"Minsky's financial instability hypothesis depends critically on what amounts to a sociological insight. People change

their minds about taking risks. They don't make a one-time rational judgment about debt use and stock market exposure and stick

to it. Instead, they change their minds over time. And history is quite clear about how they change their minds.

The longer the good times endure, the more people begin to see wisdom in risky strategies."

The Cost of Capitalism: Understanding Market Mayhem and Stabilizing our Economic Future, by

Robert Barbera

The flaw with Capitalism is that it creates its own positive feedback loop, snowballing to the point where the accumulation

of wealth and power hurts people � eventually even those at the top of the food chain. �

Banks are a clear case of market failure and their employees at the senior level have basically become the biggest bank

robbers of all time. As for basing pay on current revenues and not profits over extended periods of time, then that is

a clear case of market failure --

The banksters have been able to sell the �talent� myth to justify their outsized pay because they are the only ones

able to deliver the type of GDP growth the U.S. economy needs in the short term, even if that kills the U.S. economy in the long

term. You�ll be gone, I�ll be gone.

Unfortunately, many countries go broke pursuing war, if not financially, then morally (are the two different? � this post

suggests otherwise).

I occurs to me that the U.S. is also in that flock; interventions justified by grand cause built on fallacy,

the alpha and omega of failure. Is the financial apparatchik (or Nomenklatura, a term I like which, as many from the Soviet era,

succinctly describes aspects of our situation today) fated also to the trash heap, despite the best efforts of the Man of the

hour, Ben Bernanke?

Minsky moment is the synonym of financial crisis -- the moment when excessive leverage that was inevitably created by the financial

system during the boom phase of the cycle, starts collapsing and financial system enter the state of deep crisis with many banks becoming

insolvent due to the level of leverage they accumulated.

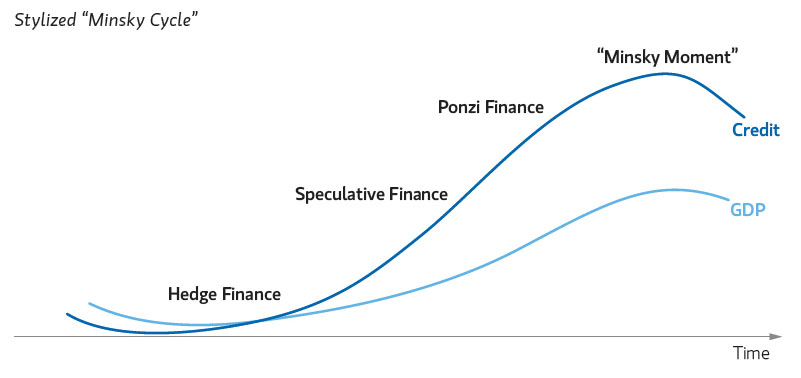

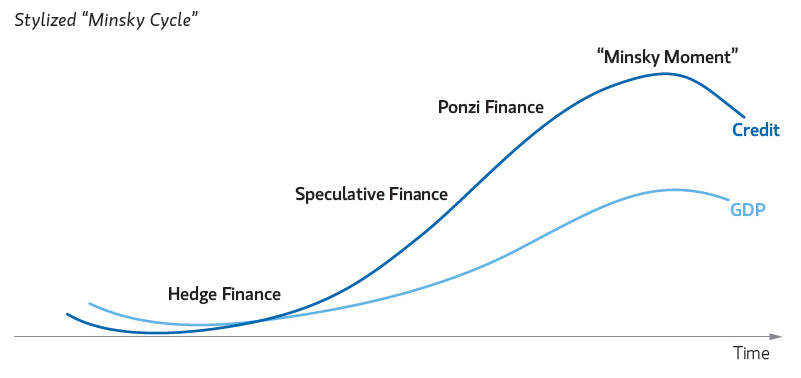

The cornerstone of Hyman Minsky's work is the concept of systemic instability. This notions is well researched in the

theory of autoregulation in the context of the stability of systems with the positive and negative feedback loop. Minsky

argued that system dynamics inherent to capitalism breed fragility and crisis, as stability stimulate the emergence and success of

more risky behaviors of financial players, and such risky behavior eventually leads to the financial crash. In this sense as he put

it: "stability is destabilizing" (Minsky 1985).

Instability is typical for any system with the positive feedback loop. And investment banks and other financial

institutions provide positive feedback loop for financial system in general and stock market in particular making periodic crashes

inevitable, just a side effect of their existence.

But like in

any complex system financial system has its share of nuances which general theory of auto regulation does not address and

Minsky theory addresses. The key idea of Minsky theory is that the behavior of key players in the market after the crash

gradually changes from cautious to

reckless. He introduced the three stages of this transformation which he called hedge finance, speculative finance, and

Ponzi finance. Those stages can be compared to a fully amortizing mortgage, an interest only mortgage, and a negative amortization

mortgage. They indicate the relative difficulties that economic units have in repaying their debt. Minsky defines them as

following:

Hedge finance. Sound phase of the cycle, where �cash flows are expected to exceed the cash flow commitments on

liabilities for every period.� Debts can be paid.

Speculative finance. Less sound �speculative finance� - where cash flows, although inadequate to fully service debt in

the short-run, are generally sufficient over the longer-term.

Ponzi finance. �The economics of euphoria�: unsound, manic prize chasing phase with excessive leverage and

corresponding inability to pay the debt, immediately preceding the crash. At this stage as Minsky pointed out �political

leaders and official economists announced that the economic system had entered upon a new era that was to be characterized by the

end of the business cycle�" Importantly, �a �Ponzi� finance unit must increase its outstanding debt in order to meet

its financial obligations.� New money and credit are a necessity for perpetuating the game, so the collapse comes due to

excessive leverage, when further attempts to increase the debt fail (which for companies often results in margin call):

�The shift toward speculative and even Ponzi finance is evident in the financial statistics of the United States as

collected in the Flow of Funds accounts. The movement to �bought money� by large multinational banks throughout the world is

evidence that there are degrees of speculative finance: all banks engage in speculative finance but some banks are more

speculative than others. Only a thorough cash flow analysis of an economy can indicate the extent to which finance is

speculative and where the critical point at which the ability to meet contractual commitments can break down is located.�

�The theory developed here argues that the structural characteristics of the financial system change during periods of

prolonged expansion and economic boom and that these changes cumulate to decrease the domain of stability of the system. Thus,

after an expansion has been in progress for some time, an event that is not of unusual size or duration can trigger a sharp

financial reaction. Displacements may be the result of system behavior or human error. Once the sharp financial reaction

occurs, institutional deficiencies will be evident.�

�Financial institutions are simultaneously demanders in one and suppliers in another set of financial markets. Once

euphoria sets in, they accept liability structures � their own and those of borrowers � that, in a more sober expectational

climate, they would have rejected�The shift to euphoria increases the willingness of financial institutions to acquire assets

by engaging in liquidity-decreasing portfolio transformations�The result is a combination of cash flow commitments inherited

from the burst of euphoria and of cash flow receipts based upon lower-than-expected income.�

Minsky suggested that if hedge financing dominates, then the economy may well behave close to an equilibrium-seeking system

typical for systems with negative feedback loop. Conversely, the greater the weight of speculative and Ponzi finance, the greater

the likelihood that the economy enters a "deviation-amplifying" mode (which means the system with positive feedback loop). This was

a new discovery different from Marx analysis of the sources of instability in capitalist economics, and Minsky deserves full credit for this discovery.

Often bursting of the bubble happens due to the sudden rise of long term interest rates. Quoting Minsky,

�the rise in long term interest rates and the decline in expected profits play particular havoc with Ponzi units, for the

present value of the hoped for future bonanza falls sharply.�

�It can be shown that if hedge financing dominates, then the economy may well be an equilibrium seeking and containing system.

In contrast, the greater the weight of speculative and Ponzi finance, the greater the likelihood that the economy is a deviation

amplifying system�Over a protracted period of good times, capitalist economies tend to move from a financial structure dominated

by hedge finance units to a structure in which there is large weight to units engaged in speculative and Ponzi finance.�

At the end financial crisis strikes wiping a lot of capital. Government bailout of financial institutions under neoliberalism follows

(because as Senator Durbin noted "banks own the place" -- the Congress) and then overhand of excessive debt depress the economy

and it enters

the stage of prolonged stagnation. Which in modern USA was smoothed by the status dollar as the world reserve currency which allow the USA export inflation. Still stagnation is what we have after 2008. And events of 2020-2021

(coronavirus recession and subsequent stock bubble, which reminds dot-com bubble and which might or might not burst in 2021-2022) are just continuation, the second or

even the third act of the same drama.

