit lobbyists to win the assignment of red state democrats

to the banking committee, so they can get contributions from bankers and serve as Trojan horses which

can break any attempt to reform the system. The IMF had shown that money channeled to lobbyists by banks

naturally impose on the society riskier lending with less supervision and regulation:

“Our analysis establishes that financial intermediaries’ lobbying activities on specific issues

are significantly related to both their mortgage lending behavior and their ex-post performance.

Controlling for unobserved lender and area characteristics as well as changes over time in the macroeconomic

and local conditions, lenders that lobby more intensively (i) originate mortgages with higher loan-to-income

ratios, (ii) securitize a faster growing proportion of loans originated; and (iii) have faster growing

mortgage loan portfolios.”

Our analysis of ex-post performance comprises two pieces of evidence: (i) faster relative growth

of mortgage loans by lobbying lenders is associated with higher ex-post default rates at the MSA

level in 2008; and (ii) lobbying lenders experienced negative abnormal stock returns during the main

events of the financial crisis in 2007 and 2008.”

The authors identify six key goals that bank achieved by spending huge sums of money for lobbying:

Prevent any tightening of lending laws or new laws aimed to reduce the benefits of

short-termist bonus generating strategies

Allow systematic underestimation of default probabilities by overoptimistic bankers;

Not only originate loans that carry more risk, but to convince legislators that such lending

is prudent;

To kill bills directed in tightening of lax lending standards

To restrict entry by others preventing competition;

To increase the probability of receiving preferential treatment in a crisis.

In other word lobbying by banks is a systemically dangerous activity that mimics methods used by organized

crime (and as such falling under RICO statute) that puts the entire society at risk. Any meaningful

actions are now impossible without weakening political influence of the financial industry (the capture

of regulators). Unfortunately, for the same reason it is unlikely to occur . . .

Deregulation has been a big problem in areas of the economy where the beneficiaries of changes in

the law purchased the deregulatory changes from the people who controlled the federal government. And

even if they can't kill regulation they have another tool in their disposal. Budgets is where regulations

are neutered by politicians who did not stop the regulations. Kind of the second line of defense for

financial oligarchy:

Rusty:

Logically, regulations benefit those that have a hand in creating them - politicians and lobbyists

who represent entrenched business interests. Certainly politicians will try with at least lip

service towards some equitable aim in the public interest, but they must work with the entrenched

interests to achieve anything and to maintain power. So it makes sense that often regulations

serve entrenched interests and thereby increase inequality.

ilsm -> Rusty...

I did some consulting work years ago in the transport industry (did an brief excursion from

the military industry complex).

No DoT (FAA, Highways, pipelines, etc) regulation is allowed without support from the industry,

thus we see new regulations discussed after each transport related disaster.

Once a regulation is "set", policies for enforcement are devised by the responsible agency,

which leads to plans for enforcement, then budgets. Budgets is where regulations are neutered

by politicians who did not stop the regulations (keep the gumint off the back of the perps).

See last Sunday's train derailment, or any pipeline explosion.

I worry more about what happens during my colonoscopy, I am much more familiar with neglect

in the aerospace world.

Banking corruption is the foundation of all corruption pyramid. We are used to talking about corruption

at various levels of government, as well as legislative and judicial branches. We also used to facts

of corruption in military-industrial complex, including public procurement. However, in most cases,

the foundation of this corruption pyramid are large banks, without which the implementation of most

of illegal business activities would be impossible.

Here we are talking about the banking corruption -- the fact that banks and other financial institutions

in the context of financial globalization and development of cashless payments have become a major part

of the infrastructure of the shadow economy. And are extremely interested in participation in shady

activities as those provide much better profit margins then legal activities. Without their mediation

and help in money laundering including laundering of criminal assets would be not have the scale it

now has. They are also the central player in organizing illegal export of capital abroad to offshore

jurisdictions, which, in essence, is just another form of money laundering.

However, the media and the economic mainstream try to dismiss this systemic behaviour of major financial

players, creating an image of respectable bankers and respectable businessmen. With few bad apples.

In reality many banks have shadow economy as the major source of their income and are committing illegal

transactions in the financial market necessary for support of both "gray" and "black" economy.

It is clear that large banks in those condition are especially interested in emasculation of regulators

both directly via financing of political campaigns and then forcing the appointment of cronies as heads

of regulatory agencies and indirectly, providing "revolving door" for personnel in regulatory agencies.

Corruption can be more subtle. A politician who looks to a career after political office knows that

big companies can offer lucrative consultancies and directorships, but representing the public interest

does not. Everyone who works in a regulatory agency knows that if they are well regarded in the industry,

they are eligible for jobs in the private sector which are far more rewarding than employment in a public

agency. At this point serving in government office became just a jumpstart for a career in private industry.

And you no longer need to bribe such people. They will be willing accomplices without bribing.

