|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

|

|

Switchboard | ||||

| Latest | |||||

| Past week | |||||

| Past month | |||||

Jun 19, 2015 | naked capitalism

Banks are Not Intermediaries of Loanable Funds – and Why This MattersPosted on June 19, 2015

Yves here. Over the years, we've regularly criticized economists like Bernanke and Krugman, who rely on the so-called loanable funds model, which sees banks as conduits of funds from savers to borrowers. Despite the fact that many central banks, such as the Bank of England, have stressed that that's not how banks actually work (banks create loans, which then produce the related deposit), central banks still cling to their hoary old framework. For instance, when I saw Janet Yellen speak at an Institute of New Economic Thinking conference in May, she cringe-makingly mentioned how banks channel scarce savings to investments.

Even worse, the macroeconomic models used by central banks incorporate the loanable funds point of view. This article describes what happens when you use a more realistic model of the financial system. Even though the paper is a bit stuffy, the results are clear: economies aren't self-correcting as the traditional view would have you believe but have boom/bust cycles (the term of art is "procyclical") and banks show the effects of policy changes much more rapidly.

Other economists who have been working to develop models that reflect the workings of the financial sector more accurately, like Steve Keen, have come to similar conclusions: that the current mainstream models, which serve as the basis for policy, present a fairy-tale story of economies that right themselves on their own, when in fact loans play a major, direct role in creating instability. It's not an exaggeration to depict the continued reliance on known-to-be-fatally-flawed tools as malpractice.

By Zoltan Jakab, Senior Economist at the Research Department, IMF, and Michael Kumhof, Senior Research Advisor at the Research Hub, Bank of England. Originally published at VoxEU

Problems in the banking sector played a seriously damaging role in the Great Recession. In fact, they continue to. This column argues that macroeconomic models were unable to explain the interaction between banks and the macro economy. The problem lies with thinking that banks create loans out of existing resources. Instead, they create new money in the form of loans. Macroeconomists need to reflect this in their models.

Problems in the banking sector played a critical role in triggering and prolonging the Great Recession. Unfortunately, macroeconomic models were initially not ready to provide much support in thinking about the interaction of banks with the macro economy. This has now changed.

However, there remain many unresolved issues (Adrian et al. 2013) including:

• The reasons for the extremely large changes to (and co-movements of) bank assets and bank debt;

• The extent to which the banking sector triggers or amplifies financial and business cycles; and

• The extent to which monetary and macro-prudential policies should lean against the wind in financial markets.

New Research

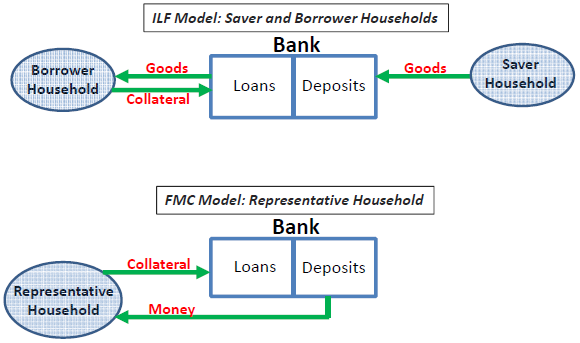

In our new work, we argue that many of these unresolved issues can be traced back to the fact that virtually all of the newly developed models are based on the highly misleading 'intermediation of loanable funds' theory of banking (Jakab and Kumhof 2015). We argue instead that the correct framework is 'money creation' theory.

In the intermediation of loanable funds model, bank loans represent the intermediation of real savings, or loanable funds, between non-bank savers and non-bank borrowers;

Lending starts with banks collecting deposits of real resources from savers and ends with the lending of those resources to borrowers. The problem with this view is that, in the real world, there are no pre-existing loanable funds, and intermediation of loanable funds-type institutions – which really amount to barter intermediaries in this approach – do not exist.

The key function of banks is the provision of financing, meaning the creation of new monetary purchasing power through loans, for a single agent that is both borrower and depositor.

Specifically, whenever a bank makes a new loan to a non-bank ('customer X'), it creates a new loan entry in the name of customer X on the asset side of its balance sheet, and it simultaneously creates a new and equal-sized deposit entry, also in the name of customer X, on the liability side of its balance sheet.

The bank therefore creates its own funding, deposits, through lending. It does so through a pure bookkeeping transaction that involves no real resources, and that acquires its economic significance through the fact that bank deposits are any modern economy's generally accepted medium of exchange.

The real challengeThis money creation function of banks has been repeatedly described in publications of the world's leading central banks (see McLeay et al. 2014a for an excellent summary). Our paper provides a comprehensive list of supporting citations and detailed explanations based on real-world balance sheet mechanics as to why intermediation of loanable funds-type institutions cannot possibly exist in the real world. What has been much more challenging, however, is the incorporation of these insights into macroeconomic models.

Our paper therefore builds examples of dynamic stochastic general equilibrium models with money creation banks, and then contrasts their predictions with those of otherwise identical money creation models. Figure 1 shows the simplest possible case of a money creation model, where banks interact with a single representative household. More elaborate money creation model setups with multiple agents are possible, and one of them is studied in the paper.

Figure 1.

The main reason for using money creation models is therefore that they correctly represent the function of banks. But in addition, the empirical predictions of the money creation model are qualitatively much more in line with the data than those of the intermediation of loanable funds model. The data, as documented in our paper, show large jumps in bank lending, pro- or acyclical bank leverage, and quantity rationing of credit during downturns. The model simulations in our paper show that, compared to intermediation of loanable funds models, and following identical shocks, money creation models predict changes in bank lending that are far larger, happen much faster, and have much larger effects on the real economy. Compared to intermediation of loanable funds models, money creation models also predict pro- or acyclical rather than countercyclical bank leverage, and an important role for quantity rationing of credit, rather than an almost exclusive reliance on price rationing, in response to contractionary shocks.

The fundamental reason for these differences is that savings in the intermediation of loanable funds model of banking need to be accumulated through a process of either producing additional resources or foregoing consumption of existing resources, a physical process that by its very nature is gradual and slow. On the other hand, money creation banks that create purchasing power can technically do so instantaneously, because the process does not involve physical resources, but rather the creation of money through the simultaneous expansion of both sides of banks' balance sheets. While money is essential to facilitating purchases and sales of real resources outside the banking system, it is not itself a physical resource, and can be created at near zero cost.

The fact that banks technically face no limits to instantaneously increasing the stocks of loans and deposits does not, of course, mean that they do not face other limits to doing so. But the most important limit, especially during the boom periods of financial cycles when all banks simultaneously decide to lend more, is their own assessment of the implications of new lending for their profitability and solvency. By contrast, and contrary to the deposit multiplier view of banking, the availability of central bank reserves does not constitute a limit to lending and deposit creation. This, again, has been repeatedly stated in publications of the world's leading central banks.

Another potential limit is that the agents that receive payment using the newly created money may wish to use it to repay an outstanding bank loan, thereby quickly extinguishing the money and the loan. This point goes back to Tobin (1963). The model-based analysis in our paper shows that there are several fallacies in Tobin's argument. Most importantly, higher money balances created for one set of agents tend to stimulate greater aggregate economic activity, which in turn increases the money demand of all households.