The view developed in this volume identifies both real and financial causes for the Great Recession, including the real income

stagnation suffered by households across most of the income distribution on one hand, and deregulation and institutional change in

the financial sector on the other.

The interplay of these factors led to massive debt accumulation, particularly by U.S. households seeking to supplement stagnant

incomes in their pursuit of increasing consumption aspirations. Household borrowing was spurred on by a financial sector rendered

ever freer of inter- and postwar financial regulations. These regulations came to be seen as unnecessary fetters on an inherently

self-regulating �free market,� an idealized notion in which financiers and policy makers placed increasing trust and confidence.

Ultimately, the self-reinforcing developments in the real and financial sectors proved deadly.

Minsky should be the most admired economist in the second half of the 21st. Century. His views are now partially accepted even by

neoclassical economists with their stochastic equilibrium of supply and demand nonsense. This is mainly because they have

no other choice. But Minsky was more than an astute researcher of business cycle and the Great Depression. Perhaps his writings on eradicating

poverty will earn the respect that it may deserve with time as well.

Financialization is inherent in capitalism and is the key to its instability. Minsk considered the rising of private

debt to GDP ratio an immanent feature of capitalism that lead to financial crisis. The idea of Minsky moment is related to the

fact that the fractional reserve banking periodically causes credit collapse when the leveraged credit expansion goes into

reverse.

In any case he was one of the first researchers who understood (after Keynes) that financialization is inherent in capitalism and

is the key to its instability:

�Capitalism is essentially a financial system, and the peculiar behavioral attributes of a capitalist economy center around

the impact of finance upon system behavior.� Minsky (1967)

Fifty years ago, Minsky, following Marx, viewed instability as the central flaw of the financial system under capitalism, as its

inherent flaw. But unlike Marx, who thought that the periodic crisis of overproduction is the source of instability (as well as

impoverishment of workers), Minsky assumed that the key source of that instability is continued in the cycles of business borrowing and fractional

bank lending, when "good times" lead to excessive borrowing and overproduction as well as rampant and increasing

until the financial crash financial speculation, fueled by the stability of the previous period and growing leverage,

which such stability makes possible (The

Alternative To Neoliberalism )

Minsky on capitalism:

He followed Marx stating that "capitalism is inherently flawed, being prone to booms, crises and depressions.

This instability is due to characteristics the financial system must possess and will inevitably acquire, if it is to

be consistent with full-blown capitalism.

Such a financial system will be capable of both generating signals that induce an accelerating desire to invest and of financing

that accelerating investment." (Minsky 1969b: 224)

�The natural starting place for analyzing the relation between debt and income is to take an economy with a cyclical past

that is now doing well.

The inherited debt reflects the history of the economy, which includes a period in the not too distant past in which the economy

did not do well.

Acceptable liability structures are based upon some margin of safety so that expected cash flows, even in periods when the

economy is not doing well, will cover contractual debt payments.

As the period over which the economy does well lengthens, two things become evident in board rooms. Existing debts are easily

validated and units that were heavily in debt prospered; it paid to lever." (65)

It becomes apparent that the margins of safety built into debt structures were too great. and should be reduced...

As a result, over a period in which the economy does well, views about acceptable debt structure change. In the dealmaking

that goes on between banks, investment bankers, and businessmen, the acceptable amount of debt to use in financing various

types of activity and positions increases.

This increase in the weight of debt financing raises the market once of capital assets and increases investment. As this continues

the economy is transformed into a boom economy... � (65)

This transforms a period of tranquil growth into a period of speculative excess

�Stable growth is inconsistent with the manner in which investment is determined in an economy in which debt-financed ownership

of capital assets exists, and the extent to which such debt financing can be carried is market determined.

It follows that the fundamental instability of a capitalist economy is upward.

The tendency to transform doing well into a speculative investment boom is the basic instability in a capitalist economy."

(65)

He called his model the "Financial Instability Hypothesis". More boldly we can talk about Minsky model of economic

activity. According to Steve Keen, Minsky model boils down to three statements:

The employment rate will rise if economic growth exceeds the sum of population growth and growth in labor productivity;

The wages share of output will rise if money wage demands exceed the sum of inflation and growth in labor productivity; and

The private debt to GDP ratio will rise if the rate of growth of private debt exceeds the sum of inflation plus the rate of economic

growth.

He considered the rising of private debt to GDP ratio to be an immanent feature of capitalism that lead to financial

crisis. While the ultimate feature of neoliberalism is redistribution of wealth up (rising inequality) it can continue only while private debt

can compensate that sliding share of labor wages in GDP. After that the crisis of neoliberalism became a reality,

the reality the US faces today. Which gave rise of Russophobia as a primitive attempt to find a scapegoat for the current

problems of the US society and growing delegitimization of the US neoliberal elite. In this sense Minsky was more astute

critic of capitalism and by extension of neoliberalism, then Marx.

Several other source of financial instability were pointed out by others:

The logic of markets gets extended to �fictitious commodities� � land, labor, and money.Polanyi (1944) famously

zeroed in on the way that today, arguably, it is the logic of finance that has been

so extended, turning everything it touches into an asset with a speculative price.

Excessive accumulations of financial wealth and emergences of the class of billionaires, large part of which

constitutes of financial moguls speculating with "other people's money" (via 401K funds, hedge funds, high frequency

trading etc) � tend to undermine democratic institutions and lead

to the gradual shift to inverted totalitarism, and later to neofascism. Brandeis (1914) thought that excessive accumulations of financial wealth � �other people�s money� � tend to

undermine democratic institutions (among other problems). Today, arguably TBTF financial institution are the

most serious threat for the remnants of the democracy in the USA.

The idea of Minsky moment is related to the fact that the fractional reserve banking periodically causes credit collapse

when the

leveraged credit expansion goes into reverse. And mainstream economists do not want to talk about the fact that increasing confidence

breeds increased leverage. So financial stability breeds instability and subsequent financial crisis. All actions to guarantee a market

rise, ultimately guarantee it's destruction because greed will always take advantage of a "sure thing" and push it beyond reasonable

boundaries.

In other words, market players are not rational and assume that it would be foolish not to maximize leverage in

a market which is going up. So the fractional reserve banking mechanisms ultimately and ironically lead to over lending and guarantee

the subsequent crisis and the market's destruction. Stability breed instability.

Fractional reserve banking based economic system with private players (aka capitalism) is inherently unstable.

It periodically causes credit collapse when the

leveraged credit expansion goes into reverse. In other words, market players are not rational and assume that it would be foolish not to maximize leverage in

a market which is going up.

That means that fractional reserve banking based economic system with private players (aka capitalism) is inherently unstable. And

first of all because fractional reserve banking is debt based. In order to have growth it must create debt. Eventually the pyramid

of debt crushes and crisis hit. When the credit expansion fuels asset price bubbles, the dangers for the financial sector and the real

economy are substantial because this way the credit boom bubble is inflated which eventually burst. The damage done to the economy by

the bursting of credit boom bubbles is significant and long lasting.

Blissex said...

�When credit growth fuels asset price bubbles, the dangers for the financial sector and the real economy are much more

substantial.�

So M Minsky 50 years ago and M Pettis 15 years ago (in his "The volatility machine") had it right? Who could have imagined!

:-)

�In the past decades, central banks typically have taken a hands-off approach to asset price bubbles and credit booms.�

If only! They have been feeding credit-based asset price bubbles by at the same time weakening regulations to push up allowed

capital-leverage ratios, and boosting the quantity of credit as high as possible, but specifically most for leveraged speculation

on assets, by allowing vast-overvaluations on those assets.

Central banks have worked hard in most Anglo-American countries to redistribute income and wealth from "inflationary" worker

incomes to "non-inflationary" rentier incomes via hyper-subsidizing with endless cheap credit the excesses of financial speculation

in driving up asset prices.