A reader on Naked Vapitalism blog, who has first hand knowledge of some of the major US financial

regulators wrote (Sep 2, 2009 |

nakedcapitalism.com) about the problem with systemic corruption of lawyers who are working in regulatory

agencies. Incentives to switch sides are way too strong and legal prohibitions for such behaviour are

absent:

A reader who has first hand knowledge of some of the major US financial regulators flagged a

CounterPunch article by

Pam Martens as the best discussion of the “revolving door” problem that he had ever seen.

The interesting thing about this article is that it highlights a problem that is not widely recognized

and therefore has no safeguards against it. As our correspondent explains:

The most important aspect of this is that the “revolving door” problem is most acute, not with

the actual regulated firms, but with the professional firms that provide services to regulated

entities, especially law firms (it is also a serious issue with compliance consulting firms,

although that is something of a separate issue.)

One reason for that is that the standards are different for lawyers than for financial professionals.

Financial professionals are forbidden from joining any company they have recently examined; but

lawyers are forbidden only from working on cases they have had contact with –- there are no specific

prohibitions on working for law firms that have cases that they have had contact with, as long

as they don’t work on those cases (as if that could ever be enforced.)

That means that lawyers like Linda Thomsen, who as head of Enforcement would have been

familiar with every case of significance, could go directly to work for a securities law firm

already handling cases which she would most certainly have been familiar with, without Ethics

making so much as a peep. I don’t know how that can be seen as anything other than a serious conflict

of interest.

I strongly disagree with the argument that SEC lawyers have incentives to drop cases to curry

favor with future employers. On the contrary; they have every incentive to break big cases, which

is the stuff that careers are made of. And it is the law firms, not the financial firms, that

will most likely be their future employers.

Where they do have an incentive, however, is to quickly settle those cases; they get credit

for making the case, but the penalties inflicted are not enough to cripple the big Wall Street

firms that (through the law firms they hire) will be the ultimate source of income for the lawyers

after they move into the private sector. If they were to do nothing, they would be seen as incompetent,

and nobody would hire them; but if they do too much, they disrupt the revenue stream that ultimately

feeds the securities law industry.

A key section of the Martens article, which is worth reading in its entirety:

The team that produced this report on one of the most long-running and convoluted frauds [Madoff]

in the history of Wall Street included Inspector General H. David Kotz who came to the SEC-IG

post in December 2007 after five years as Inspector General and Associate General Counsel for

the Peace Corps. The Deputy Inspector General, Noelle Frangipane, also came to the SEC from the

Peace Corps where she had served as Director of Policy and Public Information.

This lack of Wall Street cronyism by the top two in the Inspector General’s office might have

been refreshing to some in Congress and compensated for their not knowing the difference between

puts and calls and peaks and troughs and the intricacies of Mr. Madoff’s split-strike conversion

strategy (he splits with your money while converting you to a pauper). But the background of the

member of the team heading up the Inspector General’s Office of Investigations, J. David Fielder,

should have rang serious alarm bells to Congressional investigators.

For the ten years leading up to July 2007, J. David Fielder worked for the SEC as a Senior

Counsel in the Division of Enforcement. In February 1999, he moved to the Division of Investment

Management, first as Senior Counsel on the Task Force for Adviser Regulation, then as Advisor

to the Director. In November 2000, SEC Chairman, Arthur Levitt, appointed Fielder Counsel to the

Chairman.

In July 2007, Mr. Fielder was invited to join the corporate law firm, Haynes and Boone LLP,

as a partner. In other words, Mr. Fielder’s government issue rolodex filled with the names, home

numbers and email addresses of his colleagues at the SEC along with the investigatory matters

in his head is deemed fungible currency among corporate law firms and can be freely exchanged

for partner status, instantaneously moving one from the lowly wages and attendant lifestyle of

public servant to the rarefied bracket and luxuriant trappings of corporate law firm partner.

But what happened next is where things get interesting. In March 2009, just as the SEC Inspector

General was hot in pursuit of Madoff aiders and abettors, Mr. Fielder gave up his lucrative partner

status at Haynes and Boone to accept the lowly post of Assistant Inspector General of Investigations,

working under a boss from the Peace Corps. In other words, he gave up big bucks for a demotion

at the SEC.

What Mr. Fielder did might not raise alarm bells were it not happening on a regular basis throughout

the corridors of Washington and Wall Street. To understand the implications, this maneuver deserves

an appropriate name. A revolving door is assumed to mean one gets all the right connections as

a public servant and cashes them in to the highest bidder in private industry. That concept doesn’t

typically entertain the door revolving back to public servant status. On Wall Street, they call

a maneuver like that a round trip: you buy 100 shares and eventually sell the same 100 shares.

You end up back where you started: a round trip.

Just how many lawyer round trippers are involved in the Madoff investigation?