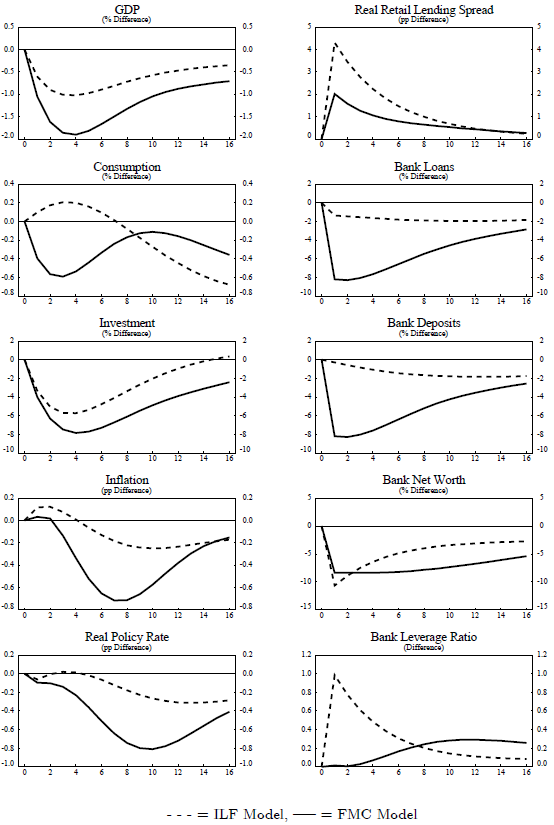

Figure 2 shows impulse responses for a shock whereby, in a single quarter, the standard deviation of borrower riskiness increases by 25%. This is the same shock that is prominent in the work of Christiano et al. (2014). Banks' profitability immediately following this shock is significantly worse at their existing balance sheet and pricing structure. They therefore respond through a combination of higher lending spreads and lower lending volumes. However, intermediation of loanable funds banks and money creation banks choose very different combinations.

Figure 2. Credit crash due to higher borrower riskiness

Intermediation of loanable funds banks cannot quickly change their lending volume. Because deposits are savings, and the stock of savings is a predetermined variable, deposits can only decline gradually over time, mainly by depositors increasing their consumption or reducing their labour supply. Banks therefore keep lending to borrowers that have become much riskier, and to compensate for this they increase their lending spread, by over 400 basis points on impact.

Money creation banks on the other hand can instantaneously and massively change their lending volume, because in this model the stocks of deposits and loans are jump variables. In Figure 2 we observe a large and discrete drop in the size of banks' balance sheet, of around 8% on impact in a single quarter (with almost no initial change in the intermediation of loanable funds model), as deposits and loans shrink simultaneously. Because, everything remaining the same, this cutback in lending reduces borrowers' loan-to-value ratios and therefore the riskiness of the remaining loans, banks only increase their lending spread by around 200 basis points on impact. A large part of their response, consistent with the data for many economies, is therefore in the form of quantity rationing rather than changes in spreads. This is also evident in the behaviour of bank leverage. In the intermediation of loanable funds model leverage increases on impact because immediate net worth losses dominate the gradual decrease in loans. In the money creation model leverage remains constant (and for smaller shocks it drops significantly), because the rapid decrease in lending matches (and for smaller shocks more than matches) the change in net worth. In other words, in the money creation model bank leverage is acyclical (or procyclical), while in the intermediation of loanable funds model it is countercyclical.

As for the effects on the real economy, the contraction in GDP in the money creation model is more than twice as large as in the intermediation of loanable funds model, as investment drops more strongly than in the intermediation of loanable funds model, and consumption decreases, while it increases in the intermediation of loanable funds model.

Banks are Not Intermediaries of Real Loanable Funds

To summarise, the key insight is that banks are not intermediaries of real loanable funds. Instead they provide financing through the creation of new monetary purchasing power for their borrowers. This involves the expansion or contraction of gross bookkeeping positions on bank balance sheets, rather than the channelling of real resources through banks. Replacing intermediation of loanable funds models with money creation models is therefore necessary simply in order to correctly represent the macroeconomic function of banks. But it also addresses several of the empirical problems of existing banking models.

This opens up an urgent and rich research agenda, including a reinvestigation of the contribution of financial shocks to business cycles, and of the quantitative effects of macroprudential policies.

Disclaimer: The views expressed here are those of the authors and do not necessarily represent those of the institutions with which they are affiliated.

craazyboy, June 19, 2015 at 11:35 amActually, the concepts of the money multiplier [hence the related concept of "bank money"] and loanable funds both existed simultaneously in my econ 101 book in college. But they were in different chapters.

The money multiplier, a consequence of fractional banking, does have a mathematical limit and it depends on the reserve ratio. Of course since banks are in the middle, they have control over whether they lend to the limit or not, if loan demand is there. If no loan demand, they would be "pushing on string", which was in yet another chapter in my econ 101 book.

A common layman misinterpretation of the money multiplier is that banks have their own printing press. That is not true – the banking system a whole creates bank money. When a loan is made, the bank now has an "asset" on it's balance sheet. That where "capital ratios" come into play limiting an individual bank.

craazyboy, June 19, 2015 at 11:07 am

Capital ratios, depending on how many SIVs you have. But if you get limited there, those numbers can be fudged. Or if you don't like faking complicated financial statements, you can always say, "faakit, I don't wanna be a bank. I'll be a CDO mill instead. Then maybe expand into insurance with CDS. That sounds better."

But economists are hopeless. They spend 50 years arguing over whether the sky is blue or green, then one comes along and says it's blue-green.

susan the other, June 19, 2015 at 11:32 amsardonicYes. Big ones. So big that it became necessary to start writing up more derivative contracts than loan contracts. This post explains derivatives better than anything I have read and it doesn't mention them once! But really, why else would Greenspin love them so much. Because it was the perfect way for banks to have all the cake and eat all the cake.

As long as banks' balance sheets were OK, they were OK, except that they could crash the entire world economy and then, oops, they weren't OK any more.

So enter derivatives to ensure their own balance sheets. Problem solved.

June 19, 2015 at 11:05 amThis is not academese, it's the reality. Read the BoE explanation of the same in Money creation in the modern economy.

Banks create money when they issue loans to others: they obviously can't issue a loan to themselves should they find themselves in a liquidity/solvency crunch. Hence the need for bailouts by somebody else.

Nathan Tankus, June 19, 2015 at 2:26 pmThis is the problem with using imprecise language like money.

Banks create deposits which are money to non-bank businesses, individuals, state and local governments and sometimes foreign governments. Deposits are however, not money to other banks. Settlement balances (money in essentially bank's checking accounts at the central bank) are money to them (in the sense that they can use them to settle their liabilities). A bank needs these to clear payments with other banks and the government.

Normally the central bank makes sure there are enough settlement balances in the system to clear payments between banks and those balances are distributed through the banking system when banks make daily unsecured loans to each other. In the crisis however, since all these loans were unsecured, banks stopped lending to each other. The government then had to guarantee interbank loans in the trillions to get the payments system functioning again.