Not very hands-off at all.

Steve Keen clearly understands this mechanism. See http://www.debtdeflation.com/blogs/manifesto/ John Kay in his January 5 2010 FT column very aptly explained the systemic instability of financial sector hypothesis:

The credit crunch of 2007-08 was the third phase of a larger and longer financial crisis. The first phase was the emerging market

defaults of the 1990s. The second was the new economy boom and bust at the turn of the century. The third was the collapse of markets

for structured debt products, which had grown so rapidly in the five years up to 2007.

The manifestation of the problem in each phase was different � first emerging markets, then stock markets, then debt. But the

mechanics were essentially the same. Financial institutions identified a genuine economic change � the assimilation of some

poor countries into the global economy, the opportunities offered to business by new information technology, and the development

of opportunities to manage risk and maturity mismatch more effectively through markets. Competition to sell products led to

wild exaggeration of the pace and scope of these trends. The resulting herd enthusiasm led to mispricing � particularly in asset

markets, which yielded large, and largely illusory, profits, of which a substantial fraction was paid to employees.

Eventually, at the end of each phase, reality impinged. The activities that once seemed so profitable � funding the financial systems

of emerging economies, promoting start-up internet businesses, trading in structured debt products � turned out, in fact, to have

been a source of losses. Lenders had to make write-offs, most of the new economy stocks proved valueless and many structured products

became unmarketable. Governments, and particularly the US government, reacted on each occasion by pumping money into the financial

system in the hope of staving off wider collapse, with some degree of success. At the end of each phase, regulators and financial

institutions declared that lessons had been learnt. While measures were implemented which, if they had been introduced five years

earlier, might have prevented the most recent crisis from taking the particular form it did, these responses addressed the particular

problem that had just occurred, rather than the underlying generic problems of skewed incentives and dysfunctional institutional

structures.

The public support of markets provided on each occasion the fuel needed to stoke the next crisis. Each boom and bust is larger than

the last. Since the alleviating action is also larger, the pattern is one of cycles of increasing amplitude.

I do not know what the epicenter of the next crisis will be, except that it is unlikely to involve structured debt products. I do

know that unless human nature changes or there is fundamental change in the structure of the financial services industry � equally

improbable � there will be another manifestation once again based on naive extrapolation and collective magical thinking. The recent

crisis taxed to the full � the word tax is used deliberately � the resources of world governments and their citizens. Even if there

is will to respond to the next crisis, the capacity to do so may not be there.

The citizens of that most placid of countries, Iceland, now backed by their president, have found a characteristically polite

and restrained way of disputing an obligation to stump up large sums of cash to pay for the arrogance and greed of other people.

They are right. We should listen to them before the same message is conveyed in much more violent form, in another place and at another

time. But it seems unlikely that we will.

We made a mistake in the closing decades of the 20th century. We removed restrictions that had imposed functional separation

on financial institutions. This led to businesses riddled with conflicts of interest and culture, controlled by warring groups

of their own senior employees. The scale of resources such businesses commanded enabled them to wield influence to create a � for

them � virtuous circle of growing economic and political power. That mistake will not be easily remedied, and that is why I view

the new decade with great apprehension. In the name of free markets, we created a monster that threatens to destroy the very free

markets we extol.

While Hyman Minsky was the first clearly formulate the financial instability hypothesis I think Keynes understood

the same dynamic pretty well. He postulated that a world with a large financial sector and an excessive emphasis on the production of investment

products creates instability both in terms of output and prices. In other words it automatically tends to generate credit and asset

bubbles. The key driver of taking excessive risk is the fact that financial professionals generally risk other people�s money and due to this fact have

asymmetrical incentives:

They get big rewards when bets go right

They don�t have to pay when bets go wrong.

The key driver of taking excessive risk is the fact that financial professionals generally risk other people�s money and due to this fact have

asymmetrical incentives:

They get big rewards when bets go right

They don�t have to pay when bets go wrong.

This asymmetrical incentives ensure that the financial system is structurally biased toward taking on more risk than what should

be taken.

This asymmetry is not a new observation of this systemic problem. Andrew Jackson noted it in much more polemic way long ago:

�Gentlemen, I have had men watching you for a long time and I am convinced that you have used the funds of the bank to speculate

in the breadstuffs of the country.When you won, you divided the profits amongst you, and when you lost, you charged

it to the bank. You tell me that if I take the deposits from the bank and annul its charter, I shall ruin ten thousand families.

That may be true, gentlemen, but that is your sin! Should I let you go on, you will ruin fifty thousand families, and that would

be my sin! You are a den of vipers and thieves. I intend to rout you out, and by the grace of the Eternal God, will rout you out.�

This asymmetrical incentives ensure that the financial system is structurally biased toward taking on more risk than what should

be taken. In other words it naturally tend to slide to the casino model, the with omnipresent reckless gambling as the primary

and the most profitable mode of operation while an opportunities last. The only way to counter this is to throw sand into the

wheels of financial mechanism: enforce strict regulations, limit money supplies and periodically jail too enthusiastic bankers.

The latter is as important or even more important as the other two because bankers tend to abuse "limited liability" status like no

other sector.

Asset inflation over the past 10 years and the subsequent catastrophe incurred is a way classic behavior of dynamic system with strong

positive feedback loop. Such behavior does not depends of personalities of bankers or policymakers, but is an immanent property

of this class of dynamic systems. And the main driving force here was deregulation. So its important that new regulation has safety

feature which make removal of it more complicated and requiring bigger majority like is the case with constitutional issues.

Another fact was the fact that due to perverted incentives, accounting in the banks was fraudulent from the very beginning

and it was fraudulent on purpose. Essentially accounting in banks automatically become as bad as law enforcement permits. This

is a classic case of control fraud and from prevention standpoint is make sense to establish huge penalties for auditors, which might

hurt healthy institutions but help to ensure that the most fraudulent institution lose these bank charter before affecting the whole

system. With the anti-regulatory zeal of Bush II administration the level of auditing became too superficial, almost non-existent.

I remember perverted dances with Sarbanes�Oxley when it

was clear from the very beginning that the real goal is not to strengthen accounting but to earn fees and to create as much profitable

red tape as possible, in perfect Soviet bureaucracy style.

Deregulation also increases systemic risk by influencing the real goals of financial organizations. At some point of

deregulation process the goal of higher remuneration for the top brass becomes self-sustainable trend and replaces all other goals

of the financial organization. This is the essence of Martin Taylor�s, the former chief executive of Barclays, article

FT.com - Innumerate bankers were ripe

for a reckoning in the Financial Times (Dec 15, 2009), which is worth reading in its entirety:

City people have always been paid well relative to others, but megabonuses are quite new. From my own experience,

in the mid-1990s no more than four or five employees of Barclays� then investment bank were paid more than �1m, and no one

got near �2m. Around the turn of the millennium across the market things began to take off, and accelerated rapidly � after

a pause in 2001-03 � so that exceptionally high remuneration, not just individually, but in total, was paid out between 2004 and

2007.

Observers of financial services saw unbelievable prosperity and apparently immense value added. Yet two years later the

whole industry was bankrupt. A simple reason underlies this: any industry that pays out in cash colossal accounting profits

that are largely imaginary will go bust quickly. Not only has the industry � and by extension societies that depend on it �

been spending money that is no longer there, it has been giving away money that it only imagined it had in the first place. Worse,

it seems to want to do it all again.

What were the sources of this imaginary wealth?

First, spreads on credit that took no account of default probabilities (bankers have been doing this for centuries, but not

on this scale).

Second, unrealised mark-to-market profits on the trading book, especially in illiquid instruments.

Third, profits conjured up by taking the net present value of streams of income stretching into the future, on derivative

issuance for example.

In the last two of these the bank was not receiving any income, merely �booking revenues�. How could they pay this

non-existent wealth out in cash to their employees? Because they had no measure of cash flow to tell them they were idiots,

and because everyone else was doing it. Paying out 50 per cent of revenues to staff had become the rule, even when the �revenues�

did not actually consist of money.

In the next phase instability is amplified by the way governments and central banks respond to crises caused by credit bubble: the

state has powerful means to end a recession, but the policies it uses give rise to the next phase of instability, the next bubble�.