Enough to raise a strong stench of circular corruption.

The correspondent may be right about a revolving door, but he is wrong about the ethical rules

governing lawyers. You cannot work against the former client, not just on any cases you had before,

but on any new cases. The client owns your loyalty for the rest of your professional life. The

client can waive some conflicts, but not others.

So: the rules on lawyers are actually much stricter than the person thinks. Yes, you can SOMETIMES

work for a firm that has the other side of a case or deal, provided that you are “chinese walled.”

But that is really not common (probably more common in transactional law than litigation). Few

lawyers and law firms are willing to take the risk of an accusation – these are career ending

events if you were to break the confidence and accidentally share something that hurt the former

client. Also, clients get royally pissed that you affiliated with somebody who works against them.

What the correspondent doesn’t seem to realize is that the stricter rules tend to make you even

more bound to the client because you can tend to be stuck to one large client in fields where

competitors tend to sue each other. So in some fields, like oil and gas, a firm might work for

several majors. In a field like investment banking, not so much.

With deals, companies will have their preferred lawyers and not change much. Also, the more

you move your business around, the more you can block firms from helping your enemies. I have

sometimes suspected that firms went on campaigns to sew up potential opposing counsel.

This is a little simplistic, but the person seems to have an overly negative idea of the ethics

rules under which lawyers operate. Law firms take conflicts checks VERY seriously, as do individual

lawyers. If practices around Wall Street have changed, it is out of necessity. Several investment

banks *used* to be a hundred years old: that is a lot of conflicts history. And you would still

have to get the clients’ consent.

I honestly believe in regulatory capture. But what you ought to ask yourself, perhaps, is how

one can take graduates from the same two or three colleges and business schools, and expect different

thinking from them if they are plopped into different work environments? They are still socializing

with the same bunch educated at the same two schools, still living with those people, working

with those people – but one group is supposed to be policing the other. If you ask me, take a

look at everybody who went to Harvard over the past 25 years, and there is the start of your revolving

door. The “elites” in all fields across the East Coast already have a lot in common before they

start work.

So Felder has been rehired by the SEC after 2 years of orientation by the law firm Haynes and

Boone LLP to become counter intelligence for the Madoff operation back at the SEC? Do we have

an espionage thriller here?

A lawless industry fueled by political and regulatory capture would use more than just a few

tools perfected by military and criminal organizations for covert activities.

I’m looking forward to an expose of the finance industry’s private investigation and para military

organization hires with their personnel migration patterns.

DownSouth, September 2, 2009 at 7:43 am

Yves,

Reforming the polity at this point is more important than reforming the economy. If we attempt

economic reform before political reform is accomplished, we’re just going to wind up with more

disasters like the 2003 drug benefit for the elderly or the recent (and ongoing) bank bailout.

What with Obama’s backroom deals with BigPharma that we already know about, plus heaven knows

what else we don’t know about, the more astute observer can already see where healthcare reform

is headed–huge benefits to powerful insiders, little benefit to the general good and huge cost

to taxpayers.

I notice this post, along with a couple of other recent posts dealing with the Fourth Estate

http://en.wikipedia.org/wiki/Fourth_Estate , deal more with political reform than with economic

reform. I believe this is key, and I salute your efforts, as I am convinced that substantive economic

reform is impossible without first achieving political reform.

The most radical creed of the American Revolution was that of the separation of Church and

State. As Daniel Yankelovich put it, “the enemy was entrenched inherited privilege embodied in

the church and in most branches of European royalty in collusion with each other.” Granted, the

revolution was nominally against the British monarchy, but the Founding Fathers were acutely aware

that the monarchy and the church were so inextricably interwoven as to be all but one and the

same.

Today we face a similar problem, but instead of an unholy alliance between church and state,

we have an equally pernicious alliance between major business corporations and state.

The first American revolution institutionalized the separation of church and state. I think

we need a second American revolution that promulgates separation of big business and state.

You’ve already posted on a couple of the problem areas that require reform before the deathgrip

that big business enjoys on the polity can be loosened. Let me repeat those and add a couple more

(this is not meant to be a complete list):

• The Fourth Estate (the press, media)

• The Revolving Door

• Campaign Finance

• The Academe (and here I’m not just talking about the aberrant economics departments and their

capture by business interests, but the equally perverse Nobel prize committee)

jake chase, September 2, 2009 at 1:05 pm

The truth about the SEC is not intuitive. One must have worked there as I did forty years

ago (when, allegedly, it WAS enforcement minded) to understand that teh agency is a small army

of bureaucrats who are simply biding their time either until retirement or escape to lucrative

private practice. To the extent any enforcement takes place, it is directed against a fringle

element of tin horn promoters, penny stock floggers, arrant confidence men whose pitches are so

transparently idiotic that anyone falling for them really has only himself to blame. As for the

top tier finaglers, they are strictly off limits. When a white shoe firm has a client with a problem,

he calls the man at the top of the enforcement chain, who instructs the juniors accordingly.