Bailouts serve to make people believe the financial system is stabilized and to increase their official capital levels (capital levels matter because regulators are supposed to take over and resolve banks that are under-capitalized or even have negative equity). They are however, not essential to keep these banks going.

Letting banks lie about the value of their assets (which happened on a widespread level after the financial crisis) is just as effective as keeping these banks running as official bailouts.

The dirty little secret is that as long as the central bank makes sure that banks can borrow on the inter-bank loan market (or directly lend to them) and regulators all agree to lie (or not check) about the net worth and capital levels of a bank, they can stay in business. This is the nature of accounting control frauds in the modern age.

washunate, June 19, 2015 at 3:25 pm

So that leaves my original question. What is the policy value of the semantics?

In your description, banks are still constrained in their ability to lend. In order to loan more, to create new money, government has to make sure the bank IOUs are interchangeable with the national currency.

Nathan Tankus, June 19, 2015 at 3:45 pm

a) this is not true. in payment systems where bank liabilities don't trade at par (like antebellum united states) what adjusts is the value of the liabilities, not the banks ability to issue liabilities.

b) the definition of a modern currency is making sure that insured deposits in the same country equal each other in value. The most important Central Bank mandate is to preserve the integrity of the payments system. not putting enough settlement balances into the banking system means making interest rates explode and the payments system freeze. If you think that banks are at all constrained in lending by the threat of the central bank deliberately blowing up the payments system country wide, I have some penny stocks i would like you to invest in. What's interesting about Europe right now is that they don't have a "federal" (as in europe wide) insured deposit system and thus there is no such thing as insured deposits in the normal sense. as a result the ECB has blown up the payments system in cyprus and seems to be contemplating doing the same in Greece and wrote down deposits (in many ways like the antebellum banking system). Note that even in this case lending hasn't been constrained, the resulting liabilities have just been written down and may be written down in the future.

C) saying that banks are "constrained in lending" when this "constraint" is something that doesn't exist in the real world ie the United States and most central banks in the world refusing to provide the necessary amount of settlement balances to clear payments between banks at par is much more of a semantic game with no value for understanding policy than the reverse.

washunate, June 19, 2015 at 4:02 pm

I hear what you are saying. What you are saying is that there is no alternative.

The public must bail out the banksters.

Ben Johannson, June 19, 2015 at 2:37 pm

They can't create money for the payments system. U.S. banks don't make dollars. British banks don't make pounds sterling. They make bank IOUs for the deposit system.

Code Name D, June 19, 2015 at 3:32 pm

I am not sure this is completely true. The point of secularization is to sell these assets into the shadow markets. So not the markets hold the assets just created by the banks while the bank takes their money in exchange.

To create more money, all they have to do is find more loans to underwrite, then secularize the results.

Ben Johannson, June 19, 2015 at 3:49 pm

Banks can create money denominated in the government's currency but they can't create that currency. If you get a bank loan for $10,000 you're being given a bank IOU with a value of $10,000 - which means the bank isn't actually loaning you anything at all. They're agreeing to clear a payment through the reserve system in exchange for a series of small payments from you in the future.

Actual dollars can only exist in a reserve account or as cash.

OpenThePodBayDoorsHAL, June 19, 2015 at 4:22 pm

So far no one is mentioning the elephant in the room: why are money and credit necessarily interconnected?

We could certainly have money, produced in a quantity that matched underlying economic activity or population growth or something. On top of that we could have savings, investment, fractional lending etc.

Instead we have a system where every banking crisis is also a monetary crisis.

Milton Friedman suggested a desktop computer that created 2% more money each year.

Then there are those who suggest using some rare, shiny substance that is materially difficult to obtain:http://www.alt-m.org/2015/06/04/ten-things-every-economist-should-know-about-the-gold-standard-2/

Instead when we get a banking crisis (year 7 and counting) the only possible response is to flood the system with scrip, with predictable results (runaway inflation, this time in financial assets, last time in housing, the time before in commodities). Everybody moaning about the plunge in oil prices, but nobody seems to ask how/why they got to $140/bbl in the first place. Excess capacity everywhere you look, from Chinese steel to US college grads.

So let's have a real debate, not just argue how many angels are on the head of our current money/credit pin.

washunate, June 19, 2015 at 3:33 pm

Yeah, we very much agree here. Banks can create bank IOUs. Just like I can create wash IOUs. I, wash, do solemnly and seriously promise to give you a trillion dollars next week.

Now, gimme a trillion dollars today!

If the government backs my $1 trillion promise, then the government created the money, not me. If the government doesn't back my promise, then it ain't worth jack squat in payments systems. I couldn't even buy a coffee at Starbucks with it, nevermind a car or a house or something.

craazyman, June 19, 2015 at 4:32 pm

How does a dude driving a car with a gas gauge run out of gas?

hahahahah

If you fkk things up so bad you can't pay for your money making machine to make money then you can't make money. But it's not cause you can't make money, it's because you can't pay for your money making machine to crank it out1

How do all these boneheads get so rich if they can't make money? They could never get that rich if they just loaned money that was already there. No way.

They don't get rich linearly. They get rich exponentially. that's inconsistent with Not making money whenever they want. Loanable funds is linear. Making is exponential.

Where does the money come from if they dont make money? The first bank had to have money to start. where did that come from? It might have come from the govermint. But the govermint had to borrow it from people. They probably got it from a bank someplace that cooked it up. There was probably a bank in the Garden of Eden. That's probably what the snake was. A Banker. hahahahahahah. The apple was a loan. Then reality set it when Adam and Eve realized they had to hit the mall to buy some clothes so they could look for jawbs to pay it off.

craazyboy

June 19, 2015 at 4:45 pm

You read that in David Graeber's book, didn't you?susan the other, June 19, 2015 at 11:37 am

They can create money as long as there is someone to loan it to. Bec. they have to mind their own assets and liabilities to be legit.

But the trick is that they don't have to pay attention to reality as long as their books balance. It is such a clever fiction.

Theoretically it could work to smooth the bumps in an economy, except that it causes such precipitous crashes nobody can recover. One small detail.

washunate, June 19, 2015 at 12:32 pm

How can an entity that can create money ever have unbalanced books?

todde, June 19, 2015 at 12:43 pm

When the economy starts to shrink, earning potential goes down as do asset prices.

This prevents banks from making new loans. Banks loans are a function of past and future earnings.

At the same time the ability of the debtor to repay loans on the books is also curtailed.

This leads to a bailout.

cripes, June 19, 2015 at 3:37 pm

@washunate:

Now you're being obtuse. Deliberately?

It's clear they can create asset-money by loaning asset-money to borrowers.

We're not talking about paper bills here, which are a very small part of circulating "money."

washunate, June 19, 2015 at 3:44 pm

No, this is very important. A currency issuer can issue unlimited amounts of currency.