When money is virtually free � or, at least, at 0.5 per cent � traders feel stupid if they don�t leverage up to the hilt. Thus previous

bubble and crash become a dress rehearsal for the next.

Resulting self-sustaining "boom-bust" cycle is very close how electronic systems with positive feedback loop behave and

cannot be explained by neo-classical macroeconomic models. Like with electronic devices the financial institution in this mode are unable

to provide the services that are needed.

As Minsky noted long ago (sited from Stephen Mihm

Why capitalism fails

Boston Globe):

Modern finance, he argued, was far from the stabilizing force that mainstream economics portrayed: rather, it was a system

that created the illusion of stability while simultaneously creating the conditions for an inevitable and dramatic collapse.

...our whole financial system contains the seeds of its own destruction. �Instability,� he wrote, �is an inherent and inescapable

flaw of capitalism.�

Minsky�s vision might have been dark, but he was not a fatalist; he believed it was possible to craft policies that could blunt

the collateral damage caused by financial crises. But with a growing number of economists eager to declare the recession over, and

the crisis itself apparently behind us, these policies may prove as discomforting as the theories that prompted them in the first

place. Indeed, as economists re-embrace Minsky�s prophetic insights, it is far from clear that they�re ready to reckon with the full

implications of what he saw.

And he understood the roots of the current credit bubble much better that neoclassical economists like Bernanke:

As people forget that failure is a possibility, a �euphoric economy� eventually develops, fueled by the rise of far riskier borrowers

- what [Minsky] called speculative borrowers, those whose income would cover interest payments but not the principal;

and those he called �Ponzi borrowers,� those whose income could cover neither, and could only pay their bills by borrowing

still further.

As these latter categories grew, the overall economy would shift from a conservative but profitable environment to a much more

freewheeling system dominated by players whose survival depended not on sound business plans, but on borrowed money and freely available

credit.

Minsky�s financial instability hypothesis suggests that when optimism is high and ample funds are available for investment,

investors tend to migrate from the safe hedge end of the Minsky spectrum to the risky speculative and Ponzi end. Indeed, in the current

crisis, investors tried to raise returns by increasing leverage and switching to financing via short-term � sometimes overnight � borrowing

(Too late to learn?):

In the church of Friedman, inflation was the ol' devil tempting the good folk; the 1980s seemed to prove that, let loose, it would

cause untold havoc on the populace. But, as Barbera notes:

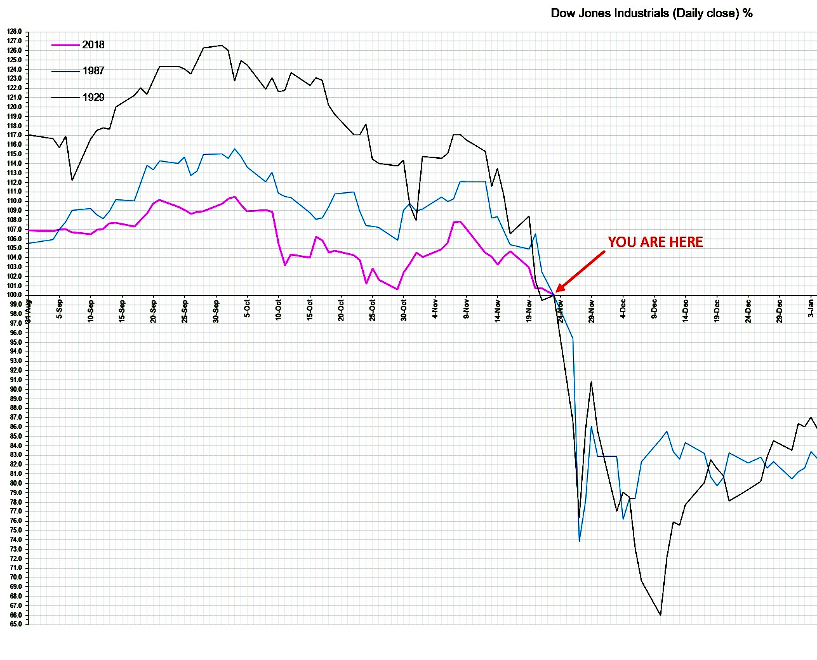

The last five major global cyclical events were the early 1990s recession - largely occasioned by the US Savings & Loan crisis,

the collapse of Japan Inc after the stock market crash of 1990, the Asian crisis of the mid-1990s, the fabulous technology boom/bust

cycle at the turn of the millennium, and the unprecedented rise and then collapse for US residential real estate in 2007-2008.

All five episodes delivered recessions, either global or regional. In no case was there a significant prior acceleration of wages

and general prices. In each case, an investment boom and an associated asset market ran to improbable heights and then collapsed.

From 1945 to 1985, there was no recession caused by the instability of investment prompted by financial speculation - and since

1985 there has been no recession that has not been caused by these factors.

Thus, meet the devil in Minsky's paradise - "an investment boom and an associated asset market [that] ran to improbable heights and

then collapsed".

According the Barbera, "Minsky's financial instability hypothesis depends critically on what amounts to a sociological insight.

People change their minds about taking risks. They don't make a one-time rational judgment about debt use and stock market exposure

and stick to it. Instead, they change their minds over time. And history is quite clear about how they change their minds. The longer

the good times endure, the more people begin to see wisdom in risky strategies."

Current economy state can be called following Paul McCulley a "stable disequilibrium" very similar to a state a sand pile.

All this pile of stocks, debt instruments, derivatives, credit default swaps and God know corresponds to a pile of sand

that is on the verse of losing stability. Each financial player works hard to maximize their own personal outcome but the "invisible

hand" effect in adding sand to the pile that is increasing systemic instability. According to Minsky, the longer such situation continues

the more likely and violent an "avalanche".

The late Hunt Taylor wrote, in 2006:

"Let us start with what we know. First, these markets look nothing like anything I've ever encountered before. Their stunning

complexity, the staggering number of tradable instruments and their interconnectedness, the light-speed at which information moves,

the degree to which the movement of one instrument triggers nonlinear reactions along chains of related derivatives, and the requisite

level of mathematics necessary to price them speak to the reality that we are now sailing in uncharted waters.

"... I've had 30-plus years of learning experiences in markets, all of which tell me that technology and telecommunications

will not do away with human greed and ignorance. I think we will drive the car faster and faster until something bad happens.

And I think it will come, like a comet, from that part of the night sky where we least expect it."

This is a gold age for bankers. As Peter Boone Simon Johnson wrote in New Republic (The

Next Financial Crisis ):

Banking was once a dangerous profession. In Britain, for instance, bankers faced �unlimited liability�--that is,

if you ran a bank, and the bank couldn�t repay depositors or other creditors, those people had the right to confiscate all your personal

assets and income until you repaid. It wasn�t until the second half of the nineteenth century that Britain established limited

liability for bank owners. From that point on, British bankers no longer assumed much financial risk themselves.

In the United States, there was great experimentation with banking during the 1800s, but those involved in the enterprise typically

made a substantial commitment of their own capital. For example, there was a well-established tradition of �double liability,�

in which stockholders were responsible for twice the original value of their shares in a bank. This encouraged stockholders

to carefully monitor bank executives and employees. And, in turn, it placed a lot of pressure on those who managed banks. If they

fared poorly, they typically faced personal and professional ruin. The idea that a bank executive would retain wealth and social

status in the event of a self-induced calamity would have struck everyone--including bank executives themselves--as ludicrous.

Enter, in the early part of the twentieth century, the Federal Reserve. The Fed was founded in 1913, but discussion about whether

to create a central bank had swirled for years. �No one can carefully study the experience of the other great commercial nations,�

argued Republican Senator Nelson Aldrich in an influential 1909 speech, �without being convinced that disastrous results of recurring

financial crises have been successfully prevented by a proper organization of capital and by the adoption of wise methods of banking

and of currency�--in other words, a central bank. In November 1910, Aldrich and a small group of top financiers met on an isolated

island off the coast of Georgia. There, they hammered out a draft plan to create a strong central bank that would be owned by banks

themselves.

What these bankers essentially wanted was a bailout mechanism for the aftermath of speculative crashes--something

more durable than J.P. Morgan, who saved the day in the Panic of 1907 but couldn�t be counted on to live forever. While they sought

informal government backing and substantial government financial support for their new venture, the bankers also wanted it to remain

free of government interference, oversight, or control.