Instead of this regulation tapdance, what we need to enforce honesty in business is integrity

in the legal system. Unfortunately, we have defendant oriented federal judges who are universally

hostile to shareholder interests, as well as state regulation which insulates management against

liability in order to pile up franchise fees. Delaware is the leading culprit in this regard.

The Congress could solve this problem by insisting upon federal charters for publicly traded corporations.

They never will because the corporations will never permit it.

It looks like the USA is repeating all the mistake that were made in early XX century on a new level.

During the 19th century, Washington was generally happy to do favors for Wall Street financiers. Railroad

tycoons, who often used those railroads as vehicles of extravagant speculation, enjoyed subsidies, tax

exemptions, loans, and a whole smorgasbord of financial fringe benefits supplied by pliable congressmen

and senators (not to mention armadas of state and local officials).

But in 19th century when panic struck, the mighty, as well as the meek, went down with the ship.

Washington felt no obligation to rush to the rescue. And there was blood on the floor.

By early in the 20th century, however, the savage anarchy of the financial marketplace had been at

least partially domesticated under the reign of the greatest financier of them all, J P Morgan. Ever

since the panic of 1907, the legend of Morgan's heroics in single-handedly stopping a meltdown that

threatened to become worldwide, the iron discipline he imposed on more timorous bankers, has been told

and re-told each time an analogous implosion looms. Back then, with Morgan performing his role as the

nation's unofficial private central banker, president Teddy Roosevelt's administration continued to

keep its distance from Wall Street, still unready to offer salvation to desperate financial oligarchs.

Not normally sympathetic to Morgan and his crowd, Roosevelt did cheer from the sidelines as the uber-banker

performed his rescue operation.

As it turned out, though, the days of Washington agnosticism about Wall Street were numbered. The

economy had become too complex and delicate a mechanism and, in 1907, had come far too close to meltdown

- even Morgan's efforts couldn't prevent several years of recession -- to leave financial matters entirely

in the hands of the private sector. That's why Federal Reserve was established in 1913 under president

Woodrow Wilson as a quasi-public authority meant to regulate the country's credit markets -- albeit

one heavily influenced the country's principal bankers. That worked well enough until the Great Crash

of 1929 and the Great Depression that followed and lasted until World War II.

President Franklin D Roosevelt's New Deal did, as a start, engage in some bail-out operations. The

Reconstruction Finance Corporation, actually created by president Herbert Hoover, continued to rescue

major railroads and other key businesses, while some of the New Deal's efforts to help homeowners also

rewarded real estate interests. The main emphasis, however, switched to regulation. The Glass-Steagall

Banking Act, the two laws of 1933 and 1934 regulating the stock exchange, the creation of the Securities

and Exchange Commission, and other similar measures subjected the financial sector to fairly rigorous

public supervision.

Actually, while Reagan administration get its due as as an initiator of the deregulatory binge,

Clinton administration role in deregulation

is often underestimated. For all practical purposes the OTC derivative dealers could be classified as

RICO criminal enterprises since the early nineties. Frank Partnoy’s book,

Infectious Greed provides an excellent summary up through 2002. Scot Griffin in his comment to

“Wake

Up, Gentlemen” ( The Baseline Scenario, Dec 15, 2009 noted:

The explanation for the perceived “flaw” is the recognition of the existence of regulatory capture.

That is, the regulators were captured by the very businesses they were required to regulate.

The regulators were puppets on a string dancing to the tune of the financial innovators. There was

no separate regulatory innovation. It was lock-step by design.

Now, let’s assume there was no regulatory capture. What was the motivation for “regulatory

innovation?” The answer is GDP growth.

There’s an argument that “It’s the economy, stupid!” the meme spawned by the first Clinton campaign,

has had adverse consequences on the long term health of the economy by focusing government officials

and regulators on an arbitrarily short cycle (e.g., 2 to 4 years) just as public corporations are.

Again, extending the analogy (started above) of U.S. government as corporation, the voters are shareholders

and they vote based on earnings growth. If you recognize that a lot of members of government have

been involved in managing public corporations, it is easy to see how they can get caught up in this

mentality.

Of course, one might argue correctly that this short-term focus existed long before Clinton.

New Deal lasted for at least two political generations. When it was dismantles, the USA was on the

sure path to step on the same rake again and again. And sure it stepped. Financial crisis of 2008 was

a significant blow, that almost killed the American empire and set back the political influence of the

USA almost to pre-WWII levels. The USA found itself almost in the USSR shoes when, like happened with

communism in the USSR, the dominant ideology --

neoliberalism -- became a subject

of nasty jokes.