An entity that is not a currency issuer cannot. They are constrained by the existing resources.

human, June 19, 2015 at 11:41 am

Of course banks don't _need_ bailouts. They get them because they are able to coerce the populace through the great circle jerk of the Loanable Funds model!

washunate, June 19, 2015 at 12:30 pm

What do you mean banks don't need bailouts?

human, June 19, 2015 at 12:53 pm

Bailouts are used to bolster the publics' perception of the Feds' regulatory authority and responsibility and spread some more wealth around. Look at what happened to AIG!

washunate, June 19, 2015 at 1:01 pm

Exactly, look at what happened. Goldman Sachs would have ceased to exist without government support. The smartest bank on the planet was incapable of creating money.

human, June 19, 2015 at 1:39 pm

"ceased to exist" I find that very hard to believe. They might have had to cut bonuses…maybe.

washunate, June 19, 2015 at 3:40 pm

Well sure, we can't prove something that didn't happen. But we can point to how desperate actors behaved at the time. For example:

In light of the unusual and exigent circumstances affecting the financial markets, and all other facts and circumstances, the Board has determined that emergency conditions exist that justify expeditious action on this proposal

Unusual, exigent, emergency, and expeditious. In just one sentence.

http://www.federalreserve.gov/newsevents/press/orders/orders20080922a1.pdf

human, June 19, 2015 at 3:53 pm

Desperate?! They were handed an opportunity to gorge at the Fed discount window by becoming a bank holding company!!! They didn't hesitate and the rest is history.

Your comprehension seems to be so much neoliberal twaddle…meant for the proles. Of course they had their avarice covered by so much high-sounding legalese.

Benedict@Large, June 19, 2015 at 3:23 pm

If banks could create new money, they wouldn't need government bailouts.

Also, If banks could create new money, they wouldn't need to borrow depositors' money.

And, If banks could create new money, you wouldn't need depositors' insurance.

All of these speak to the "banks create money" idea as nonsense. Banks create credit.

However, the "loanable funds" idea is still nonsense. Loans are both made from and deposited to loanable funds, for a net of zero. This is critical, because it completely nullifies the idea that government borrowing affects interest rates by creating a shortage of funds.

Government spending does not slow other financial activity in the economy, which means the entire conservative paradigm in macroeconomics is garbage.

washunate, June 19, 2015 at 3:59 pm

Well said, it's all nonsense.

Personally I would tweak "banks create credit" to more specifically say that banks convert borrower credit into government credit. It's a transformation, an exchange, not an act of creation.

It's the borrower, not the bank, that supplies the credit. Indeed, a bank that systematically makes loans exceeding their borrower's ability to repay quite predictably goes out of business.

Vatch, June 19, 2015 at 4:08 pm

As Sardonic and Susan the Other have both pointed out, banks create money only when they issue loans to others. They aren't able to create money in any other ways. If there aren't borrowers, then the banks can't create money.

And when someone fully repays her or his bank loan, the money that was created by that bank loan is destroyed.

But of course the bankers have a multitude of ways to game the system.

fledermaus, June 19, 2015 at 10:57 am

It's easy to make money when you can lend the same $100 to ten different people.

sardonic, June 19, 2015 at 11:14 am

Money is credit, so your statement does not make sense. What is happening in the scenario you imagine is you are creating ten different loans. These dollars are no more "same" than are numbers in different banks demand deposit accounts.

todde, June 19, 2015 at 11:02 am

Since we run massive trade deficits there are.always dollars.offshore that can be lent to banks to meet any reserve requirements.

So banks ability to make.loans and create money would be a function of society's ability to repay.

Another point, banks don't create money out of thin air, they create money based on prior earnings (secured loans) or future earnings (unsecured loans).

Ben Johannson, June 19, 2015 at 2:41 pm

Bank loans aren't derived from cash flow, they are entries on the balance sheet. They come from nowhere and go back to nowhere when a loan is paid back.

Also, all dollar deposits exist within the computers of the Federal Reserve so there's nothing "offshore" to bring back.

todde, June 19, 2015 at 2:51 pm

Not all dollar reserves are sitting in the federal reserve , although many are.

And cash flow of the borrower matters.

Ben Johannson, June 19, 2015 at 3:08 pm

All dollar deposits exist on computers at the Federal Reserve. Anyone at the Fed, Treasury and CBO can tell you this.

Cash flow of the borrower is a matter of underwriting standards, not capacity to extend a loan.

Jesse, June 19, 2015 at 11:14 am

Are all 'banks' the same?

In a regime where the banking authority imposes a strict 50% reserves requirements and eliminates the gimmickry of overnight sweeps to gimmick the base of assets and liabilities, and stresses certain types of higher quality reserves and a conservative valuation, are the 'banks' the same as a regime where reserve requirements are minimal and easily financialized?

Is an economy where loans are intimately tied to organic growth through 'real' economic activity and a high velocity of money (sorry Austrians but it does mean something) different from one in which the banks are largely preoccupied with speculating with their own trading books and money supplied by the central banking authority monetizing debt?

A model that fits a particular circumstance which is itself is rather distorted from the historical norm is just that. An example of a particular circumstance and not a general model for a range of conditions.

susan the other, June 19, 2015 at 11:53 am

This post was killer. It left us all with the question, Well just how do we change our financial behavior to fit the real model, the money creation model. Because we all went blithely on our way for decades thinking things were balancing out when in fact they weren't.

It sounds a little Minsky, in that the good times always crash but nobody knows what to do about it. So at least Minsky had an inkling of this. And there were plenty of crashes when banks really did intermediate loans, but they were recoverable.

When did loan intermediation end? 1913 and with the creation of the Federal Reserve? If so it is amazing it was mythologized for so long. One way to begin to get real would be to analyze the value of money, and its creation, by what it accomplishes. So, that's after the fact and hard to do in a "free market" but the FM is also another myth. MMT looks at this very clearly. We don't need loans to run the sovereign business of the country. That takes care of a large chunk of the mess right off the top.

susan the other , June 19, 2015 at 2:12 pm

yes. it's scary. Mistakes are easier to make than progress. But we have much better analytics now… maybe we can estimate what will happen and actually maintain a steady course. I'd like to think that.

Synoia, June 19, 2015 at 12:08 pm

Step 1. When did loan intermediation end? 1913 and with the creation of the Federal Reserve?

Step 2. Getting off the gold standard in 1972.

Min, June 19, 2015 at 12:26 pm

Back in the free banking era of the 19th century, there was a bank in Rhode Island that issued $600,000 in bank notes backed by 7 bits ($0.875 in coins) in the vault. ;)

Source: A talk on CSPAN book TV a few years ago. Sorry I can't be more definite.

craazyboy, June 19, 2015 at 1:06 pm

That was back when we/Europe were still trying to decide if we should do fractional gold banking, or if banking based on the banker's reputation was adequate. 'Course bankers found that cheating on fractional gold banking was very profitable as well.

Adam1, June 19, 2015 at 1:12 pm

The basis of loans create deposits has been around since shortly after the creation of double-entry bookkeeping. The FED's existence only stabilizes and standardizes the interbank clearing process and has little to do with loans create deposits. The gold standard only fixed foreign exchange rates and floated domestic rates, it had little impact on loans create deposits.

Larry Headlund, June 19, 2015 at 12:53 pm

When did loan intermediation end?