Another destabilizing fact is so called myth of invisible hand which is closely related to the myth about market self-regulation.

The misunderstood argument of Adam Smith [1776], the founder of modern economics, that free markets led to efficient outcomes, �as if

by an invisible hand� has played a central role in these debates: it suggested that we could, by and large, rely on markets without

government intervention. About "invisible hand" deification, see

The Invisible Hand, Trumped by

Darwin - NYTimes.com. One of the most important counterargument against financial market self-regulation is existence of so called

�Minsky moments�:

�Minsky� was shorthand for Hyman Minsky, an American macroeconomist who died over a decade ago. He predicted almost exactly

the kind of meltdown that recently hammered the global economy. He believed in capitalism, but also believed it had almost a genetic

weakness. Modern finance, he argued, was far from the stabilizing force that mainstream economics portrayed: rather, it was a system

that created the illusion of stability while simultaneously creating the conditions for an inevitable and dramatic collapse.

In other words, the one person who foresaw the crisis also believed that our whole financial system contains the seeds of its

own destruction. �Instability,� he wrote, �is an inherent and inescapable flaw of capitalism.�

Minsky believed it was possible to craft policies that could blunt the collateral damage caused by financial crises. As economists

re-embrace Minsky�s prophetic insights, it is far from clear that they�re ready to reckon with the full implications of what he saw.

Minsky theory was not well received due to powerful orthodoxy, born in the years after World War II, known as the neoclassical

synthesis. The older belief in a self-regulating, self-stabilizing free market had selectively absorbed a few insights from John

Maynard Keynes, the great economist of the 1930s who wrote extensively of the ways that capitalism might fail to maintain full employment.

Most economists still believed that free-market capitalism was a fundamentally stable basis for an economy, though thanks to Keynes,

some now acknowledged that government might under certain circumstances play a role in keeping the economy - and employment - on

an even keel.

Economists like Paul Samuelson became the public face of the new establishment; he and others at a handful of top universities

became deeply influential in Washington. In theory, Minsky could have been an academic star in this new establishment: Like Samuelson,

he earned his doctorate in economics at Harvard University, where he studied with legendary Austrian economist Joseph Schumpeter,

as well as future Nobel laureate Wassily Leontief.

But Minsky was cut from different cloth than many of the other big names. The descendent of immigrants from Minsk, in modern-day

Belarus, Minsky was a red-diaper baby, the son of Menshevik socialists. While most economists spent the 1950s and 1960s toiling over

mathematical models, Minsky pursued research on poverty, hardly the hottest subfield of economics. With long, wild, white hair, Minsky

was closer to the counterculture than to mainstream economics. He was, recalls the economist L. Randall Wray, a former student, a

�character.�

So while his colleagues from graduate school went on to win Nobel prizes and rise to the top of academia, Minsky languished. He

drifted from Brown to Berkeley and eventually to Washington University. Indeed, many economists weren�t even aware of his work. One

assessment of Minsky published in 1997 simply noted that his �work has not had a major influence in the macroeconomic discussions

of the last thirty years.�

Yet he was busy. In addition to poverty, Minsky began to delve into the field of finance, which despite its seeming importance

had no place in the theories formulated by Samuelson and others. He also began to ask a simple, if disturbing question: �Can �it�

happen again?� - where �it� was, like Harry Potter�s nemesis Voldemort, the thing that could not be named: the Great Depression.

In his writings, Minsky looked to his intellectual hero, Keynes, arguably the greatest economist of the 20th century. But where

most economists drew a single, simplistic lesson from Keynes - that government could step in and micromanage the economy, smooth

out the business cycle, and keep things on an even keel - Minsky had no interest in what he and a handful of other dissident economists

came to call �bastard Keynesianism.�

Instead, Minsky drew his own, far darker, lessons from Keynes�s landmark writings, which dealt not only with the problem of unemployment,

but with money and banking. Although Keynes had never stated this explicitly, Minsky argued that Keynes�s collective work amounted

to a powerful argument that capitalism was by its very nature unstable and prone to collapse. Far from trending toward some magical

state of equilibrium, capitalism would inevitably do the opposite. It would lurch over a cliff.

This insight bore the stamp of his advisor Joseph Schumpeter, the noted Austrian economist now famous for documenting capitalism�s

ceaseless process of �creative destruction.� But Minsky spent more time thinking about destruction than creation. In doing so, he

formulated an intriguing theory: not only was capitalism prone to collapse, he argued, it was precisely its periods of economic stability

that would set the stage for monumental crises.

Minsky called his idea the �Financial Instability Hypothesis.� In the wake of a depression, he noted, financial institutions are

extraordinarily conservative, as are businesses. With the borrowers and the lenders who fuel the economy all steering clear of high-risk

deals, things go smoothly: loans are almost always paid on time, businesses generally succeed, and everyone does well. That success,

however, inevitably encourages borrowers and lenders to take on more risk in the reasonable hope of making more money. As Minsky

observed, �Success breeds a disregard of the possibility of failure.�

As people forget that failure is a possibility, a �euphoric economy� eventually develops, fueled by the rise of far riskier borrowers

- what he called speculative borrowers, those whose income would cover interest payments but not the principal; and those he called

�Ponzi borrowers,� those whose income could cover neither, and could only pay their bills by borrowing still further. As these latter

categories grew, the overall economy would shift from a conservative but profitable environment to a much more freewheeling system

dominated by players whose survival depended not on sound business plans, but on borrowed money and freely available credit.

Once that kind of economy had developed, any panic could wreck the market. The failure of a single firm, for example, or the revelation

of a staggering fraud could trigger fear and a sudden, economy-wide attempt to shed debt. This watershed moment - what was later

dubbed the �Minsky moment� - would create an environment deeply inhospitable to all borrowers. The speculators and Ponzi borrowers

would collapse first, as they lost access to the credit they needed to survive. Even the more stable players might find themselves

unable to pay their debt without selling off assets; their forced sales would send asset prices spiraling downward, and inevitably,

the entire rickety financial edifice would start to collapse. Businesses would falter, and the crisis would spill over to the �real�

economy that depended on the now-collapsing financial system.

From the 1960s onward, Minsky elaborated on this hypothesis. At the time he believed that this shift was already underway: postwar

stability, financial innovation, and the receding memory of the Great Depression were gradually setting the stage for a crisis of

epic proportions. Most of what he had to say fell on deaf ears. The 1960s were an era of solid growth, and although the economic

stagnation of the 1970s was a blow to mainstream neo-Keynesian economics, it did not send policymakers scurrying to Minsky. Instead,

a new free market fundamentalism took root: government was the problem, not the solution.

Moreover, the new dogma coincided with a remarkable era of stability. The period from the late 1980s onward has been dubbed the

�Great Moderation,� a time of shallow recessions and great resilience among most major industrial economies. Things had never been

more stable. The likelihood that �it� could happen again now seemed laughable.

Yet throughout this period, the financial system - not the economy, but finance as an industry - was growing by leaps and bounds.

Minsky spent the last years of his life, in the early 1990s, warning of the dangers of securitization and other forms of financial

innovation, but few economists listened. Nor did they pay attention to consumers� and companies� growing dependence on debt, and

the growing use of leverage within the financial system.

By the end of the 20th century, the financial system that Minsky had warned about had materialized, complete with speculative

borrowers, Ponzi borrowers, and precious few of the conservative borrowers who were the bedrock of a truly stable economy. Over decades,

we really had forgotten the meaning of risk. When storied financial firms started to fall, sending shockwaves through the �real�

economy, his predictions started to look a lot like a road map.

�This wasn�t a Minsky moment,� explains Randall Wray. �It was a Minsky half-century.�

Minsky is now all the rage. A year ago, an influential Financial Times columnist confided to readers that rereading Minsky�s 1986

�masterpiece� - �Stabilizing an Unstable Economy� - �helped clear my mind on this crisis.� Others joined the chorus. Earlier this

year, two economic heavyweights - Paul Krugman and Brad DeLong - both tipped their hats to him in public forums. Indeed, the Nobel

Prize-winning Krugman titled one of the Robbins lectures at the London School of Economics �The Night They Re-read Minsky.�

Today most economists, it�s safe to say, are probably reading Minsky for the first time, trying to fit his unconventional insights

into the theoretical scaffolding of their profession. If Minsky were alive today, he would no doubt applaud this belated acknowledgment,

even if it has come at a terrible cost. As he once wryly observed, �There is nothing wrong with macroeconomics that another depression

[won�t] cure.�

But does Minsky�s work offer us any practical help? If capitalism is inherently self-destructive and unstable - never mind that

it produces inequality and unemployment, as Keynes had observed - now what?