In 2008 Wall Street, despite all the efforts of financial oligarchy, had been convicted in the court

of public opinion of reckless, incompetent, self-interested, even felonious behavior with consequences

so devastating for the rest of the country that government was licensed to make sure it didn't happen

again.

In 2008 Wall Street, despite all the efforts of financial oligarchy, had been convicted

in the court of public opinion of reckless, incompetent, self-interested, even felonious behavior

with consequences so devastating for the rest of the country that government was licensed to make

sure it didn't happen again.

Luckily for Wall Street, the financial oligarchy managed to replace Bush II with its Democratic copycat,

right of the center senator Obama. Control of both Congress and presidency allowed them to avoid legal

consequences of their actions.

But it is clear to everybody with IQ above 100 that the undoing of that New Deal regulatory regime,

and its replacement, largely under Republican administrations (although Glass-Steagall was repealed

on Bill Clinton's watch), with what some have called the "socialization of risk" has contributed in

a major way to the mess we're in today.

Financial sector hypertrophy in the USA, while providing illusion of growth of GDP led to decimation

of real economy, which has slipped into a coma as our resources and talents have gone into enriching

the well-connected financiers. Jobless recoveries are natural side effect of this story. As Volker noted:

“I have found very little evidence that vast amounts of innovation in financial markets in recent

years have had a visible effect on the productivity of the economy”.

In reality it was worse then Volker admitted. "Innovation" in the financial industry has had a negative

effect on productivity because it sucks available investment money from socially productive, job creating

sectors of the economy such as manufacturing. Another point is the intellectual capital “lost” to financial

services. The outsize compensation has moved the best and the brightest to Wall Street, although you

can argue whether they were really best and brightest based on the disastrous results of their activities.

But the fact that physicians were leaving medicine for finance as well as physicists moving to hedge

funds are undisputable.

Neoliberal regime that was established

in the USA in early 80th made the country legal framework (shredding New Deal regulations) and government

behavior (corrupt administrations of Clinton and Bush II) extremely comfortable for financial oligarchy.

Beginning with the massive bail-out of the savings and loan industry in the late 1980s, Washington committed

itself, at least under conditions of acute crisis, to the policy of off-loading the risks taken by major

financial institutions, no matter how irrationally speculative and wasteful, onto the backs of the American

taxpaying public.

Beginning with the massive bail-out of the savings and loan industry in the late 1980s,

Washington committed itself, at least under conditions of acute crisis, to off-loading the risks

taken by major financial institutions, no matter how irrationally speculative and wasteful, onto

the backs of the American taxpaying public.

Despite free market/anti-big-government rhetoric, real-life Washington has tacitly acknowledged

the degree to which our national economy has become dependent on the financial sector (finance,

insurance and real estate - or FIRE). And it will do whatever it takes to keep it afloat. The "socialization

of risk" was accompanied by the "privatization of reward". This applies not only to particular institutions

like Bear Stearns, or even to mortgage mega-firms like Fannie and Freddie, but to finance in general.

When it seemed necessary, public monies were indeed funneled in the general direction of the banking/brokerage

community to shore up the whole rickety structure. This allowed one burst bubble -- the dot-com debacle

-- to be replaced by another, namely mortgage/collaterized-debt-obligation bubble. Blowing bubbles became

substitute for real economy growth.

Backstopping the present bail-out is American taxpayer. Even while Washington was instituting the

periodic "socialization" of bad debts, it was systematically abandoning the New Deal's commitment to

regulation. That, of course, was in the very period when financial markets became more arcane due to

introduction of computers.

It's time for a reversal of course. Stringent re-regulation of FIRE is not enough any more. Washington's

mission may, at this late date, be an even more complex one than Roosevelt's faced when instituting

New Deal. The government must figure out how to deploy its power to shift the flow of investment capital

out of the minefields of speculative paper transactions back into productive channels. The attempt to

ride the country of speculative activities of Wall Street, based on the role of dollar as the world

reserve currency will fail. The country is just too big to be fed from this activities, and the other

players will not be passive for long. Signs of activity in the direction of weakening of dollar role

on international arena are visible both in Europe (despite its satellite status) and BRICS.

"I believe that the fraudulent nature of the GWOT (Global War on Terror)

should be a key ingredient of any analysis of our political situation and it should be looked

at as a part of the massive financial fraud of that period–the two are not separate. "

Current situation does not raise much hope. Looks like corruption of regulators will continue as

a firmly established practice. As if it is a goal of the government to support it.

There is overwhelming evidence that those charged with regulating our financial system are simply

in the bag of financial oligarchy, including our three most recent Presidents, nearly all Senators and

Congressmen, as well as all prominent officials of the SEC, CFTC, Treasury Dept, Federal Reserve, and

Agencies. All those revolving doors personalities. There appear to be individual exceptions (Ron

Paul, Bernie Sanders), but they just

confirm the rule.