According to Lombard Street (1873) by Walter Bagehot lending as a function of 'banks' preceded their accepting of deposits by some years.

Min, June 19, 2015 at 12:21 pm

Can't we all agree that banks create money? Fractional reserve banking makes no sense unless banks create money. I learned that in high school, fer crissakes!

washunate, June 19, 2015 at 12:58 pm

No, we can't.

:)

But seriously, it's important to understand why there are differences of opinion. The monetarists (of all stripes, this is not a left/right thing) want people to think that money (as in currency) is created by banks because that obfuscates the real actor – the government.

When the government accepts the bank IOU as exchangeable 1:1 with the national currency, then it is the government that has created more currency units, not the bank. But if people can be convinced to ignore that little step, it looks like banks create the currency units themselves.

And once you accept those bank IOUs as legitimate currency units in the boom times, well, you've committed to a policy of bailing out criminal and/or insolvent management teams during the bust times.

Benedict@Large, June 19, 2015 at 3:30 pm

Banks don't create money. You were taught wrong. The model used where banks create money does not match the accounting a bank uses. There is no money multiplier.

[Note that several first world countries have reserve requirements of zero percent. They do not suffer hyperinflation, as the money multiplier would suggest. Even Ben Bernanke said that the reserve percentage only affected the cost of money, and that he would have preferred the US also move to a zero percent reserve.]

craazyboy, June 19, 2015 at 4:21 pm

Banks create credit, but common usage sometimes interchanges money and credit when the distinction isn't relevant to the narrow context of the discussion.

There is a money multiplier. No one made it up – if you have fractional banking it is there. Math says it can happen. You could call it a credit multiplier if you prefer, but I try and limit how many new words I make up.

The reserve ratio limits the money multiplier to a non-infinite number. The reason we have bank reserves is so in theory banks have some cash on hand to satisfy deposit withdrawals.

Capital ratios are used by regulators to monitor bank solvency. Some counties have zero reserve requirements. I guess the CBs there will FedEx your money to you. Who knows. I'll take the FDIC insurance.

Canada has a 0 reserve requirement. Canada has a housing bubble. So does Oz. The EU has even more lax capital ratio requirements than the US. The EU is now a basket case. The US has asset bubbles.

Bernanke is an a-hole.

nothing but the truth, June 19, 2015 at 1:30 pm

when Y is talking about investment / saving, she is talking about the real side of the picture.

when you are talking about the loan-> deposit causality, this is from the technicality of the financial system.

both are correct because they are talking about apples and oranges.

the money multiplier story is something that economists have spread and they are _so_ surprised to find out that it is not the (complete) truth. partly this story comes from history because that is how banks started. That is because gold is a real resource – you cannot just create it fictionally and lend it. Now that money is nothing, there cannot be a shortage of nothing, unless it is to keep the "people in their place". When the likes of Goldman have a shortage of money, it is produced out of nothing.

The view of money multiplier is correct, except for the causality part. loans create deposits, but those deposits belong to someone.

From the operational side of things, there is not much difference. Whether the bank creates loans and then deposits, or deposits first and then loans, the fact remains that the bank is on the hook for the loan (to its capital reserves) if it defaults, so the bank has to be careful whom to lend to. Reckless lending can even lead to jail time for the lender (or it used to).

so long store short, there is not much to see in this technical view of things. Yes under the hood the car is very complicated, has 80+ microprocessors and so on. The function of the car is to be driven. To obsess about spark plugs is to forget the function of the car – transport.

This is the real question – what is the function of money in the real economy, who is benefiting from the legalized frauds, and how to stop this and bring finance to serve the real economy, not vice versa. This is political economy, not really finance. Yes to fix something you have to understand it. But it should be understood that we diagnose in order to prescribe.

DolleyMadison, June 19, 2015 at 2:01 pm

Wow – A few days ago Maxine Waters wrote an op-ed about the 2-tier justice system when it comes to bankers – surprisingly printed by American Banker. So I try to click on it and the link is DEAD. So I search for the article and found it cross posted on 3 other sites – and on each one the link was broken. WOW. And we wonder how the "2-tier justice system" became that way…

See dead links below:Big Banks and America's Broken, Two- Tiered …

http://www.americanbanker.com/bankthink/big-banks-and-americas...Jun 16, 2015 · In February, federal prosecutors began a 90-day examination to determine whether to bring cases against individuals for their role in the 2008 financial …

Big Banks and America's Broken, Two- Tiered …

grabpage.info/t/www.americanbanker.c…/bankthink/big…CachedAmerica, American, Bank, Banker, Banks, Big, Bond, Broken, Buyer, Justice, Mortgage, National, News, PaymentsSource, System, The, Think, Tiered, Two, and

Big Banks and America's Broken, Two- Tiered …

housingindustryforum.com/industry-newswire/american…CachedJun 16, 2015 · … Two-Tiered Justice System By American Banker | June 17, 2015. SHARE Read Article. Comments.

Lambert Strether, June 19, 2015 at 3:07 pm

Adding epicycles to dynamic stochastic general equilibrium models, because markets (I would argue) do not equilibriate (though they may be equilibriated, as with LIBOR).

Trying to make a "like a fish needs an epicycle" joke here, but gotta run….

pcle, June 19, 2015 at 3:23 pm

"Figure 2 shows impulse responses for a shock whereby, in a single quarter, the standard deviation of borrower riskiness increases by 25%."

So it looks like in this model "shocks" just come from outer space. There is no sense in which the system itself generates crisis as part of its very working ? And where's the fraud parameter ?

Jesper

June 19, 2015 at 4:00 pm

Some central bankers believe that banks create money.

Some central bankers believe that financial markets can self-regulate.Given the above facts about central bankers, can we conclude if central bankers always know what they are talking about (even when it comes to monetary policy)?

Reply ↓

horostamJune 19, 2015 at 4:05 pm

ok, so I understand that loans create deposits, but…im confused about the reverse.I have this crazy exercise i try to do.

I try to visualize the thought experiment of all loans and govt deficits being paid back so that there are 0 us dollars in existence. (kind of like an economic version of reimagining the big bang in reverse)

Leaving aside for the moment the fact that there is not enough money in existence to make all interest payments… (is this even true?)

how does the money get destroyed when a loan is paid back? You will say "the balance sheets are simply adjusted, a deposit and a loan simply disappear."

i can visualize this, but i dont understand it.

So what is the difference, for the bank, between a paid back loan and a default on the loan?

and what happens to the interest payments (when they are made)? they move from deposits to reserves (or equity or whatever)… how are they seperated from the deposits that simply "disappear?"

I would really like to understand this…

Reply ↓

Nathan Tankus, June 19, 2015 at 4:25 pm

"So what is the difference, for the bank, between a paid back loan and a default on the loan?"

when a person makes a principal payment on a loan their account is debited and the value of their debt (an asset to the bank) is decreased. when a person defaults on a loan the value of their debt ( again an asset to the bank) becomes zero (well actually more like pennies on the dollar since it will likely get sold to a debt collector). In other words, one shrinks the bank's balance sheet while keeping it's net worth the same while the other decreases the bank's net worth

"and what happens to the interest payments (when they are made)? they move from deposits to reserves (or equity or whatever)… how are they seperated from the deposits that simply "disappear?""

interest is paid in the same process ie debiting the borrower's account. the difference is that interest payments increase the bank's net worth since they have less liabilities ( ie less deposits) without decreasing the value of their asset (the borrower's debt).