After spending his life warning of the perils of the complacency that comes with stability - and having it fall on deaf ears -

Minsky was understandably pessimistic about the ability to short-circuit the tragic cycle of boom and bust. But he did believe that

much could be done to ameliorate the damage.

To prevent the Minsky moment from becoming a national calamity, part of his solution (which was shared with other economists)

was to have the Federal Reserve - what he liked to call the �Big Bank� - step into the breach and act as a lender of last resort

to firms under siege. By throwing lines of liquidity to foundering firms, the Federal Reserve could break the cycle and stabilize

the financial system. It failed to do so during the Great Depression, when it stood by and let a banking crisis spiral out of control.

This time, under the leadership of Ben Bernanke - like Minsky, a scholar of the Depression - it took a very different approach, becoming

a lender of last resort to everything from hedge funds to investment banks to money market funds.

Minsky�s other solution, however, was considerably more radical and less palatable politically. The preferred mainstream tactic

for pulling the economy out of a crisis was - and is - based on the Keynesian notion of �priming the pump� by sending money that

will employ lots of high-skilled, unionized labor - by building a new high-speed train line, for example.

Minsky, however, argued for a �bubble-up� approach, sending money to the poor and unskilled first. The government - or what

he liked to call �Big Government� - should become the �employer of last resort,� he said, offering a job to anyone who wanted one

at a set minimum wage. It would be paid to workers who would supply child care, clean streets, and provide services that

would give taxpayers a visible return on their dollars. In being available to everyone, it would be even more ambitious than the

New Deal, sharply reducing the welfare rolls by guaranteeing a job for anyone who was able to work. Such a program would not only

help the poor and unskilled, he believed, but would put a floor beneath everyone else�s wages too, preventing salaries of more skilled

workers from falling too precipitously, and sending benefits up the socioeconomic ladder.

While economists may be acknowledging some of Minsky�s points on financial instability, it�s safe to say that even liberal policymakers

are still a long way from thinking about such an expanded role for the American government. If nothing else, an expensive full-employment

program would veer far too close to socialism for the comfort of politicians. For his part, Wray thinks that the critics are apt

to misunderstand Minsky. �He saw these ideas as perfectly consistent with capitalism,� says Wray. �They would make capitalism better.�

But not perfect. Indeed, if there�s anything to be drawn from Minsky�s collected work, it�s that perfection, like stability and

equilibrium, are mirages. Minsky did not share his profession�s quaint belief that everything could be reduced to a tidy model, or

a pat theory. His was a kind of existential economics: capitalism, like life itself, is difficult, even tragic. �There is no simple

answer to the problems of our capitalism,� wrote Minsky. �There is no solution that can be transformed into a catchy phrase and carried

on banners.�

It�s a sentiment that may limit the extent to which Minsky becomes part of any new orthodoxy. But that�s probably how he would

have preferred it, believes liberal economist James Galbraith. �I think he would resist being domesticated,� says Galbraith. �He

spent his career in professional isolation.�

Stephen Mihm is a history professor at the University of Georgia and author of �A Nation of Counterfeiters� (Harvard, 2007).

� Copyright 2009 Globe Newspaper Company.

The conclusion to "Leveraged bubbles," by �scar Jord�,

Moritz Schularick, and Alan Taylor:

... In this column, we turned to economic history for the first comprehensive assessment of the economic risks of asset price

bubbles. We provide evidence about which types of bubbles matter and how their economic costs differ. Our historical analysis

shows that not all bubbles are created equal. When credit growth fuels asset price bubbles, the dangers for the financial

sector and the real economy are much more substantial. The damage done to the economy by the bursting of credit boom bubbles is

significant and long lasting.

In the past decades, central banks typically have taken a hands-off approach to asset price bubbles and credit booms. This way

of thinking has been criticised by some institutions, such as the BIS, that took a less rosy view of the self-equilibrating tendencies

of financial markets and warned of the potentially grave consequences of leveraged asset price bubbles. The findings presented

here can inform ongoing efforts to devise better macro-financial theory and real-world applications at a time when policymakers

are still searching for new approaches in the aftermath of the Great Recession.

"bursting of credit boom bubbles is significant and long lasting.

In the past decades, central banks typically have taken" ~~�scar Jord�, Moritz Schularick, and Alan Taylor:~

Did Kurt Vonnegut once quip

"Each fed governor likes to live on the edge, further out on a limb where she can see more then hope against hope that limb

will not break until she leaves office." ?

Imprecisely, yet left us with a memorable hint of both his genius and fed governor's stupidity.

djb said...

of course if wages kept up with productivity, there would not have been as much of a bubble because people could have paid more,

and borrowed less

but I doubt BIS was worried about that particular issue

Peter K. -> djb...

"This way of thinking has been criticised by some institutions, such as the BIS, that took a less rosy view of the self-equilibrating

tendencies of financial markets and warned of the potentially grave consequences of leveraged asset price bubbles."

Likewise I don't the believe the BIS is big on tighter regulation of the banks. As Krugman and others have pointed out, the BIS

is always for raising rates but switches rationals. Sometimes it's about inflation, sometimes bubbles.

We need a Fed that sets as policy buying long term debt that funds new infrastructure projects that are required by Federal regulation

to pay prevailing aka higher wages.

If in 2010, the Fed had bought $3 trillion in bonds for such projects as building the NE HSR, for all the cities fixing their

century old water and sewer systems, California's HSR, bonds for replacement bridges with tunnels as option, rerouting rail to eliminate

grade crossings to speed for freight and truck traffic, then the Fed could have done what Republicans have done up until the Republicans

decided to punish all the We the People for electing Obama.

Any debt issued that does not build new capital assets requiring American labor, ie, debt paying labor costs, is totally worthless

to the economy.

Other than for some existing constant wealth redistribution purposes - during 2008-2011 savers were protected against having their

wealth taken from them and given to the borrowers who had long ago spent it.

Arne said...

Is there some data on the extent to which asset price rises are credit fueled or not. My memory (which does not qualify as a data

source) says that the housing bubble was much more so than the dot-com bubble.

Blissex said...

�When credit growth fuels asset price bubbles, the dangers for the financial sector and the real economy are much more

substantial.�

So M Minsky 50 years ago and M Pettis 15 years ago (in his "The volatility machine") had it right? Who could have imagined!

:-)

�In the past decades, central banks typically have taken a hands-off approach to asset price bubbles and credit booms.�

If only! They have been feeding credit-based asset price bubbles by at the same time weakening regulations to push up allowed

capital-leverage ratios, and boosting the quantity of credit as high as possible, but specifically most for leveraged speculation

on assets, by allowing vast-overvaluations on those assets.

Central banks have worked hard in most Anglo-American countries to redistribute income and wealth from "inflationary" worker

incomes to "non-inflationary" rentier incomes via hyper-subsidizing with endless cheap credit the excesses of financial speculation

in driving up asset prices.

Are you questioning creating wealth by price inflation of decaying asset which are churned in pump and dump?

Do you believe selling and reselling the same fixed quantity of assets creates jobs through the wealth effect of workers spending

money they don't have to buy things on credit they can't pay back to keep up with the rich?

Wealth. Creating wealth. Wealth effect. Capital gains. Money in your pocket. Signs of free lunch economic smoke and mirrors.

Wealth is created by paid labor or hard labor by the owner of the created wealth. But paying labor costs as a virtue is not

something an economist is allowed to say in the post Reagan victory world.