Preserving regulatory capture seems to be one issue about which both parties are in complete agreement.

Adopted after 2008 reforms are simply lipstick on the pig. The corruption is so deeply ingrained that

no public official can be trusted to tell the truth about nation's real financial situation.

What will happen next? Nobody knows. But 401K investors had better understand this level of uncertainty,

if not act on it, since now the safer an investment is advertized, the riskier it is likely turn to

be. Recent bubble and then crash in TIPs is one telling example.

I think that due to systemic corruption of regulators stars are aligned against the US recovery,

whatever it mean. As one commenter

Econbrowser

blog noted it might make sense to put money on the long term stagnation, Japanese style:

"The game is market manipulation to dilute the Hoi Polloi's credit holdings via interest rates

below inflation. It is the same game as was played from the mid-1930's until the early 70's."

Tesla Inc Chief Executive Elon Musk said on Tuesday the U.S. Securities and Exchange Commission was an important watchdog for

investors but questioned why it was not more proactive against the growth of listed blank-check companies.

"They have an important role to play in protecting the public from getting swindled, but are sometimes too close to Wall St hedge

funds imo (in my opinion)," Musk said on Twitter.

"Strange that they aren't taking more action on some of the SPACs (special purpose acquisition companies)," he added.

Reuters reported earlier on Tuesday that the SEC is considering new guidance to rein in growth projections made by SPACs, or listed

blank-check companies, including clarification of when they qualify for certain legal protections. That would extend an SEC crackdown

on a deal frenzy in SPACs, which the regulator worries is putting investors at risk.

Musk has had his own run-ins with the SEC. He reached a settlement with the regulator after he tweeted in August 2018 that he

had "funding secured" to potentially take Tesla private in a $72 billion transaction. In reality, Musk was not close to acquiring

funding.

"... In the Risk Alert below, the itemization of various forms of abuses, such as the many ways private equity firms parcel out interests in the businesses they buy among various funds and insiders to their, as opposed to investors' benefit, alone should give pause. And the lengthy discussion of these conflicts does suggest the SEC has learned something over the years. Experts who dealt with the agency in its early years of examining private equity firms found the examiners allergic to considering, much the less pursuing, complex abuses. ..."

"... Undermining legislative intent of new supervisory authority the SEC never embraced its new responsibilities to ride herd on private equity and hedge funds. ..."

"... The agency is operating in such a cozy manner with private equity firms that as one investor described it: It's like FBI sitting down with the Mafia to tell them each year, "Don't cross these lines because that's what we are focusing on." ..."

"... Advisers charged private fund clients for expenses that were not permitted by the relevant fund operating agreements, such as adviser-related expenses like salaries of adviser personnel, compliance, regulatory filings, and office expenses, thereby causing investors to overpay expenses ..."

"... Current SEC chairman Jay Clayton came from Sullivan & Cromwell, bringing with him Steven Peikin as co-head of enforcement. And the Clayton SEC looks to have accomplished the impressive task of being even weaker on enforcement than Mary Jo White. ..."

"... On the same side though, fraud is a criminal offence, and it's SEC's duty to prosecute. And I believe that a lot of what PE engage in would happily fall under fraud, if SEC really wanted. ..."

"... Crimogenic: Producing or tending to produce crime or criminality. An additional factor is that, in the main, the criminals do not take their money and leave the gaming tables but pour it back in and the crime metastasizes. AKA, Kleptocracy. ..."

"... You might add that the threat of consequences for these crimes makes the criminals extremely motivated to elect officials who will not prosecute them (e.g. Obama). They're not running for office, they're avoiding incarceration. ..."

"... Andrew Levitt, for instance, complained bitterly that Joe Lieberman would regularly threaten to cut the SEC's budget for allegedly being too aggressive about enforcement. Lieberman was the Senator from Hedgistan. ..."

"... More banana republic level grift. What happens when investors figure out they can't believe anything they are told? ..."

"... Can we come up with a better descriptor for "private equity"? I suggest "billionaire looters". ..."

"... Where is the SEC when Bain Capital (Romney) wipes out Toys-R-Us and Dianne Feinstein's husband Richard Blum wipes out Payless Shoes. They gain control of the companies, pile on massive debt and take the proceeds of the loan, and they know the company cannot service the loan and a BK is around the corner. ..."

"... Thousands lose their jobs. And this is legal? And we also lost Glass-Steagal and legalized stock buy-backs. The Elite are screwing the people. It's Socialism for the Rich, the Politicians and Govt Employees and Feudalism for the rest of us. ..."

We've embedded an SEC Risk Alert on private equity abuses at the end of this post. 1 What is remarkable about this

document is that it contains a far longer and more detailed list of private abuses than the SEC flagged in its initial round of examinations

of private equity firms in 2014 and 2015. Those examinations occurred in parallel with groundbreaking exposes by Gretchen Morgenson

at the New York Times and Mark Maremont in the Wall Street Journal.