In short, banks lend to increase their net worth.

horostam, June 19, 2015 at 4:49 pm

In other words, one shrinks the bank's balance sheet while keeping it's net worth the same while the other decreases the bank's net worth

do you mean "the banking system's net worth?"

if (in both cases) the loan asset value goes down, the only way net worth stays the same is if deposits decrease proportionately.

What if your deposit account is at another bank? What is the difference, to an individual bank, if its a default or principal payment?

Their liability side doesnt change…

Clearly i am missing something…

craazyboy, June 19, 2015 at 4:27 pm

"So what is the difference, for the bank, between a paid back loan and a default on the loan?"

In the case of default, the bank puts your house on it's balance sheet and it is then house money.

Interest is tricky. It comes from future years 31 thru 33.

Nathan Tankus, June 19, 2015 at 4:31 pm

yes i abstracted from collateral to make the basic point. if the loan is collateralized than the fall in the bank's net worth from a default is equal to the value of the loan minus the value of the collateral. This is part of why so many people were so cavalier about lending in the housing market because people assumed that rising capital gains would keep these loans profitable even if the rate of default increased. Of course when housing prices fell and people started to take capital losses…. and here we are.

What Paul Krugman Should Have Learned from James Tobin but Didn't

Paul Krugman last week wrote yet another response on the issue of "how banks work". This time he has decided to cite the two papers that he relies on to "think about the role of banks in the economy". The first is a thirty year old paper on bank runs that, although interesting, isn't relevant to the topic at hand. The second is a fifty year old paper written by James Tobin and William C. Brainard that is directly related to the relationship of the "monetary base" (briefly put, physical currency and coins plus settlement balances in checking accounts held with the central bank) to the overall level of loans. However, the authors make pains to point out in the beginning of the paper thatThis paper is addressed to these questions, but it treats them theoretically and at a high level of abstraction

This is important to emphasize. Krugman's thinking on the relationship between settlement balances (also called bank "reserves"), deposits and loans is primarily determined by one fifty year old theoretical, very abstract paper written by theoreticians. In other words, the people who actually implement monetary policy or are in the business of banking have had little to no influence on Krugman's thinking about banking. A priori indeed.

There is more here to unpack however. James Tobin is actually quite a famous economist (known best for the idea of a "Tobin tax", a tax on spot currency transactions) who didn't die after co-writing this paper. In fact, he won a Nobel prize in 1981 and didn't die until 2002. Nor did he think that he had sufficiently dealt with the role of banks and monetary policy because he continued to develop his ideas in these areas for decades afterwards. Thus Tobin himself wouldn't agree that "Tobin and Brainard got it all straight half a century ago". One truly seminal paper Tobin wrote on the topic is "The commercial banking firm: a simple model". In this 1982 paper (nearly 20 years after the paper that Krugman cited), Tobin lays out a series of views that stand in stark contrast to views expressed by Paul Krugman.

In a post calling the belief that banks "create money" "Banking Mysticism" , Krugman states that:

First of all, any individual bank does, in fact, have to lend out the money it receives in deposits. Bank loan officers can't just issue checks out of thin air; like employees of any financial intermediary, they must buy assets with funds they have on hand

Compare this statement with the statement of James Tobin, who Paul Krugman claims to have learned how banking works from:

When a bank makes a loan to one of its customers it simply credits the amount to the borrower's account. In the first instance, therefore, the bank's deposits are increased dollar for dollar with its loans. As the borrower spends the proceeds by check, some of the recipients will leave the money on deposit with the lending bank, while others will deposit their receipts in other banks or convert them into currency. As these recipients spend their balances and in succeeding generations of transactions, the lending bank will lose more and more of the deposit created by its initial loan

Thus, the one paper Krugman relies on "to think about the role of banks in the economy" was written by someone Krugman would derisively call a "banking mystic". Such are the ironies that emerge from ignorance. There is more to learn from this interesting paper. First let us go back to Krugman's argument.

In the "Banks and the Monetary Base" post, Krugman poses a thought experiment:

Now, think about what happens when the Fed makes an open-market purchase of securities from banks. This unbalances the banks' portfolio - they're holding fewer securities and more reserve - and they will proceed to try to rebalance, buying more securities, and in the process will induce the public to hold both more currency and more deposits. That's all that I mean when I say that the banks lend out the newly created reserves; you may consider this shorthand way of describing the process misleading, but I at least am not confused about the nature of the adjustment.

Krugman's argument here is confusing. In the thought experiment, his hypothetical bank tries to lower the amount of settlement balances it has by buying a security. This can only work in the aggregate if some other bank desires to hold more settlement balances or will use settlement balances to reduce its indebtedness to the treasury/central bank. Otherwise the banking system as a whole has more settlement balances than it desires. In no sense do "banks lend out the newly created reserves". Saying that a completely incorrect description is a "shorthand" isn't logically coherent. Further this process (if the banking system as a whole has more settlement balances than it desires) will lead to the inter-bank loan rate (the fed funds rate) to fall to the Interest On Reserves (ior) rate unless the central bank intervenes to preserve its interest rate target.

In the "Banking Mysticism" post and elsewhere Krugman argues that "currency is in limited supply - with the limit set by Fed decisions". This is obviously not true -as confirmed by a simple glance at the New York Federal Reserve website.

Depository institutions buy currency from Federal Reserve Banks when they need it to meet customer demand, and they deposit cash at the Fed when they have more than they need to meet customer demand

Even if one desired to be charitable and say by "currency" Krugman meant settlement balances held with the central bank, this is still incorrect. The central bank provides all the settlement balances needed to get banks to lend to each other at the targeted inter-bank loan rate. One can see evidence of this every couple of weeks when an actual central bank practitioner gives a speech (you can subscribe to the speeches here). Take for example this speech given by an Australian central banker on the same day as Krugman's blog post went live:

As with our regular open market operations, it will not be the Bank's aim to simply supply overnight funds to those individual institutions that are short, or absorb overnight funds from those that are long cash. That is what the interbank cash market is for. As I mentioned a minute ago, the Reserve Bank's operations are designed to put the appropriate amount of settlement funds in the system as a whole so that, in managing their individual ES accounts, ADIs [deposit-taking institutions] will transact with each other at the cash rate target

This means that whenever deposit-taking institutions want more settlement balances, the central bank will provide them on demand (either through lending or through open market operations). Thus, in no sense is "currency is in limited supply - with the limit set by Fed decisions". The loss of settlement balances through out-flowing payments has no impact on lending unless the additional cost of borrowing more settlement balances makes lending unprofitable (quite unlikely). Note that the cost of settlement balances can vary wildly (as they did under Volcker) but they must ultimately be supplied at some price if payments are going to clear between banks. If you want to argue otherwise you have to argue that the central bank is willing to let the interbank loan market collapse and checks to stop clearing if some arbitrary amount of settlement balances is seen as "too many".