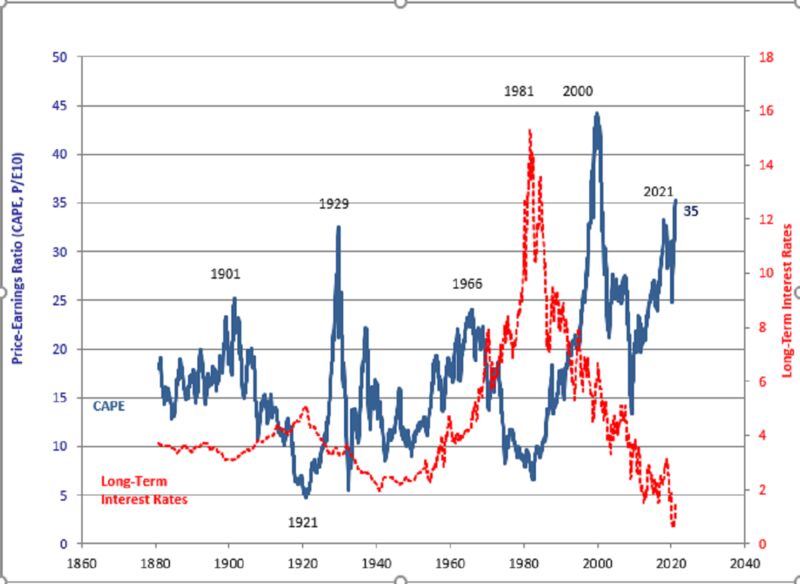

Listen to this article 6 minutes 00:00 / 06:06 1x Earnings, valuation and rampant speculation have all played a role in the extraordinary bull market that began a year ago this week. The latest combination of the three has a troubling reliance on the speculative element. A broad framework for thinking about stocks can be derived from the late economist Hyman Minsky's three stages of debt. In the first stage, borrowers take on only what they can afford to repay in full from their earnings by the time the debt matures; a standard mortgage works like this. Earnings, valuation and rampant speculation have all played a role in the extraordinary bull market that began a year ago this week. The latest combination of the three has a troubling reliance on the speculative element. A broad framework for thinking about stocks can be derived from the late economist Hyman Minsky's three stages of debt. In the first stage, borrowers take on only what they can afford to repay in full from their earnings by the time the debt matures; a standard mortgage works like this. A broad framework for thinking about stocks can be derived from the late economist Hyman Minsky's three stages of debt. In the first stage, borrowers take on only what they can afford to repay in full from their earnings by the time the debt matures; a standard mortgage works like this. A broad framework for thinking about stocks can be derived from the late economist Hyman Minsky's three stages of debt. In the first stage, borrowers take on only what they can afford to repay in full from their earnings by the time the debt matures; a standard mortgage works like this. U.S. 10-year Treasury yield Source: Tullett Prebon As of March 24 % Pre-pandemic peak of S&P 500 2020 '21 0.25 0.50 0.75 1.00 1.25 1.50 1.75 2.00 S&P 500 forward price/earnings ratio Source: Refinitiv Note: Weekly data S&P 500 peak 2020 '21 12 14 16 18 20 22 24 The parallel in the stock market is stocks going up when earnings -- or rather the expectation of earnings, since the market looks ahead -- go up. There is a risk of course, just as there is with debt: The earnings might not appear, and the stock goes back down. But earnings offer the least risky form of gains, and one that we should welcome as obviously justified. From the low in the summer, 2020 earnings forecasts jumped more than 10%, and expectations for this year rose more than 8%. Stocks responded. In Minsky's second stage, borrowers plan only to repay the interest, and refinance when the main debt is due to be repaid; much company debt works like this. It is taken out with a plan to roll it over indefinitely. Interest rates matter a lot: If they go down when the company needs to refinance, it will pay less. The equity parallel is to gains in valuation due to lower long-term rates. As with corporate debt, this is entirely justified and sustainable so long as rates stay low, because future earnings are now more appealing. The danger is that rates rise, in which case the stock might be hit no matter how earnings pan out. A big chunk of the gains in stocks in the past year came from the sharply lower rates in the first response to the pandemic when the Federal Reserve flooded the system with money. Price-to-forward-earnings multiples soared. From the S&P 500's low on March 23 to the end of June, the market went from 14 to more than 21 times estimated earnings 12 months ahead, even as those estimated earnings fell amid lockdown gloom. The yield on the 10-year Treasury, already down sharply from mid-February's high, fell further as stocks rebounded. In Minsky's third phase, borrowers take loans where they can't afford to pay either the interest or principal from income, in the hope of capital gains big enough to make up the gap. Land speculators are a prime example. The parallel in the stock market is the The parallel in the stock market is stocks going up when earnings -- or rather the expectation of earnings, since the market looks ahead -- go up. There is a risk of course, just as there is with debt: The earnings might not appear, and the stock goes back down. But earnings offer the least risky form of gains, and one that we should welcome as obviously justified. From the low in the summer, 2020 earnings forecasts jumped more than 10%, and expectations for this year rose more than 8%. Stocks responded. In Minsky's second stage, borrowers plan only to repay the interest, and refinance when the main debt is due to be repaid; much company debt works like this. It is taken out with a plan to roll it over indefinitely. Interest rates matter a lot: If they go down when the company needs to refinance, it will pay less. The equity parallel is to gains in valuation due to lower long-term rates. As with corporate debt, this is entirely justified and sustainable so long as rates stay low, because future earnings are now more appealing. The danger is that rates rise, in which case the stock might be hit no matter how earnings pan out. A big chunk of the gains in stocks in the past year came from the sharply lower rates in the first response to the pandemic when the Federal Reserve flooded the system with money. Price-to-forward-earnings multiples soared. From the S&P 500's low on March 23 to the end of June, the market went from 14 to more than 21 times estimated earnings 12 months ahead, even as those estimated earnings fell amid lockdown gloom. The yield on the 10-year Treasury, already down sharply from mid-February's high, fell further as stocks rebounded. In Minsky's third phase, borrowers take loans where they can't afford to pay either the interest or principal from income, in the hope of capital gains big enough to make up the gap. Land speculators are a prime example. The parallel in the stock market is the In Minsky's second stage, borrowers plan only to repay the interest, and refinance when the main debt is due to be repaid; much company debt works like this. It is taken out with a plan to roll it over indefinitely. Interest rates matter a lot: If they go down when the company needs to refinance, it will pay less. The equity parallel is to gains in valuation due to lower long-term rates. As with corporate debt, this is entirely justified and sustainable so long as rates stay low, because future earnings are now more appealing. The danger is that rates rise, in which case the stock might be hit no matter how earnings pan out. A big chunk of the gains in stocks in the past year came from the sharply lower rates in the first response to the pandemic when the Federal Reserve flooded the system with money. Price-to-forward-earnings multiples soared. From the S&P 500's low on March 23 to the end of June, the market went from 14 to more than 21 times estimated earnings 12 months ahead, even as those estimated earnings fell amid lockdown gloom. The yield on the 10-year Treasury, already down sharply from mid-February's high, fell further as stocks rebounded. In Minsky's third phase, borrowers take loans where they can't afford to pay either the interest or principal from income, in the hope of capital gains big enough to make up the gap. Land speculators are a prime example. The parallel in the stock market is the In Minsky's second stage, borrowers plan only to repay the interest, and refinance when the main debt is due to be repaid; much company debt works like this. It is taken out with a plan to roll it over indefinitely. Interest rates matter a lot: If they go down when the company needs to refinance, it will pay less. The equity parallel is to gains in valuation due to lower long-term rates. As with corporate debt, this is entirely justified and sustainable so long as rates stay low, because future earnings are now more appealing. The danger is that rates rise, in which case the stock might be hit no matter how earnings pan out. A big chunk of the gains in stocks in the past year came from the sharply lower rates in the first response to the pandemic when the Federal Reserve flooded the system with money. Price-to-forward-earnings multiples soared. From the S&P 500's low on March 23 to the end of June, the market went from 14 to more than 21 times estimated earnings 12 months ahead, even as those estimated earnings fell amid lockdown gloom. The yield on the 10-year Treasury, already down sharply from mid-February's high, fell further as stocks rebounded. In Minsky's third phase, borrowers take loans where they can't afford to pay either the interest or principal from income, in the hope of capital gains big enough to make up the gap. Land speculators are a prime example. The parallel in the stock market is the The equity parallel is to gains in valuation due to lower long-term rates. As with corporate debt, this is entirely justified and sustainable so long as rates stay low, because future earnings are now more appealing. The danger is that rates rise, in which case the stock might be hit no matter how earnings pan out. A big chunk of the gains in stocks in the past year came from the sharply lower rates in the first response to the pandemic when the Federal Reserve flooded the system with money. Price-to-forward-earnings multiples soared. From the S&P 500's low on March 23 to the end of June, the market went from 14 to more than 21 times estimated earnings 12 months ahead, even as those estimated earnings fell amid lockdown gloom. The yield on the 10-year Treasury, already down sharply from mid-February's high, fell further