At least some of the SEC enforcement actions in that era look

to have been triggered by the press effectively getting ahead of the SEC. And the SEC even admitted the misconduct was more common

at the most prominent firms.

Yet despite front-page articles on private equity abuses, the SEC engaged in wet noodle lashings. Its pattern was to file only

one major enforcement action over a particular abuse. Even then, the SEC went to some lengths to spread the filings out among the

biggest firms. That meant it was pointedly engaging in selective enforcement, punishing only "poster child" examples and letting

other firms who'd engaged in precisely the same abuses get off scot free.

The very fact of this Risk Alert is an admission of failure by the SEC. It indicates that the misconduct it highlighted five years

ago continues and if anything is even more pervasive than in the 2014-2015 era. It also confirms that its oft-stated premise then,

that the abuses it found then had somehow been made by firms with integrity that would of course clean up their acts, and that now-better-informed

investors would also be more vigilant and would crack down on misconduct, was laughably false.

In particular, the second section of the Risk Alert, on Fees and Expenses (starting on page 4) describes how fund managers are

charging inflated or unwarranted fees and expenses. In any other line of work, this would be called theft. Yet all the SEC is willing

to do is publish a Risk Alert, rather than impose fines as well as require disgorgements?

The SEC's Abject Failure

In the Risk Alert below, the itemization of various forms of abuses, such as the many ways private equity firms parcel out interests

in the businesses they buy among various funds and insiders to their, as opposed to investors' benefit, alone should give pause.

And the lengthy discussion of these conflicts does suggest the SEC has learned something over the years. Experts who dealt with the

agency in its early years of examining private equity firms found the examiners allergic to considering, much the less pursuing,

complex abuses.

Undermining legislative intent of new supervisory authority the SEC never embraced its new responsibilities to ride herd on

private equity and hedge funds.

The SEC has long maintained a division between the retail investors and so-called "accredited investors" who by virtue of having

higher net worths and investment portfolios, are treated by the agency as able to afford to lose more money. The justification is

that richer means more sophisticated. But as anyone who is a manager for a top sports professional or entertainer, that is often

not the case. And as we've seen, that goes double for public pension funds.

Starting with the era of Clinton appointee Arthur Levitt, the agency has taken the view that it is in the business of defending

presumed-to-be-hapless retail investors and has left "accredited investor" and most of all, institutional investors, on their own.

This was a policy decision by the agency when deregulation was venerated; there was no statutory basis for this change in priorities.

Congress tasked the SEC with supervising the fund management activities of private equity funds with over $150 million in assets

under management. All of their investors are accredited investors. In other words, Congress mandated the SEC to make sure these firms

complied with relevant laws as well as making adequate disclosures of what they were going to do with the money entrusted to them.

Saying one thing in the investor contracts and doing another is a vastly worse breach than misrepresentations in marketing materials,

yet the SEC acted as if slap-on-the-wrist-level enforcement was adequate.

We made fun when thirteen prominent public pension fund trustees wrote the SEC asking for them to force greater transparency of

private equity fees and costs. The agency's position effectively was "You are grownups. No one is holding a gun to your head to make

these investments. If you don't like the terms, walk away." They might have done better if they could have positioned their demand

as consistent with the new Dodd Frank oversight requirements.

Actively covering up for bad conduct . In 2014, the SEC started working at giving malfeasance a free pass. Specifically, the SEC

told private equity firms that they could continue their abuses if they 'fessed up in their annual disclosure filings, the so-called

Form ADV. The term of art is "enhanced disclosure". Since when are contracts like confession, that if you admit to a breach, all

is forgiven? Only in the topsy-turvy world of SEC enforcement.

The agency is operating in such a cozy manner with private equity firms that as one investor described it: It's like FBI sitting down with the Mafia to tell them each year, "Don't cross these lines because that's what we are focusing

on."

Specifically, as we indicated, the SEC was giving advanced warning of the issues it would focus on in its upcoming exams, in order

to give investment managers the time to get their stories together and purge files. And rather than view its periodic exams as being

designed to make sure private equity firms comply with the law and their representations, the agency views them as "cooperative"

exercises! Misconduct is assumed to be the result of misunderstanding and error, and not design.

It's pretty hard to see conduct like this, from the SEC's Risk Alert, as being an accident:

Advisers charged private fund clients for expenses that were not permitted by the relevant fund operating agreements, such

as adviser-related expenses like salaries of adviser personnel, compliance, regulatory filings, and office expenses, thereby causing

investors to overpay expenses

The staff observed private fund advisers that did not value client assets in accordance with their valuation processes or in

accordance with disclosures to clients (such as that the assets would be valued in accordance with GAAP). In some cases, the staff

observed that this failure to value a private fund's holdings in accordance with the disclosed valuation process led to overcharging

management fees and carried interest because such fees were based on inappropriately overvalued holdings .