Interestingly, the argument that it is the expected cost of acquiring additional settlement balances that matters is in James Tobin (1982). From the abstract:

In case withdrawals exceed its defensive position in liquid assets, the bank incurs extra costs in meeting reserve requirements, penalties in borrowing or losses in disposing of illiquid assets.

Thus it is not the quantity of settlement balances that impacts the loan decision of an individual bank, but the expected spread between the cost of liabilities and the return on assets. Being a good neoclassical, Tobin believes that the "profit maximizing bank" will equate expected marginal cost and expected marginal revenue. I think that is nonsense but at least we're having the right conversation- one about the costs of liabilities and the return on assets rather then the quantity of settlement balances and deposits. Anyway, who are you going to believe? The Central bankers and the sole expert Krugman relies on to understand banking, or Paul Krugman?

Read more at http://www.nakedcapitalism.com/2013/08/james-tobin-versus-paul-krugman.html#mCulqPtePjFuucWF.99Hugh:

I think we have known for a long time now that Krugman doesn't understand banking, money, or debt. He also used to be an ardent free trader so I am not sure how much he understands about trade either.

Travis says:

Ken, Krugman is well known KINO. Keynesian in name only.

craazyman says:

not one of them understands any of this because they've been brainwashed their whole lives by technical instruction in the levers of monetary bureaucracies.

They have never studied cultures that organize themselves in ways that don't use money and what that might imply for how humans self-organize and what role money plays in that process.

And so they know only the forms they've been taught and not the broader forms of nature from which those they've been taught arise.

It's as if they know the statue but can't comprehend the marble from which it is carved. Michaelangelo would never have stood for that for 10 seconds.

psychohistorian says:

So why are we not having the discussion about whether the historical plutocracy is best making capital allocations in the long run or should sovereign entities be "trusted" with capital allocations and the "profits" from providing banking as a public utility?

It is evident the plutocracy has erred (kind word) in many areas of social policy and governance, but the question becomes if the secular public can build a "better" (equitable, just, future prudent, etc.) society.

I think we can and should get started on it immediately.

mike smitka says:

I think you've got two different issues here – portfolio rebalancing (Tobin & Brainard) and whether that rebalancing is costless (Tobin 1982).

Note that (as a grad student in Tobin's macro class in 1981, so familiar with both papers) Krugman seems to capture Tobin's approach well, albeit I find Krugman's prose sloppy - he fails in trying to make the ideas more accessible.

Benoit Essiambre:

I don't always agree with Krugman but I think Nathan is playing semantic games here. Krugman understands how this works. He's just using many "shorthands", such is the nature of economic vulgarisation.

For example: > Thus, in no sense is "currency is in limited supply - with the limit set by Fed decisions".

Its not limited in actual quantity but it is indirectly limited by the fed interest rate target.

diptherio says:

No. Currency is in no way limited in supply. The Fed does not target or even care much about the quantity of money, only the interest rate. The last time the Fed tried to target and control quantity was a disaster (Volcker, starting about '79). Krugman isn't using short-hand, he's just wrong.

By repeating the fallacy of limited currency, Krugman plays into the "we're broke" meme, so beloved by deficit hawks. But then again, Krugman himself believes that "in the long run" budget deficits are harmful and pushes what is essentially "austerity lite," so maybe that's on purpose.

Read more at http://www.nakedcapitalism.com/2013/08/james-tobin-versus-paul-krugman.html#mCulqPtePjFuucWF.99

middle seaman says:

One of the most prominent voices on the liberal side is Krugman and his constant and lengthy hammering at the reactionary, illegitimate and destructive policies we live with.

Is Krugman perfect? Surely, he isn't. But then every Monday and Thursday some liberal decides to attack Krugman. Typically, claiming that he is totally wrong, an ignoramus and even worse.

Although such attacks follow a well-worn tradition, I find it pointless.

Read more at http://www.nakedcapitalism.com/2013/08/james-tobin-versus-paul-krugman.html#mCulqPtePjFuucWF.99

David Lentini says:

Frankly, I find the arguments against Krugman's and the conventional wisdom far more convincing. So, why won't Krugman and the CW admit this? Well, once you make the admission, then banking is no longer "boring" (to quote Krugman) and the whole basis of macroeconomics is a lot messier. So, let's just keep looking under this street light a little while longer.

F. Beard says:

However banking works, it should not require government privileges to work much at all UNLESS it is crooked – which it is.

Banking is gambling – betting that one can borrow short and lend long and not get caught. So why does the government subsidize gambling?

James says:

"his hypothetical bank tries to lower the amount of settlement balances it has by buying a security. This can only work in the aggregate if some other bank desires to hold more settlement balances or will use settlement balances to reduce its indebtedness to the treasury/central bank."

If the banks have excess reserves as the result of Fed open market purchases, and the banks then make more loans to the public, the level of excess reserves in the banking system GOES DOWN.

This is because the extra reserves stop being "excess" and instead become "required", as the direct result of the extra loans to the public.

Some of those loans also result in the public withdrawing more cash, so reserves also go down in that sense.

"In no sense do "banks lend out the newly created reserves"."

Banks lend reserves in the sense that each new deposit is a claim on base money (reserves) – i.e. a promise made by the bank to pay base money to the depositor, or on their behalf, on demand. A bank deposit is simply a bank debt, a promise to pay base money on demand.

A bank deposit can thus also be thought of as a loan by a depositor to the bank. This is clearly the case when a depositor deposits physical cash at a bank. But it is still the case when a bank creates a new deposit "out of thin air", when it makes a loan. Each time a bank creates a deposit, the depositor is essentially lending base money (either physical currency or its electronic equivalent, reserve balances) to the bank. No base money has to actually change hands for this to be the case.

So banks don't normally "lend out" reserves, because the reserves generally stay inside the banking system (unless they are withdrawn as cash) as so don't go "out". However banks still "lend reserves" in the sense that each deposit is simply a promise to pay reserves (base money) on demand.

"Further this process (if the banking system as a whole has more settlement balances than it desires) will lead to the inter-bank loan rate (the fed funds rate) to fall to the Interest On Reserves rate"

Not necessarily!

If the banks make more loans, the amount of excess reserves goes down, as explained above. This causes the Fed Funds rate to rise, all else being equal. So if the Fed adds excess reserves through OMPs, and then the banks increase the amount of their loans to the public by a sufficient amount, the Fed Funds rate can potentially stay the same, or even RISE (assuming the Fed allows it to rise by not intervening).

mdm says:

@James:

"If the banks have excess reserves as the result of Fed open market purchases, and the banks then make more loans to the public, the level of excess reserves in the banking system GOES DOWN."

This is incorrect, and would only be applicable in an institutional setting with contemporaneous reserve accounting. The actual institutional arrangement uses 'lagged reserve accounting'. The actual set up is a little complicated but it basically works as follows: a bank is required to hold a certain amount of reserves equal to an average of a subset of liabilities (e.g. certain types of deposits) from the previous 'maintenance period'. In no way does a bank issuing a loan now affect the level of 'excess reserves'. It may in the next maintenance period but not the current one.