as stocks rebounded. In Minsky's third phase, borrowers take loans where they can't afford to pay either the interest or principal from income, in the hope of capital gains big enough to make up the gap. Land speculators are a prime example. The parallel in the stock market is the The equity parallel is to gains in valuation due to lower long-term rates. As with corporate debt, this is entirely justified and sustainable so long as rates stay low, because future earnings are now more appealing. The danger is that rates rise, in which case the stock might be hit no matter how earnings pan out. A big chunk of the gains in stocks in the past year came from the sharply lower rates in the first response to the pandemic when the Federal Reserve flooded the system with money. Price-to-forward-earnings multiples soared. From the S&P 500's low on March 23 to the end of June, the market went from 14 to more than 21 times estimated earnings 12 months ahead, even as those estimated earnings fell amid lockdown gloom. The yield on the 10-year Treasury, already down sharply from mid-February's high, fell further as stocks rebounded. In Minsky's third phase, borrowers take loans where they can't afford to pay either the interest or principal from income, in the hope of capital gains big enough to make up the gap. Land speculators are a prime example. The parallel in the stock market is the A big chunk of the gains in stocks in the past year came from the sharply lower rates in the first response to the pandemic when the Federal Reserve flooded the system with money. Price-to-forward-earnings multiples soared. From the S&P 500's low on March 23 to the end of June, the market went from 14 to more than 21 times estimated earnings 12 months ahead, even as those estimated earnings fell amid lockdown gloom. The yield on the 10-year Treasury, already down sharply from mid-February's high, fell further as stocks rebounded. In Minsky's third phase, borrowers take loans where they can't afford to pay either the interest or principal from income, in the hope of capital gains big enough to make up the gap. Land speculators are a prime example. The parallel in the stock market is the A big chunk of the gains in stocks in the past year came from the sharply lower rates in the first response to the pandemic when the Federal Reserve flooded the system with money. Price-to-forward-earnings multiples soared. From the S&P 500's low on March 23 to the end of June, the market went from 14 to more than 21 times estimated earnings 12 months ahead, even as those estimated earnings fell amid lockdown gloom. The yield on the 10-year Treasury, already down sharply from mid-February's high, fell further as stocks rebounded. In Minsky's third phase, borrowers take loans where they can't afford to pay either the interest or principal from income, in the hope of capital gains big enough to make up the gap. Land speculators are a prime example. The parallel in the stock market is the In Minsky's third phase, borrowers take loans where they can't afford to pay either the interest or principal from income, in the hope of capital gains big enough to make up the gap. Land speculators are a prime example. The parallel in the stock market is the In Minsky's third phase, borrowers take loans where they can't afford to pay either the interest or principal from income, in the hope of capital gains big enough to make up the gap. Land speculators are a prime example. The parallel in the stock market is the The parallel in the stock market is the The parallel in the stock market is the hunt for the greater fool . Sure, GameStop < shares bear no relation to the reality < of the company, but I can make money from buying an overpriced stock if I can find someone willing to pay even more because they "like the stock." Wild bets became obvious this year, as newcomers armed with stimulus, or "stimmy," checks Wild bets became obvious this year, as newcomers armed with stimulus, or "stimmy," checks Wild bets became obvious this year, as newcomers armed with stimulus, or "stimmy," checks drove up the price of many tiny stocks, penny shares and those popular on Reddit discussion boards. Speculative bets such as the solar and ARK ETFs rallied up until mid-February, long after growth stocks peaked in August Price performance Source: FactSet *Russell 1000 indexes As of March 25, 7:02 p.m. ET % Invesco Solar Value* ARK Innovation Growth* Sept. 2020 '21 -25 0 25 50 75 100 125 The concern for investors: How much of the market's gain is thanks to this pure speculation, and how much to the justifiable gains of the improving economy and low rates? If too much comes from speculation, the danger is that we run out of greater fools and prices quickly drop back. The concern for investors: How much of the market's gain is thanks to this pure speculation, and how much to the justifiable gains of the improving economy and low rates? If too much comes from speculation, the danger is that we run out of greater fools and prices quickly drop back. me title= A look at how stocks moved through the pandemic suggests earnings and bond yields are still much more important than the gambling element for the market as a whole, but is still troubling. From the S&P peak in mid-February to the end of June, the story was of cratering earnings partly offset by higher valuations. The S&P was down 8%. Earnings forecasts for 12 months ahead fell 20%, while with 10-year yields down almost a full percentage point, valuations were up from a precrisis high of 19 times forecast earnings (itself the highest since the aftermath of the dot-com bubble) to 21 times. Growth stocks -- based on the Russell 1000 index of larger companies -- were slightly up, because they benefit most from falling bond yields, having more of their earnings far in the future. Cheap value stocks, which benefit less, were down 18%. A look at how stocks moved through the pandemic suggests earnings and bond yields are still much more important than the gambling element for the market as a whole, but is still troubling. From the S&P peak in mid-February to the end of June, the story was of cratering earnings partly offset by higher valuations. The S&P was down 8%. Earnings forecasts for 12 months ahead fell 20%, while with 10-year yields down almost a full percentage point, valuations were up from a precrisis high of 19 times forecast earnings (itself the highest since the aftermath of the dot-com bubble) to 21 times. Growth stocks -- based on the Russell 1000 index of larger companies -- were slightly up, because they benefit most from falling bond yields, having more of their earnings far in the future. Cheap value stocks, which benefit less, were down 18%. A look at how stocks moved through the pandemic suggests earnings and bond yields are still much more important than the gambling element for the market as a whole, but is still troubling. From the S&P peak in mid-February to the end of June, the story was of cratering earnings partly offset by higher valuations. The S&P was down 8%. Earnings forecasts for 12 months ahead fell 20%, while with 10-year yields down almost a full percentage point, valuations were up from a precrisis high of 19 times forecast earnings (itself the highest since the aftermath of the dot-com bubble) to 21 times. Growth stocks -- based on the Russell 1000 index of larger companies -- were slightly up, because they benefit most from falling bond yields, having more of their earnings far in the future. Cheap value stocks, which benefit less, were down 18%. From the S&P peak in mid-February to the end of June, the story was of cratering earnings partly offset by higher valuations. The S&P was down 8%. Earnings forecasts for 12 months ahead fell 20%, while with 10-year yields down almost a full percentage point, valuations were up from a precrisis high of 19 times forecast earnings (itself the highest since the aftermath of the dot-com bubble) to 21 times. Growth stocks -- based on the Russell 1000 index of larger companies -- were slightly up, because they benefit most from falling bond yields, having more of their earnings far in the future. Cheap value stocks, which benefit less, were down 18%. From the S&P peak in mid-February to the end of June, the story was of cratering earnings partly offset by higher valuations. The S&P was down 8%. Earnings forecasts for 12 months ahead fell 20%, while with 10-year yields down almost a full percentage point, valuations were up from a precrisis high of 19 times forecast earnings (itself the highest since the aftermath of the dot-com bubble) to 21 times. Growth stocks -- based on the Russell 1000 index of larger companies -- were slightly up, because they benefit most from falling bond yields, having more of their earnings far in the future. Cheap value stocks, which benefit less, were down 18%. Growth stocks -- based on the Russell 1000 index of larger companies -- were slightly up, because they benefit most from falling bond yields, having more of their earnings far in the future. Cheap value stocks, which benefit less, were down 18%. Growth stocks -- based on the Russell 1000 index of larger companies -- were slightly up, because they benefit most from falling bond yields, having more of their earnings far in the future. Cheap value stocks, which benefit less, were down 18%. NEWSLETTER SIGN-UP ( Mar 26, 2021 , www.wsj.com )

NEW YORK (Reuters) - In this manic era of meme stocks, cryptocurrencies and real-estate