Advisers failed to apply or calculate management fee offsets in accordance with disclosures and therefore caused investors

to overpay management fees.

We're highlighting this skimming simply because it is easier for laypeople to understand than some of the other types of cheating

the SEC described. Even so, industry insiders and investors complained that the description of the misconduct in this Risk Alert

was too general to give them enough of a roadmap to look for it at particular funds.

Ignoring how investors continue to be fleeced . The SEC's list includes every abuse it sanctioned or mentioned in the 2014 to

2015 period, including undisclosed termination of monitoring fees, failure to disclose that investors were paying for "senior advisers/operating

partners," fraudulent charges, overcharging for services provided by affiliated companies, plus lots of types of bad-faith conduct

on fund restructurings and allocations of fees and expenses on transactions allocated across funds.

The SEC assumed institutional investors would insist on better conduct once they were informed that they'd been had. In reality,

not only did private equity investors fail to demand better, they accepted new fund agreements that described the sort of objectionable

behavior they'd been engaging in. Remember, the big requirement in SEC land is disclosure. So if a fund manager says he might do

Bad Things and then proceeds accordingly, the investor can't complain about not having been warned.

Moreover, the SEC's very long list of bad acts says the industry is continuing to misbehave even after it has defined deviancy

down via more permissive limited partnership agreements!

Why This Risk Alert Now?

Keep in mind what a Risk Alert is and isn't. The best way to conceptualize it is as a press release from the SEC's Office of Compliance

Inspections and Examinations. It does not have any legal or regulatory force. Risk Alerts are not even considered to be SEC official

views. They are strictly the product of OCIE staff.

On the first page of this Risk Alert, the OCIE blandly states that:

This Risk Alert is intended to assist private fund advisers in reviewing and enhancing their compliance programs, and also

to provide investors with information concerning private fund adviser deficiencies.

Cutely, footnotes point out that not everyone examined got a deficiency letter (!!!), that the SEC has taken enforcement actions

on "many" of the abuses described in the Risk Alert, yet "OCIE continues to observe some of these practices during examinations."

Several of our contacts who met in person with the SEC to discuss private equity grifting back in 2014-2015 pressed the agency

to issue a Risk Alert as a way of underscoring the seriousness of the issues it was unearthing. The staffers demurred then.

In fairness, the SEC may have regarded a Risk Alert as having the potential to undermine its not-completed enforcement actions.

But why not publish one afterwards, particularly since the intent then had clearly been to single out prominent examples of particular

types of misconduct, rather than tackle it systematically? 2

So why is the OCIE stepping out a bit now? The most likely reason is as an effort to compensate for the lack of enforcement actions.

Recall that all the OCIE can do is refer a case to the Enforcement Division; it's their call as to whether or not to take it up.

The SEC looks to have institutionalized the practice of borrowing lawyers from prominent firms. Mary Jo White of Debevoise brought

Andrew Ceresney with her from Debeviose to be her head of enforcement. Both returned to Debevoise.

Current SEC chairman Jay Clayton came from Sullivan & Cromwell, bringing with him Steven Peikin as co-head of enforcement. And

the Clayton SEC looks to have accomplished the impressive task of being even weaker on enforcement than Mary Jo White. Clayton made

clear his focus was on "mom and pop" investors, meaning he chose to overlook much more consequential abuses by private equity firms

and hedgies. The New York Times determined that the average amount of SEC fines against corporate perps fell markedly in 2018 compared

to the final 20 months of the Obama Administration. The SEC since then levied $1 billion fine against the Woodbridge Group of Companies

and its one-time owner for running a Ponzi scheme that fleeced over 8,400, so that would bring the average penalty up a bit. But

it still confirms that Clayton is concerned about small fry, and not deeper but just as pickable pockets.

David Sirota argues that the OCIE

was out to embarrass Clayton and sabotage what Sirota depicted as an SEC initiative to let retail investors invest in private equity.

Sirota appears to have missed that that horse has left the barn and is in the next county, and the SEC had squat to do with it.

The overwhelming majority of retail funds is not in discretionary accounts but in retirement accounts, overwhelmingly 401(k)s.

And it is the Department of Labor, which regulates ERISA plans, and not the SEC, that decides what those go and no go zones are.

The DoL has already green-lighted allowing large swathes of 401(k) funds to include private equity holdings.

From a post earlier this month :

Until now, regulations have kept private equity out of the retail market by prohibiting managers from accepting capital from

individuals who lack significant net worth.

Moreover, even though Sirota pointed out that Clayton had spoken out in favor of allowing retail investors more access to private

equity investments, the proposed regulation on the definition of accredited investors in fact not only does not lower income or net