Keep in mind that in banking systems without reserve requirements, ALL reserves are by definition 'excess reserves', so again your example is of a limited case, applying to a highly stylized American case.

"If the banks make more loans, the amount of excess reserves goes down, as explained above. This causes the Fed Funds rate to rise, all else being equal. So if the Fed adds excess reserves through OMPs, and then the banks increase the amount of their loans to the public by a sufficient amount, the Fed Funds rate can potentially stay the same, or even RISE (assuming the Fed allows it to rise by not intervening)."

As I mentioned in my response here, this is only applicable in with contemporaneous reserve accounting.

Your post misses the important point that, as Nathan argued above, the supplying of reserves is an accommodating behavior by the central bank to ensure that the there are sufficient reserves in the banking system. If we were to assume the causal process in your post (increase in reserves -> increase in loans), then we're left with the awkward scenario of explaining banking systems that operate by either removing all reserves from the system (the Canadian case) or even where the amount of reserves is deliberately left deficient in order to encourage active participation between the central bank and the banking system, i.e. it encourages the banks to be actively communicating with the central bank, so that the central bank can better forecast the desired quantity of reserves demanded by the banking system (as is the case in the Australian example).

Continuing on with your example, and the assumed causal process: if the OMO leave the banking system with more reserves than it desires to hold, the interbank rate would fall to zero or the lower bound set by the liquidity absorbing standing facility. On the other hand, if the banking system is deficient in reserves, i.e. the amount of reserves in the banking system is less than the amount demanded, then the interbank rate rise to infinite, with no possible market clearing price. So again, it's not a great description of actual monetary policy implementation. Of course, in practice both instances are avoided because central banks have adopted standing facilities, as important instruments to minimize interbank interest rate volatility.

. . .

There's a part in the middle of your post which is more semantic than anything else. If you want to call it 'lending reserves' fine, but it's unnecessarily obscure.

digi_owl:

Shit like this seems like a repeating pattern in mainstream economics. Someone writes a paper that provide a semblance of backbone to vague theories that border on "might makes right", but in later years categorically disown that paper as a unrealistic theory wank. But still said paper gets held up as the height of economic theory decades later. If anything it puts meat on the argument that economics is the religion of kleptocracy, with Ayn Rand as their patron saint…

Animal Nitrate

Probably the best summation of Economics and Economists I've read anywhere, ever :

"not one of them understands any of this because they've been brainwashed their whole lives by technical instruction in the levers of monetary bureaucracies.

They have never studied cultures that organize themselves in ways that don't use money and what that might imply for how humans self-organize and what role money plays in that process.

And so they know only the forms they've been taught and not the broader forms of nature from which those they've been taught arise.

It's as if they know the statue but can't comprehend the marble from which it is carved. Michaelangelo would never have stood for that for 10 seconds."

What has failed this past few years is the notion of Economics itself.

The fact that there are so many blogs and commentators pitching in about the price of gold or oil or shares still amazes me.

None of these economists seem to have the remotest idea that Economics, at its most basic, is the study of people and their interactions. Cullen Roche in a recent post on inflation suggested that while peoples real world experiences didnt tally with his theory/data (he said there was 'no inflation') that the peoples experience must be wrong. It certainly couldnt be errors in his data. Or the idea that his data was incomplete. Or that his theories, models and data were wholly f**king useless. But this is what you are up against. You are not allowed to believe the evidence of your own eyes. You must accept the evidence (and collection and analysis of same) presented to you as fact. To do otherwise makes you nuts; regardless of what your eyes and ears tell you. These people are out to subvert your very mind with their bluster and bullsh!t. Look away. Turn the other cheek.

Nathanael says:

There is no "inflation", because it's not inflation until your wages go up. Did you get a raise recently? If not, no inflation.

What there is is nasty price-gouging in consumer products. The price-gouging creates profits, which go into CEO pockets.

That's not inflation.

Roland says:

Nathanael, I think you're trying to "define the problem away" here.

Of course you can get widespread price inflation without wage increases.

There are good recent examples to be had. e.g. The price of higher education has soared in recent years, even as incomes have tanked. How? Easy: the consumers substituted large amounts of debt for the income they lacked.

A rapid expansion of available credit can serve as fuel for inflationary fires.

History is also full of examples of large numbers of people simply getting "eaten up" by secular price increases that exceeded their incomes. Entire classes can get effectively liquidated in such fashion.

larry says:

I agree with Mike Smitka. Krugman fails to make the ideas more accessible and is sloppy. I would like to add that K's treatment of data is also often sloppy, even to the extent of leaving out the axes on data graphs, which is completely unacceptable.

Nathan Tankus is working with Steve Keen. And a while ago, Keen and Krugman had a public argument with Keen contending that Krugman's understanding of macroeconomic issues left something to be desired, more or less. I believe that the general consensus was that Keen "won" the interchange. Certainly, Krugman never seemed to adequately respond to Keen's criticisms.

I have often wondered how deep or broad Krugman's knowledge of economic history actually is. As a comparison, one can peruse Antoin Murphy's Genesis of Macroeconomics, a brilliant exposition.

Lambert Strether says:

"Nathan Tankus is working with Steve Keen." Look out, world!

Dan Kervick says:

The bottom line is that when Krugman says this:

Similarly, if we ask, "Is the volume of bank lending determined by the amount the public chooses to deposit in banks, or is the amount deposited in banks determined by the amount banks choose to lend?", the answer is once again "Yes"; financial prices adjust to make those choices consistent.

he's just wrong.

The public's portfolio balancing choice concerning how much of its present monetary assets it decides to hold in the form of physical currency and how much it decides to hold as balances in bank deposit accounts in no way determines the amount of bank lending. Banks in the aggregate can issue new liabilities in the form of deposit balances in exchange for borrower promissory notes, and then acquire any additional payment assets it needs (reserves) to meet the obligations that the new liabilities incur.

Acquiring those assets usually has a cost, and so the bank's concern is the difference between the amount it can earn from the loans and the cost of acquiring the additional funds. But banks don't have to acquire the funds first, and to expand their lending they certainly doesn't have to rely on the public making additional cash deposits at banks.

MaroonBulldog:

"But banks don't have to acquire the funds first, and to expand their lending they certainly don't have to rely on the public making additional cash deposits at banks." As any reflective persons might readily understand, who ever wrote a check against a home equity line of credit, or successfully asked a bank to extend a credit card limit and then made a large purchase the same day, or negotiated a bank's car loan at the dealership that simultaneously sold them thenew car. Here is something I wonder about when economists make statements like Krugman's: "Do such persons never reflect upon the practical necessities of their own transactions in the real world? Or is it that they have never done any transactions with banks?"

Nathanael says:

Indeed, in actual practice banks pay no attention in the short or even medium term to how much deposits they have.

They lend out money profligately (printing money) and then go to the Federal Reserve at the end of the day to "balance their books". They can operate with NO deposits at ALL, and they will happily do so, until the regulators come after them. If they look at their books at the end of the quarter and worried about the regulators, they start advertising for deposits. Eventually.

Alejandro says:

Imho, here is a case study in the role of credentials and effective obscurantism.